By

Q: Brokers, what was the pivotal moment that inspired you to diversify into commercial and business lending and what do you think is preventing the large majority of brokers from doing the same?

Josh Ugo: For us there were two main reasons. Firstly, to add more value to our customers and, secondly, to create more opportunities for us. And because we took the step to understand the product, we went from being reactive to proactive, and then we were finding the opportunities. They were always there.

Mhairi MacLeod: Originally, my business specialised across asset and commercial lending and I have diversified a lot further in 20 years by picking up niche customer segments. This has given me an even broader diversification and today my staff and I collaborate to find new market and customer niches, and we do that every year. I think brokers like us who are always forward-thinking are always going to be looking for the next thing that is going to assist our clients, which will open the market to diversification.

Rob Grul: Simply because the need was there. Around 50–60% of what we do is some form of capital raising for business. Whether we can raise money off the balance sheet or we can utilise cash flow products, our customers were screaming for cash flow and we, like all good brokers, needed to find solutions. This was a happy marriage between our firm’s operations and customers’ needs.

Steve Sladek: For us it was a simple transition. Originally we provided consultancy, helping troubled and distressed entities. The other part of the business was asset finance, equipment and so on. It’s about getting to know your customer and, for us, doing consultancy as well as asset finance, we need to see full financials for the last few years, balance sheet, etc. Through that you get a very good understanding of a customer’s business and you uncover these other needs. Doing business consultancy, asset finance and now business loans, all three work really well together.

Q: What are the challenges in diversifying sources of business?

Q: What are the challenges in diversifying sources of business?

Rob Grul: Education. I was lucky enough to have an experienced Prospa BDM come into my office, sit down and educate me on how to do it. Traditionally, we have always offered a secured funding type of arrangement for our customers, whether that is leaseback or debtor finance, but someone from Prospa came and spent time with me to explain how these products fit clients.

Mhairi MacLeod: A lot of resi brokers are unable to articulate what products such as Prospa’s small business loan actually do, or they are fearful because they think it’s expensive. If someone could teach them, through a narrative, it would help them.

Stephen Hale: The skills gap and lack of experience are the main barriers we hear about at MFAA. But the fintech sector is filling the gap with the products on offer and the speed to market that they can facilitate.

Q: How are brokers being supported in order to meet these challenges?

Q: How are brokers being supported in order to meet these challenges?

Matt Bauld: Close to 70% of Prospa’s business comes from intermediary partners, and we have always understood that we need to help our partners find customers efficiently and then provide the best service possible. We regularly approach the market to ask how we can help and then respond, which has built our product, technology and trust. We have worked with more than 10,000 partners to do that; we are on aggregator panels and we work with associations. The amazing experience we deliver for customers is evidenced by our NPS, which is in excess of +77, and our industry-leading TrustPilot rating.

Q: Looking at the number of brokers who work beyond residential, what does the data say?

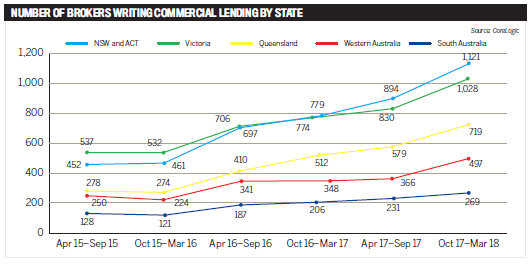

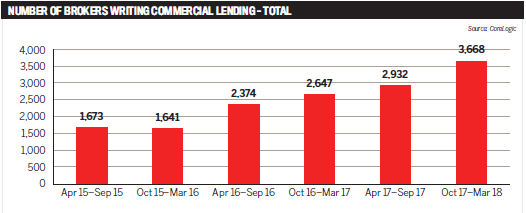

Stephen Hale: There has been a 25% increase in residential brokers writing commercial loans in the last quarter, and they wrote around $9bn in the first half of 2018. As an association, when the MFAA talks to brokers we see many start as residential brokers, and the tech-based commercial lenders such as Prospa provide a really good way for them to get into a new customer base. Because commercial is more complex than residential it’s a big challenge to step straight into. Starting with small business loans is a great way to learn your client’s needs and then look at whether it’s right for you as a broker. We don’t say it’s right for every broker, but many brokers have that ability to diversify.

Stephen Hale: There has been a 25% increase in residential brokers writing commercial loans in the last quarter, and they wrote around $9bn in the first half of 2018. As an association, when the MFAA talks to brokers we see many start as residential brokers, and the tech-based commercial lenders such as Prospa provide a really good way for them to get into a new customer base. Because commercial is more complex than residential it’s a big challenge to step straight into. Starting with small business loans is a great way to learn your client’s needs and then look at whether it’s right for you as a broker. We don’t say it’s right for every broker, but many brokers have that ability to diversify.

Q: To the non-brokers, what challenges do you see for those who don’t diversify?

Matt Bauld: Prospa has seen the greatest challenge as the question of ‘what happens when...?’

That means, if you specialise in only one thing, when the customer comes to you with a different requirement, how do you meet it?

That means, if you specialise in only one thing, when the customer comes to you with a different requirement, how do you meet it?

Stephen Hale: And if you want to keep that relationship you have to find a solution or the customer will go elsewhere.

Matt Bauld: The biggest challenges for Prospa as a lender are increasing awareness and then consideration. Most small business owners aren’t aware of and don’t understand their options. Prospa is now in its sixth year and we are investing a huge amount in education to increase awareness and ensure customers know there are options. Consideration was sub-5% a couple of years ago and now it’s reaching the low twenties. So that education is critical.

Q: What should the role of an aggregator be in helping brokers to diversify?

Josh Ugo: Aggregators host conferences with great content and they can make a broker aware of what is available product-wise, but they may not be focused on educating brokers on the mechanics of reaching a larger market.

Mhairi MacLeod: Back-end collaboration between the aggregators, brokers, and lenders needs to be tighter. But I think the role aggregators could play at PD days is in encouraging peer-to-peer partnerships, for example pairing brokers who have used Prospa with those who haven’t. The two can assist each other with the first few deals and then choose if they want to do the next one alone or with more support.

Alex Brgudac: As a lender, Prospa has had a tremendous amount of success with our partnerships, not just with aggregators but with key industry associations as well. Ultimately, we are a commercial lender, but we are about helping brokers of all sorts of backgrounds and specialties, be they residential, commercial or asset finance – all they need is access to small businesses. I am pleased to say that all partnerships we have across the industry have really embraced our approach and opened up the flood gates in terms of giving us opportunities to help drive awareness and education through to the broker base. Reflecting the recent MFAA data, we are also seeing an uplifting in new broker business, which means diversification is absolutely growing.

.jpg)

Q: What features do SME owners want in their loans?

Steve Sladek: Fast turnaround times. We deal fundamentally with small businesses, and you usually find the owner-operator of a business is very engaged with the operations, and they know they need funding but, until we come on and provide service, it’s left until the last minute. What we find from a business consulting point of view is that SMEs can be very last-minute, and when they decide they need finance they need you to make it happen fast. So timing is everything. Rate, too, to a certain extent. They do want bank rates, but we explain that it’s just not always doable. So there is a bit of an education process.

Mhairi MacLeod: Education is key. I educate my clients on the products and services as well as the solutions they are designed to provide.

Rob Grul: Small businesses are looking for approvals. When you’re talking about a business with a turnover of less than $50m, or even $20m, unless there is a copy of security they’re not getting access to funds. So probably the demands aren’t as rate-focused as some brokers expect, but I think it’s the ability to get money, and unless you’re a specialist, and we all are, customers just don’t know how to access funds.

Mhairi MacLeod: We bring them a solution, but we also bring them a get-out. We show them they are going to pay this loan off; it’s not an evergreen facility that is going to get them into financial difficulty. They have an end result and a solution. It’s a continuous example of what we do as brokers, which is educating our SME clients on how to use a product.

Matt Bauld: In Prospa’s experience, customers want to be heard. They actually want to have a conversation about the business and they want someone to understand what the business is about. Working with our partners and working alongside the business owners, we can do that.

Alex Brgudac: Speed, service and price. You never hear a broker saying “I have a small business in need of funds but have a few weeks before they need it!” Small business owners wake up in the morning and go to bed at night thinking about the cash flow in their business. Even using technology, it’s also about how to educate the SMEs on what is possible if funds were available to them.

Q: In terms of the availability of capital, what is possible in the current lending environment?

Stephen Hale: There is a tightening of credit policy at the moment, and that is worrying a lot of SMEs and commentators. Brokers must continue to provide access to new forms of lending. They have that source and access to relationships that can help SMEs, and as an association we see fast growth in the fintech sector, and fintechs filling the gap where there is a credit squeeze starting to happen.

Rob Grul: I think the banks actually created this market. Previously, a business owner saw their bank manager, did the deal and everyone was happy. But banks, in tightening up, created this market themselves – it didn’t just appear. People realised they needed options, and fintech is a perfectly viable option for the customer at this time.

Matt Bauld: I think the great opportunity here for the broker is that they, too, are a business owner, so the opportunity is right in front of them. It’s not just about solving problems; it’s about the massive opportunity in the SME market and how you as the broker grow within the financial opportunities in front of you. The more regularly you can speak to business clients, the more opportunity you will see exists.

Q: Are brokers apprehensive about fintechs and online lenders?

Josh Ugo: When I first started working with Prospa I was extremely hesitant because they had direct contact with my customer. But the first few deals went really smoothly and the customer had a good experience, so now that fear has gone.

Stephen Hale: Ownership of the client relationship is a big fear for brokers. A lot of people came into the tech lending market thinking, ‘we’re cool, we’re online, we don’t wear ties’, but brokers were hesitant because, firstly, they didn’t know how to sell the product and, secondly, they were fearful of the client being taken from them.

Brokers said to the MFAA years ago: what if these lenders go into mortgages and take the whole client’s business away from us?

Alex Brgudac: I think that one of our biggest obstacles in the early days, and to some extent still today, is having brokers trust a lender to speak to a client. It’s a big deal. Your client is everything, and historically brokers would go out of their way to ensure the lender never had that contact.

Matt Bauld: One of the big changes Prospa has made over the journey is our value proposition as a fintech and how fast we can do things; that’s a real talking point for our team. Yes, introduce your customer and we will do the work – that is one of our processes and we can do that. But at the same time, for the broker market we can deliver a service that is absolutely about working with partners to get the full application and submission done through the broker. We also offer valuable services to our partners, such as partner-branded marketing support, to help them service their customers best.

Steve Sladek: If you have a client relationship there is nothing to be scared of. If anything, it complements the client relationship you have built up as a broker.

Mhairi MacLeod: In the last couple of weeks we have had two clients go direct to Prospa, and we knew they had gone there following a courtesy call from Prospa touching base. Then my team rang the customer to ask about their experience, and we got a car finance deal out of them. So even if they go direct to Prospa, the client isn’t gone.

.jpg)

Q: What’s the future of small business lending?

Josh Ugo: I think regulations over the next few years will be the greatest change.

Mhairi MacLeod: I think as more fintechs enter the market we will see more money from overseas. Those of us who have been through the GFC remember how we were all kicked to the curb by major lenders, so I see more offshore money coming in, more fintechs, customers embracing those third party lenders that they didn’t know about, and us as brokers showing them the way. We have such an open playing field and so many amazing products to offer.

Alex Brgudac: In the US and Asian markets the fintech experience is different, so for Prospa, being the leading fintech locally, the benefit we have is that we are building a fintech specifically for Australia. The big difference compared to other overseas markets is that Australians still want to talk to a human, regardless of whether they are millennials, withGen Xers or baby boomers. We are leveraging that and providing something new for our brokers so they can join the fintech revolution.

Stephen Hale: The trend we are seeing at MFAA is a shift in brokers diversifying, and we are working with new data partners to measure how the different market shares continue to grow. When the major lenders restricted mortgage lending, the online mortgage market grew, so we expect the same thing to happen now.

Steve Sladek: The big question is what is going to happen with the major banks? They are sleeping giants: they have a large customer base and will want to keep their bigger clients. But, overall, they are going all out to retain these big existing clients, while perhaps pushing away new clients. It’s interesting to see how they will react to what is going on in the marketplace.

Matt Bauld: Change is always going to occur; it’s what you do with the change that makes a difference. The fintech revolution is happening around the world, but there is appetite for Australians to continue to talk to someone about their financial requirements. The big opportunity is to see that as an opportunity and work with customers to meet their needs