.jpg)

Non-bank lender Better Choice meets with a cohort of leading brokers to discuss how regulation, technology and customer demand for the broker channel could shape the industry to 2025

TAKING A GENERAL VIEW OF THE INDUSTRY, WHERE DO YOU BELIEVE BROKING WILL BE IN 2025?

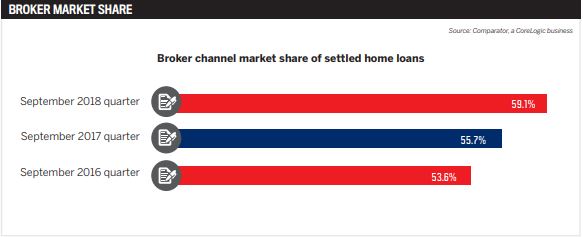

Allan Savins: I think that in terms of market share we will see it hit 60% of all new home loans originated through the broker channel over the coming two quarters, and by 2025 we will see the channel reach 75% to 80% market share.

Regardless of the royal commission, there is still a need for brokers to find the best outcomes for their clients. Borrowers still need access to finance, and it’s going to be a very complex environment as we move forward to navigate the process of getting a home loan.

Stephen Michaels: I also think brokerages themselves will change.

A lot of business will come from online platforms, with the broker popping in and out on structuring, policy and advice. There will be fewer sole traders, more larger broker groups, and more introductions through online platforms.

I predict that technology will increase, but the missing piece is that a machine can’t take over the policy aspect. That means that until someone can really make a dynamic piece of software that can put every scenario into a tick box, the broker is still relevant.

I predict that technology will increase, but the missing piece is that a machine can’t take over the policy aspect. That means that until someone can really make a dynamic piece of software that can put every scenario into a tick box, the broker is still relevant.

Peter Valentino: We are going to see a huge advancement in technology. Currently, I input or email a customer a questionnaire, which is a quasi-application. They give us their details but it requires manual formatting. I think the tech developers will create a platform where you email to the client and they will furnish all of that information electronically.

Allan: There needs to be an upskilling of knowledge. Brokers will have to become the absolute product experts and improve standards across the industry. You will still get clients who chase rate, but it’s about understanding the policies and the lenders’ assessment techniques.

The rate component is still there but probably second or third on the list compared to what it used to be.

Jaison Singh: I think it will become a more customer-centred business in which services and solutions become a lot more diversified. Probably things like budgeting advice will become key, as well as creating that value proposition and point of difference for our clients as well.

Allan: The broker needs to create deeper relationships with the client, and there are ancillary-style products and services to help the customer fulfil their objectives that I see as perfect low-hanging fruit integration. For example, you have valuation, insurance, utility connections, so if you can partner up with groups who can provide a seamless and fluid delivery – and automate that delivery – it will build a deeper relationship. Brokers need to evolve in that way, and quickly.

Darren Liu: That’s one thing we see in our business: the more we deal with the customer the more we feel like we need to be a bank. We can’t just do one loan any more; we have to comprehensively service many requirements. At each stage in the journey, we give our clients options so they feel they are being taken care of, and that is why we get repeat business.

HOW MIGHT BROKER BUSINESS MODELS EVOLVE OVER THE COMING YEARS?

Stephen: Policy and education are going to be paramount. The solo operators who aren’t seeing enough deal flow and don’t have a team to workshop solutions with will probably either amalgamate or join larger firms. Policy is so dynamic, one day a bank is lending for studio apartments; the next it just isn’t in their appetite. The larger groups will benefit from having more deal flows, more scenarios and resources.

Jaison: As a solo operator, you become a generalist, whereas in a team environment you have niches and specialists, and that’s more profitable. For example, I don’t touch superfund loans, but one of my consultants is really good at them. It’s important to identify the skill set of each person.

Lili Barron: Diversification will be massive over the coming years. For the commercial space and from a policy BETTER CHOICE IN NUMBERS perspective, it will mean that brokers will  have additional interests in real estate or insurance to add more value to their business. I think there will be amalgamation and growth across broker businesses, which means we will become very specialised in our industry.

have additional interests in real estate or insurance to add more value to their business. I think there will be amalgamation and growth across broker businesses, which means we will become very specialised in our industry.

Jaison: And you have to make sure these partners aren’t doing it opportunistically; some people will take advantage of some brokers. Diversification should have been a big part of business in the last 10 years anyway – financial planning, insurance, property, all those different avenues should have been done already. It’s only because there has been a bit of a shake-up in the industry that people are looking at it now.

Peter: The problem, I believe, is that the larger aggregators have done little to assist their brokers to diversify.

Jaison: The more experienced brokers use their aggregator as a portal, just to leverage. It’s about a business transaction with them, whereas 15 years ago it was more relationship driven; you weren’t looking at the commission splits, for example. It’s the aggregation model that has driven it that way, and that’s the key thing I think moving forward.

COULD A FEE FOR SERVICE EVENTUALLY BECOME PART OF THE INDUSTRY?

Darren: I would prefer to work in that way if possible. It will push us to a higher level of service, and we would also be able to get more stable systems and more people. We will get the clients to recognise the value of the broker by thinking “this is what I’m paying for”. And the broker can explain how they do more in return for that fee. Because there is no regulation of this, there is also no idea of what to charge.

Jaison: Fee for service is great, don’t get me wrong, but are you going to see the institutions passing on those reductions? All they will do is ramp up the mobile lending space.

Allan: If a fee-for-service model was introduced, banks would have a competitive advantage over brokers as banks have the infrastructure and cost base to subsidise any fee that is introduced.

Peter: Personally, I think the fee for service would put a lot of brokers out of work.

HOW COULD REGULATION BE TIGHTENED TO BETTER SUPPORT THE BROKER CHANNEL?

Peter: One thing I would like to see is a more black-and-white approach rather than the interpretation of regulations that we have at the moment. Even when NCCP came in everybody did it the way they saw fit. Everybody, I believe, even today, does compliance in a different way and a different format because no regulator has made it clear. Then there’s best interest – a real live case that comes back to the honesty of the broker.

Allan: Where compliance is heading is quite scary. Recent reports claim there are certain data uploads ASIC now wants to receive moving forward. That means there is no question about the level of scrutiny and data that the regulators will want from aggregators and brokers. They will be looking at more and more borrower files at a granular level, and that is where compliance is headed. Then there’s clawback. Where does that sit? Because on one side I’m hearing all this noise about best interest duties, and on the other hand we have clawbacks of two years; they are not mutually aligned. We are regulating for that 2% cohort at the end of the day. They recommend drastic changes based on a minority of people who were doing the wrong thing.

Jaison: Channel conflict is another massive issue, and it has been for the last couple of years. The problem is the majors are trying to realign their business models, but all of a sudden they are on a different playing field. Clients are given different expectations in a branch.

Stephen: From my perspective you have the associations for accreditation and then an aggregator for compliance and regulation. But there is no written guidance on how you are supposed to look after a file from start to finish. If there was one body that intervened across all aggregators and all brokers to create a black-and white checklist, it would help.

Lili: There is a lot of tidying up that needs to be done. For example, living expenses are another area that requires clarity, and that’s probably the first step I would say in terms of what ASIC might look at next. We need to know what is ASIC looking for, what is the client data they are looking for? What are we, in the brokering world, doing to work in a client’s best interest? And what is best interest in your terms? Those are the trends that we are starting to see with the new compliance reporting and heavier regulation. But the living expenses is a big thing.

Allan: In New Zealand their lender application form is essentially the same across all lenders. When I was on the MFAA National Lenders Forum the topic of a unified single application form was brought up every quarter, year after year, but every lender has their own agenda and risk department, so it didn’t happen. I feel it would help us get to that point.

IN TERMS OF TECHNOLOGY, HOW DO YOU PREDICT THIS WILL EVOLVE?

Darren: That’s an opportunity for brokers and aggregators alike. By 2025, I think the industry will be flatter because of the technology that will be available. For example, Finsure is investing a lot in its new CRM, Infynity, but if other aggregators don’t continue to invest, brokers will build their own technology. Today when I came to this discussion I could see on my phone how many customers I have in the area, and I know they are good clients that I have to visit today. So, by 2025, if aggregators aren’t ahead people will take their business.

Allan: Today you have all this technology you can potentially leverage on, and it’s up to the aggregator to open that window for you to transfer data and information, or you partner with third parties that can connect the value chain. I think open APIs are what aggregators need to be doing to assist in process improvement. When it comes to customer engagement, brokers will be looking to personalise themselves and control their front of house and design it whatever way they want, to level the playing field for lead generation and capture the client. That’s how brokers will compete with the fintechs.

Darren: I don’t think AI or technology will replace us, because we still give advice and assistance. That’s something that the technology can’t give, but we need more education to be able to continue to provide that.

Peter: We have got to learn that we are all in the financial industry, and at some point most of us were in banks or credit unions. In those environments, it’s instilled in you to get as many tentacles as you can into that one client.

Allan: The more products you give a client, the more sticky they become. But the more you open up an opportunity for your client to have a conversation with someone else, the more you’re at risk.

IN TERMS OF THE SUPPORT YOU RECEIVE FROM LENDERS IN DIVERSIFYING, HOW RELEVANT IS A BROAD PRODUCT SUITE TO YOUR BUSINESS?

Peter: The best approach I find is one application, one solution, with a number of lenders behind that… How can you ask for anything more?

Stephen: Diversity in products for our businesses is of the utmost importance. With Better Choice, you have credit-impaired, low-doc, construction lending, sharp prime lending for bankable clients. The way we all run our businesses, it’s official, professional; it needs to be seamless. Having a product suite that is behind one brand or lender adds to our service and customer experience.

Jaison: Things like your car finance and equipment, general insurances, but with a number of different funders and providers for each. It creates a point of difference.

HOW DO YOU BELIEVE THE BROKER’S CUSTOMER MIX WILL CHANGE OVER THE COMING YEARS?

HOW DO YOU BELIEVE THE BROKER’S CUSTOMER MIX WILL CHANGE OVER THE COMING YEARS?

Allan: What was a loan six months ago may not be today, given the constant shifting sands. It isn’t as clear-cut as to what a traditional prime borrower is these days.

Lili: The changes in credit reporting will bring a lot more data into play, which will determine what is prime and what is no longer prime. There will be a lot of things that come out of the woodwork in the two-year reporting, and the clients will claim they don’t remember. I think we will come to see a lot more of that in the nonbank space compared to the majors.

Stephen: Catalyst deals with SMEs and high net worth [HNW] clients, and we also get referrals from that. They are all prime clients running several businesses with good income, and taking their custom to a major bank may not be the right move because the majors don’t do applications in the name of a trust, or an entity structure is too complex or there is something quirky about their income. So, going to one bank with a diverse product suite – like a Better Choice or a brokerage with a 40-lender panel – is absolutely paramount. I don’t think the customer mix will change just from our business; more so our service becomes even more relevant because you are fitting a square peg into a round hole. It just doesn’t work.

Jaison: I don’t think there will be much of a change. We deal with a lot of people with portfolios, and I think you are going to have to have that niche lending experience moving forward to be able to accommodate those types of borrowers. And I also think we are going to see far more sophisticated client profiles. The credit scoring for an HNW client might not be as high because they are a lot more active. So how do you judge and put HNWs in the same category as a non-performing client? In reality they are a more sophisticated borrower and they know exactly what their risks are, and as long as you mitigate those risks, that’s the main thing.

Allan: For Better Choice moving forward, we have always been a price and policy taker. In other words, our funders tell us the wholesale price and underlying policy. But now we have become a price and policymaker in the context of the Goldfields Money deal. We are now able to manufacture, price and control our destiny, and that is the big development that will set Better Choice apart from the other mortgage managers, because they will always be a price and policy taker. So it goes back to how we align with our own bank and manufacture products. We are going through a migration phase at the moment, and that’s what 2019 will be, but you will find that by the third quarter of this year we will become much more aggressive in terms of the products we will have to offer, because we will have the balance sheet firepower to do so. We will have the infrastructure and ability to offer unique products and services just for certain cohorts of clients, and that is quite exciting. It isn’t going to be dull!