By

As APRA starts to hand control for investor lending back to individual ADIs, Australian Broker asks if the nation’s appetite for bricks and mortar investments is enough to reinvigorate its cooling property markets

Last month, APRA confirmed it would remove the temporary 10% benchmark on investor loan growth in favour of "more permanent measures to strengthen lending standards.”

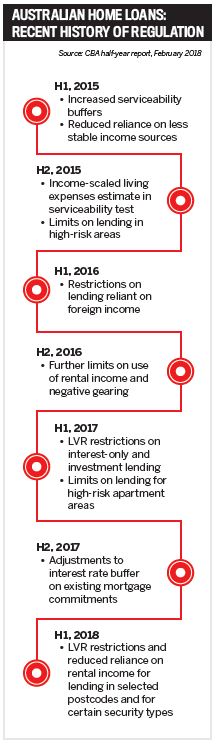

Introduced in 2014 as one of a number of actions to reduce higher-risk lending and improve practices, the removal of the cap is not an industry-wide measure. In order to comply with APRA’s growth limits, each ADI must provide assurances on the strength of its lending standards in three key areas: investor loan growth over the previous six months; policies and serviceability; and lending practices.

For APRA chairman Wayne Byres, the removal of the cap is a marker of progress, although he maintains that “there is more to do to strengthen the assessment of borrower expenses and existing debt commitments, and the oversight of lending outside of policy.”

In a statement, Byres said, “The temporary benchmark on investor loan growth has served its purpose. Lending growth has moderated, standards have been lifted and oversight has improved. However, the environment remains one of heightened risk, and there are still some practices that need to be further strengthened. APRA is therefore seeking assurances from ADI boards that they will maintain a firm grip ono the prudence of both policies and practices.”

The announcement coincides with a series of emerging trends in the house market. In Melbourne and Sydney – two cities where investor appetite drove the market to a fever pitch, prompting warnings of a bubble – a drop in buyer demand has cooled house prices, and further declines are expected. Some economists predict these will be as high as 5%, and the hard data backs them up.

Figures from CoreLogic confirm that in the last 12 months prices have dropped by 2.6% in Sydney, 4.9% in Melbourne and 2.3% in Perth, with further, albeit marginal, declines in Brisbane and Adelaide. In Sydney and Melbourne’s auction markets, the latest clearance rates are down a full 10% year-on-year.

Further, ANZ chief executive Shayne Elliott says tighter lending standards as a direct result of the royal banking commission will make it more difficult for the average Australian to obtain a home loan, placing more pressure on the investment market.

“Would [APRA’s] action be because the big four banks and second-tier lenders have seen a massive drop in investment activity?” asks Kevin Lee, buyer’s agent and mentor at Smart Property Adviser.

“With the royal commission having claimed a number of scalps after the first round of hearings, this will be interesting, as not one lending institution will dare to lower their lending standards or credit assessment criteria to facilitate ramping up this side of their mortgage book.”

Australia’s investors

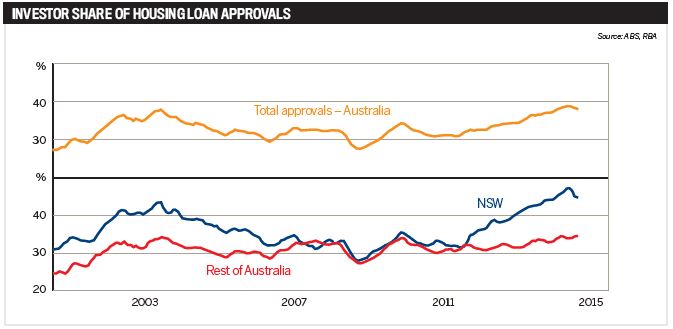

Loan approval data published by the RBA (see graph) demonstrates a strong appetite for investor loans in Australia since the early 2000s, with the market’s only previous slowdown attributable to the GFC. Approvals increased from a little over 30% in 2011 to almost 40% in 2015, with the trend most pronounced in NSW.

As much as 83% of all investment property in Australia is owned by small-scale investors – typically married couples with a high income and existing family home. CoreLogic data published in April confirms investors represent around 51% of new mortgage demand – well above the long-run average of 37% and in spite of tougher serviceability criteria and mortgage rate premiums. Demand from these investors, along with foreign cash buyers, is also driving new construction projects.

“With lower rates perhaps closer to those offered to current owner-occupiers on a principal and interest basis, the cap’s removal may increase interest in refinancing and potentially new purchases, which may see a surge in demand for investment loans,” says Natalie Sheehan, COO of Better Choice Home Loans.

Those who harbour ambitions to own multiple properties have likely seen portfolio growth dampen over the last two years. However, the stage is now set for these investors to start working towards their long-term goals once again, providing they meet new criteria around rental income, expenses and other credit obligations. Crucially, in a more complicated marketplace brokers will have an important role to play.

“Responsible lending means brokers are required to provide a loan that is not unsuitable for the consumer,” Sheehan says.

“Brokers are required to undertake a detailed fact-find and due diligence surrounding areas such as an applicant’s living expenses, serviceability and loan sustainability. Working with brokers to satisfy consumer demand whilst meeting our obligations as a lender will remain unchanged."

One emerging hotspot for investors is Hobart, Tasmania. In the midst of a housing boom that has seen property price growth rise by 17% in the past year, and an increasing number of first home buyers, demand is driven by interstate relocations and investors tempted by the high yields that can be achieved on holiday rentals and secondary properties. Figures from MyState Bank confirm that interstate buyers comprise 21% of Tasmanian house sales currently, and almost half of those are purchased as investments.

Paul Ranson, CEO of Tasmania-based Bank of Us, says, “Prior to the APRA announcement, we advised our broker network that we’ve been successful in managing our investment lending to comply with APRA’s limits and we now have the capacity for growth.”

Elsewhere, other lenders are similarly prepared.

“We have always maintained an appropriate mix of owner-occupier and investor loans, including before the APRA guidelines were announced in 2014,” says Homeloans GM of third party distribution Daniel Carde.

“Following this announcement, we will continue to originate investor loans well within our desired threshold. We are comfortable with our approach to this type of lending.”

As APRA hands responsibility back to individual ADIs, the jury is out on how this could influence the market, overall property trends and, more importantly, loan approvals.

While strict criteria will underpin the investment segment in future, historic demand shows that Australians are unlikely to step away from property investments, and the loans that fund them are only part of the story. What remains to be seen is whether the mechanisms introduced to reinvigorate the market will be enough to reheat the nation’s cooling property prices.