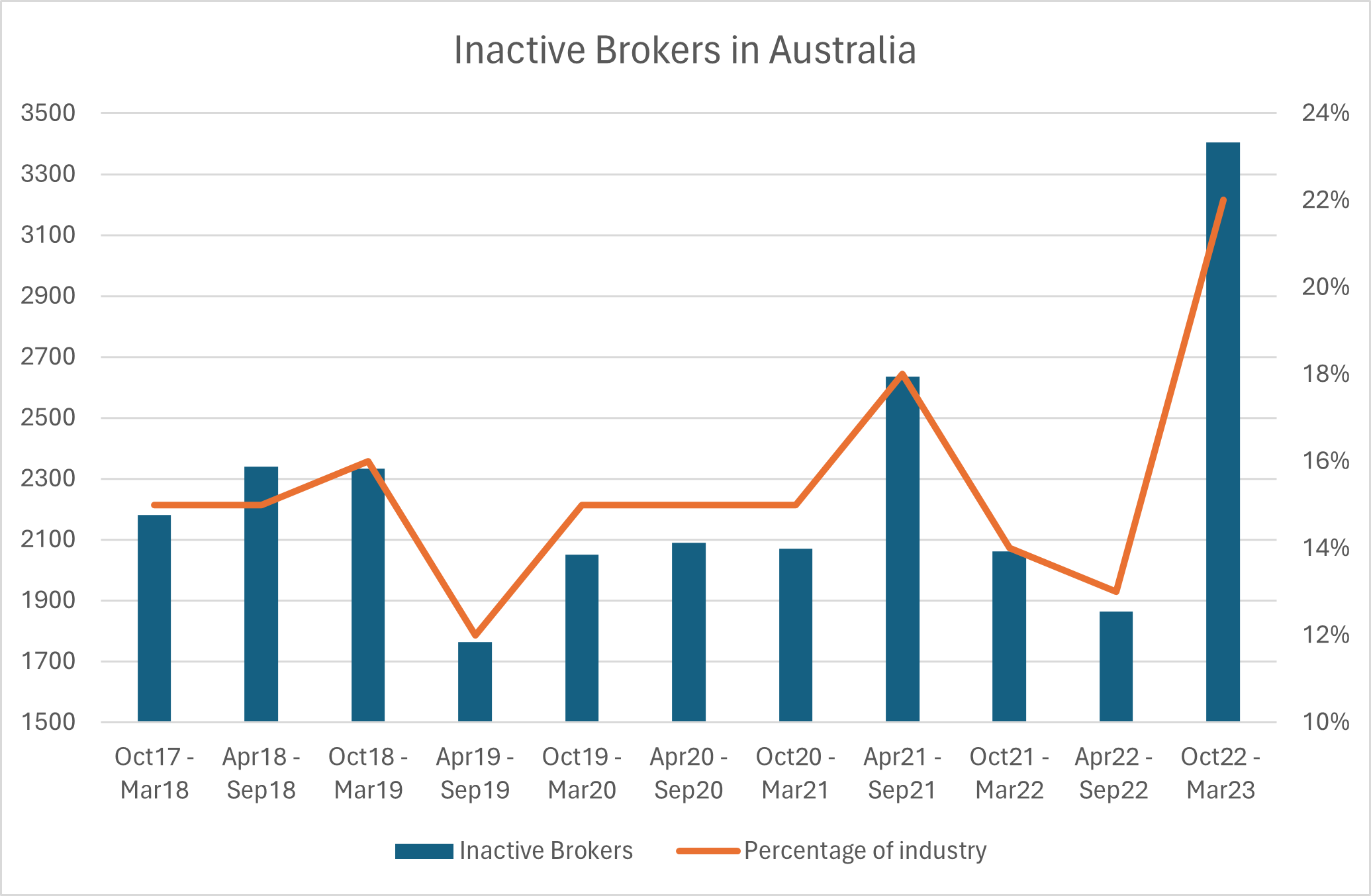

The Australian mortgage broking industry has witnessed a significant decline in activity, with more than 3,400 brokers ceasing to settle home loans during the October 2022 – March 2023 period.

This represents a staggering 22% of the broker population and marks a near-doubling of the inactivity rate compared to the preceding six months.

“This is the first time a large uplift in the cohort of inactive brokers, which has previously been fairly stable year-on-year, has been observed,” according to the latest data from the MFAA Industry Intelligence Service 16th edition report.

The report is based on information provided by 11 of Australia’s leading aggregators, including AFG, Choice Aggregation, FAST, nMB, Mortgage Choice, Loan Market, Finsure, Lendi Group, Vow Financial, PLAN Australia and Connective.

Based on data extracted from MFAA Industry Intelligence Service reports from 2017 to 2023

The surge in inactive brokers highlights the challenges facing the mortgage industry amidst rising interest rates, tightening credit conditions, and a shifting market landscape.

Matthew Whyte (pictured above), general manager distribution growth at Lendi Group, said 2023 was characterised by a remarkably low housing supply, a significant decline in purchase activity, and a higher interest rate environment that directly affected borrowing capacity.

“These market shifts really highlight the challenges brokers in the industry today face, and how important it is to be backed with technology, processes, training and a strong support model as the backbone, enhancing broker capability,” Whyte said.

This increase in inactive brokers is consistent with the decline in overall productivity observed during the period.

Mortgage brokers settled $161.79 billion in residential home loans for the six-month period from October 2022 to March 2023. This represents a year-on-year decrease of $15.28 billion or 8.63% in new loan settlements.

The last time a decline was observed was four years ago in the April 2019 – September 2019 period, according to the IIS report.

The total number of home loans lodged also decreased by 10.2%, from 382,523 to 343,524 between the two six-month periods.

The drastic increase in inactive brokers also aligns with a rising broker population, increasing to a record 19,456 in the October 2022 to March 2023 period.

The large number of inactive brokers also impacts the way industry data gets reported.

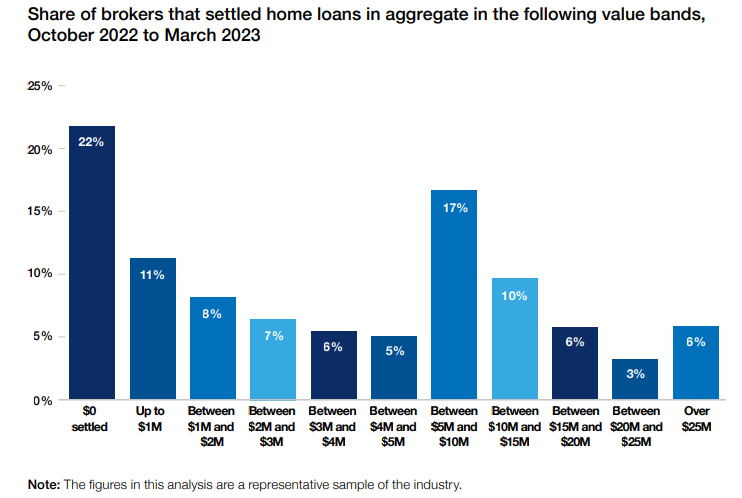

If inactive brokers were excluded and the data recalculated for their exclusion, 33.3% of brokers wrote $3 million in home loans or less, 47% of brokers wrote $5 million in home loans or less, 33.8% of brokers wrote $5 million to $15 million, and 19.2% wrote more than $15 million in the current six-month period.

Source: MFAA Industry Intelligence Service 16th edition report, 1 October 2022 – 31 March 2023

This also reduced the average number of home loan application lodged per broker, dropping from 19.9 in April to September 2022 to 17.7 in the October 2022 to March 2023 period.

However, the effects of this are not felt across all aggregators, according to Whyte, with Lendi Group increasing its market growth by 6.6% in the 2023 financial year.

“We’ve invested significantly in Lendi Group’s platform and support model – ensuring brokers have the right technology and resources to dynamically respond to such market shifts,” said Whyte.

“We’re also seeing our home loan specialists lodge four times the industry average, as a result of this model.”

The exact reasons behind the high number of inactive brokers remain unclear.

However, insights can be drawn from the MFAA IIS 5th edition report, which analysed the industry between April and September 2017.

The report attributed the high inactivity rate (16% at the time) to an increasing broker population, muted sales productivity, and volumes, falling new loan application volumes, and increased regulatory scrutiny.

Additionally, the report suggested that the “dawning generational shift” in the broker population may have contributed to the turnover.

While the market conditions in 2023 are not identical to those in 2017, some similarities exist.

The current market is characterised by a decline in housing purchase activity and a higher interest rate environment, both of which can place pressure on brokers. Additionally, the industry continues to face increased regulatory scrutiny.

However, the latest figures mark a jump that is both significant and concerning.

“We know mortgage broking takes commitment and dedication, especially for self-employed brokers, which is why we strategically recruit and partner with brokers we know are committed to the profession,” said Whyte.

“This commitment, coupled with the systems and processes in place that facilitate broker productivity, minimise the risk of Lendi Group brokers becoming inactive.”

Mortgage broking can be a tough gig – not only are they required to generate new business, but it’s crucial they nurture their existing customer base as well.

The risk to customers of increased broker inactivity is that they are potentially overpaying on their mortgage, and the risk to brokers is that their customers will simply go elsewhere.

Through the Lendi Group platform, Whyte said its brokers had easy access to the right rates and suitable products for their customers, a stream of qualified customer appointments flowing into their businesses, and a sophisticated customer journeys communications program that nurtured their existing customer base and converted cold prospects.

“These features facilitate productivity, cultivate strong broker-customer relationships, and encourage the retention of customers for life, thus boosting customer experiences and minimising the risk of broker inactivity,” Whyte said.

It’s also important to take advantage of market opportunities as they arise. Whyte said despite the market shifts, opportunity remained.

“We’ve seen this happening in refi – circa $500 billion of loans are older than five years and haven’t been refinanced – that’s a massive opportunity, and our platform and strategic marketing approach ensures our brokers do not miss out on those opportunities,” said Whyte.

“It’s much harder to leverage the customer opportunity without the right technology.”

With the exact reasons behind the rise in inactive brokers remaining uncertain, it is crucial to first understand the root causes before addressing the issue.

However, despite the lack of definitive answers, there are still proactive steps the industry can take to address the situation.

According to Whyte, a multifaceted approach is needed to tackle this challenge.

“We need a combination of strategic recruitment for the right brokers, paid customer acquisition, training and support and a leading broker platform that takes the traditional broker paperwork, admin and customer management away,” Whyte said.

“Brokers need to focus on their customers’ homeownership journey, and ensuring they are a customer for life, thus sustaining their productivity and ensuring their own success.”

Why do you think there are so many inactive brokers? Comment below.