By

The scenario

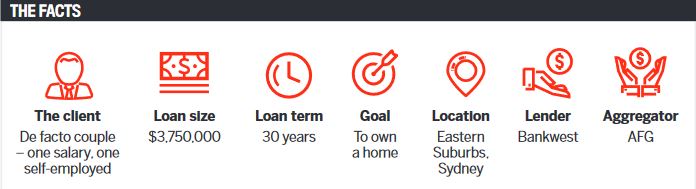

We were introduced to this client by a real estate partner. They were a couple looking to purchase a new owner-occupier property, worth over $5m, through the agent, and they required a very fast approval turnaround to be able to secure the home of their dreams.

One of the applicants was on a PAYG full-time salary – very straightforward – whereas the other applicant was a self-employed individual with income predominantly made up of commissions and dividends from a large shareholding in a listed company.

We had the clients conditionally approved within 24 hours, and they bought the property that day with a delayed settlement of 16 weeks. The reason for the long settlement was the fact that the clients had two existing investment properties that they wanted to sell, and the sale proceeds were to be contributed towards the new purchase, leaving them with as little debt as possible on their new principal place of residence.

One property sold easily, yet they struggled to sell the second property, and unfortunately, with four weeks to go until settlement of the new purchase, they still hadn’t found a buyer.

The solution

Once the clients confirmed they were having trouble selling the second property, we had to take the initiative and proceed with a back-up application with another bank.

We worked on a scenario in which they could keep the existing property as a tenanted investment but still settle the new purchase.

Borrowing capacity was evident; however, as mentioned, the clients also had a significant share portfolio, so there was the potential to sell shares and come up with additional funds to complete the purchase without selling the second property.

We had this application approved within two business days, as valuation reports had already been completed upfront in case they were needed for this purpose.

Things don’t always go to plan. Buying before selling is risky, and you need back-up options for your clients before allowing them to proceed with the purchase

The clients were very happy with the fact that they had the back-up scenario approved so quickly, and this gave them a lot of comfort and reassurance that they were not at risk of losing a deposit.

In the end, on the same day we obtained the second approval, the client secured a buyer and decided to sell the property.

They made the decision to take a lower price rather than have to sell part of their share portfolio to cover the purchase.Once the property was sold, we went back to the original lender and increased the loan amount slightly. This enabled us to limit the amount of equity they needed to put towards the purchase (they had originally assumed a higher sale price for the second property), which left them in a strong liquidity position.

This was important to them because of the current economic climate due to COVID-19, as the client did have concerns in regard to future commission income. They also had concerns around future dividends due to the stock market crashing amid the COVID 19 uncertainty.

But increasing the loan amount ensured they had surplus funds at hand post-settlement to fall back on, in case they needed them in the coming months.

The takeaways

Things don’t always go to plan. Buying before selling is risky, and you need back-up options for your clients before allowing them to proceed with the purchase.

Always ensure that when people are buying first, they negotiate as lengthy a settlement as possible so they have time to sell their assets, such as existing property and/or shares, etc.

Have a bridging back-up if possible. For this client, one of the existing properties was owned in a trust, and therefore bridging was not going to be possible. For this reason we recommended they push for 16 weeks on the settlement, and we ensured that they could keep the property as an investment if the sales didn’t go to plan.

Make sure multiple lenders will provide a solution – this is to ensure you have back-ups when it comes to all the elements outside of your control, such as valuations, sale outcomes, etc.

Before we gave the client the go-ahead to purchase, we knew that three banks would have lent them the money (for both scenarios), so they had the confidence to proceed with the property purchase.

Finally, when purchasing first, we always encourage clients to work on a conservative sales estimate to avoid shortfalls. We suggest 10% below the sales appraisal at a minimum.

Charlie Loveridge

Charlie Loveridge

Senior credit adviser at

Shore Financial