Small businesses are the engine room of the economy, and while the pandemic threw a spanner in the works, SMEs are now returning to peak performance. Lenders are tuned in, providing funding options for brokers and their clients.

Large employers often hog the limelight in Australia, but really it’s small businesses that should get all the attention.

Defined as those having fewer than 20 employees, small businesses account for 97.4% of all businesses in Australia, according to the Australian Small Business and Family Enterprise Ombudsman’s Small Business Counts study from December 2020.

That figure jumps to over 99% if you include medium-sized businesses, which have between 20 and 199 employees.

Small business employs more than 4.7 million people or 41% of the business workforce, making it the nation’s biggest employer. The biggest contribution by small business to GDP is in the construction sector, where it accounted for $71.3bn in value-added in 2018/19.

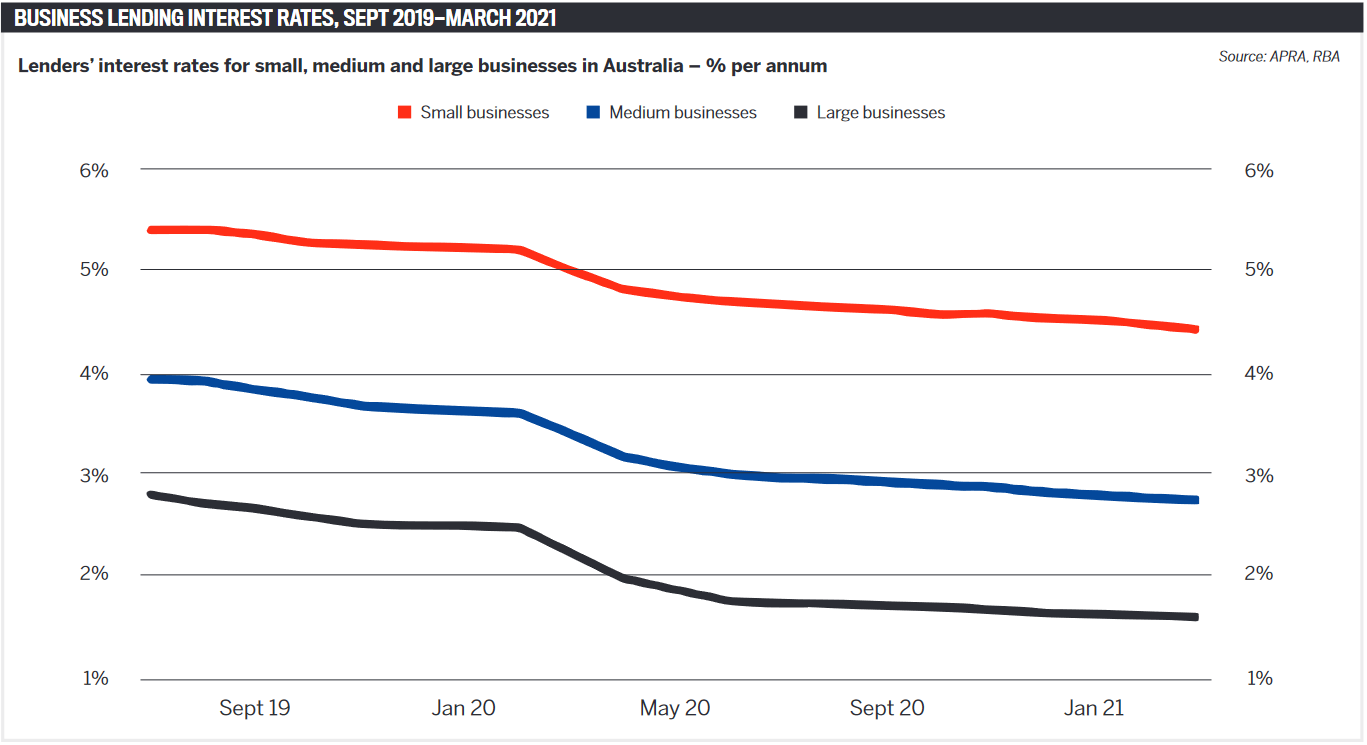

While the pandemic had a devastating effect on some SMEs, causing job losses and closures, many stood strong, and with low COVID-19 numbers, employment rising and historically low interest rates, small business operators are now looking to expand and want access to finance.

Liberty has been around since 1997, and group sales manager John Mohnacheff says the non-bank lender has a proud history of helping borrowers who don’t fit traditional lending criteria.

“Supporting small business owners is an important part of that,” says Mohnacheff. “Often with complex lending needs, Liberty recognised the benefit of bringing greater options and more flexibility for this group early on, and we were one of the first to offer specialist solutions to SME borrowers.”

Liberty recently celebrated its 15th year in the commercial lending space and now offers even more options to thousands of small business customers.

“As demand grows, we will continue to refine our product offerings to plug the gaps and support our customers’ changing needs,” Mohnacheff says.

Non-bank lender Thinktank was formed in 2006 by a group of highly experienced professionals with backgrounds in property and consumer finance and business lending.

“We could see a clear opportunity to provide simple, hassle-free commercial finance under terms and conditions not dissimilar to that of residential home loans,” says Peter Vala, Thinktank’s general manager partnerships and distribution.

He says the company’s main focus was to improve customer cash flow options by offering longer-term facilities, and remove frustrating reporting covenants, including annual reviews and revaluation requirements.

“This approach quickly established Thinktank as a leading commercial property specialist that is SME-inspired to meet the needs of brokers and their customers.

“The success of this style of lending has also enabled us to grow and widen our product offering to now include all forms of SMSF lending and residential owner-occupied and investment loans,” says Vala.

About 90% of Thinktank loans are for self-employed and SME customers, with settled loans now numbering more than 6,000.

OnDeck was set up in Australia in 2015 specifically as a lender for small business, and has since funded thousands of SMEs.

“As a small business owner myself, I had long been aware of a significant gap in the lending market,” says Cameron Poolman, CEO of OnDeck Australia.

“As a small business owner myself, I had long been aware of a significant gap in the lending market,” says Cameron Poolman, CEO of OnDeck Australia.

“Traditional banks simply don’t cater very well to the SME sector. Not only can the loan application process be arduous for small businesses, loan approvals can take weeks – a time lag that often sees SMEs miss valuable opportunities.”

He says OnDeck takes a different approach to banks, which base loan decisions on SMEs’ past financials. Instead the non-bank lender uses innovative data analytics and technology to make real-time lending decisions and deliver capital rapidly to small businesses.

“OnDeck Australia has continued to grow year-on-year, and globally, OnDeck has provided over $13bn in loans to over 110,000 customers,” Poolman says.

Commonwealth Bank looks after more than 800,000 SME customers nationwide.

CBA’s general manager broker and agency sales, Ian Burnett, says at the start of the pandemic the bank’s focus was on helping customers with the initial economic shock to ensure they had the cash flow and support they needed to keep afloat.

“We responded quickly and at scale with measures such as automatically deferring loan repayments for more than 80,000 customers,” Burnett says. “We improved speed to lending through our BizExpress lending platform, which meant we could quickly offer the federal government’s SME Guarantee Loan Scheme, and we’ve been the leading provider of loans, funding about half of all loans under the scheme so far.”

Burnett says as economic conditions improve CBA is focused on ensuring SMEs have the cash flow, products and localised services they need to rebuild and grow.

“It’s positive to see more businesses looking to invest and capture opportunities, and we’re focused on supporting their business goals.”

Moula is another non-bank lender that was established to provide loans to small businesses.

“When Moula was founded in 2013, there was a massive gap in the market, with SMEs facing a 74% rejection rate for unsecured finance, which meant too many good businesses were getting knocked back for funding,” says Sam Sfeir, head of strategic partnerships at Moula.

“Where banks were relying on legacy systems, we saw an opportunity to underwrite based on a business’s data, not their assets, while offering more personalised service. We’ve since processed tens of thousands of applications with same-day decisions, and funded SMEs with over $500m.”

“Liberty’s suite of small business loan options is second to none, and we have solutions to help all kinds of borrowers and all kinds of businesses,” says Mohnacheff.

“For those looking for funding to grow their business, we provide both secured and unsecured options. Our Liberty Mint product offers loans up to $3m, while Liberty Lift offers more flexible options up to $1m.”

“With more than two decades of experience in specialist lending, we are very comfortable working with SME customers no matter how complex the situation – we can offer flexibility that many other lenders can’t.”

Mohnacheff says Liberty was also one of the first non-bank lenders to join the government’s SME Guarantee Scheme, which has been extended to 30 June.

Liberty created its new Business Care lending product to support SMEs through the pandemic, and it also joined the SME Recovery Loan Scheme.

“Our comprehensive suite of lending products also includes competitive commercial loans which can help customers to invest in commercial property – with options to buy via their SMSF.”

As a dedicated SMSF lender, Mohnacheff says Liberty has the expertise to walk brokers through the SMSF loan process.

“One of our key points of difference is our open lines of communication. We’re proud to provide our business partners with direct access to our underwriting team.”

This eliminates “endless hours of legwork” for brokers and helps process applications with far greater efficiency and achieve the best customer outcomes, Mohnacheff says.

At Thinktank, all loans are mortgage secured with loan sizes ranging from $100,000 to $3m per property offered as security.

“This may be in the form of commercial, industrial, retail, office or residential property types,” says Vala. “We also support some specialised securities such as boarding houses, student accommodation and childcare with loan ratios up to 75%.”

“The businesses we service are wide-ranging, from the sole trader to complex corporate structures and trusts.”

Thinktank provides finance for purchases, refinances and equity release, with some of these refinance and purchase requests coming in the form of SMSF loans.

“Not surprisingly, the majority of our SMSF enquiries are from owners of SMEs wishing to run their trading business from premises they own in an SMSF in a highly tax-effective way.”

Vala says a key attraction and advantage of Thinktank loans is their set-and-forget nature.

“This saves precious time and expense for the customer, and fewer hassles, with no annual reviews or ongoing report covenants to monitor and administer. Our loans are also offered over terms up to 30 years, which provides greater flexibility, a practical feature that has been particularly valuable in recent times.”

This longer term lowers repayments, allowing customers to better optimise their monthly cash flow and still make capital reductions or accelerate payments when circumstances allow.

Vala says shorter terms can be requested, but “we prefer to see a longer term taken where possible and see the customer pay back the loan quicker if they so desire”.

Through the SME Recovery Loan Scheme, CBA is offering eligible businesses loans of up to $5m with variable interest rates from as low as 2.60% for secured loans, and from 2.85% with a repayment holiday.

Burnett says unsecured loans are available from 3.25% and from 3.75% with a repayment holiday.

“Also, our Better Business Loan is a simple loan that can be secured or unsecured with flexible repayment options and competitive interest rates. Customers can borrow from $10,000 and save interest by making special repayments which can be then redrawn at any time.

“We also have a range of solutions for smaller financing needs, including overdrafts and business credit cards.”

CBA has deep expertise across SME sectors, including retail, hospitality, health, professional services, trades, manufacturing, construction and agriculture.

“We have the scale to provide service, with hundreds of employees across customer-facing and broker support roles, and, importantly, we’re accessible across multiple touchpoints.”

Burnett says branches remain an important channel for small business customers, and CBA is well on its way to more than doubling the number of business bankers in branches nationwide by the end of 2021. “We also have a dedicated Australian contact centre for all business banking customers open 24/7, with dedicated relationship managers for larger customers and brokers.”

EFTPOS, e-commerce and innovative online banking and business insights tools, including ‘Personalised Insights’ sent directly to customers, powered by business insights tool Daily IQ, have also helped CBA meet small business finance needs.

OnDeck offers short-term business loans of $10,000 to $250,000 to SMEs with a minimum $100,000 gross annual turnover and a minimum of one year in business.

SMEs also need a business credit score of at least 500, which business owners can check by using OnDeck’s free online Know Your Score tool.

“We do not ask for security, just a personal guarantee,” says Poolman.

Poolman says OnDeck funding is used for variety of purposes.

“Our loans are also used by SMEs to buy trading stock and take advantage of terms that offer discounts for early payment. We service all industries within the SME community.”

As an online, dedicated SME lender, Poolman says OnDeck offers a simple application process, requiring just six months’ worth of bank statements, which can be uploaded in minutes via OnDeck’s secure portal.

OnDeck also recently launched its own KOALA Score™, formally known as the Key Online Australian Lending Algorithm, an innovative credit assessment system developed by its own team of data scientists.

Poolman says the KOALA Score™ uses a sophisticated blend of big data, predictive analytics and statistical techniques, as well as business and personal credit scores data from credit reporting agencies such as illion and Equifax, to support more tailored risk assessment for SME lending.

“To the best of our knowledge, no other online SME lender is working with the level of detail that KOALA provides ... this makes KOALA an important asset in allowing OnDeck to help level the finance playing field for business owners, particularly for very small or very new enterprises, and their brokers.”

Moula offers business loans of $5,000 to $250,000, unsecured regardless of loan amount, with loan terms from 12- to 24-months.

“We deliver same-day funding decisions, and clients have the ability to repay funds early, at any stage, without any fees or penalties,” says Sfeir. “Within 24 hours, we tailor finance to your client’s unique needs, helping them better seize time-sensitive opportunities. We support a broad range of industries and businesses with more than six months of trading history.”

Sfeir says Moula is up front about what it offers, quoting business loans in annual percentage rate (APR) so brokers and customers can easily understand the cost of finance before they take the loan.

“APR simply stacks up. It’s also an important aspect of SMART Box™, a tool we helped develop in collaboration with the Australian Finance Industry Association, which helps brokers and customers compare different business loans from different lenders on a level playing field.”

Moula offers two referral processes, Sfeir says.

“You can manage your client exclusively by submitting a full business loan application, or submit a referral and we’ll handle the entire process on your behalf. If you choose to submit a ‘tick and flick’ referral, we’ll work directly with your client to tailor finance to their needs.”

Sfeir says Moula’s move to flexible referrals has been welcomed by brokers with varying levels of experience.

“It makes things easier for mortgage brokers who are new to the space, who may not feel as confident with commercial lending. It also saves time for established brokers, while streamlining the process for their clients.”

Vala says not all business sectors have been adversely affected by COVID, and there are a number of areas where there has been significant growth, such as logistics and industrial property.

“We see the market continuing to improve over the coming year or so; however, when it comes to serviceability, historical financial statements may not be the best or easiest way to demonstrate capacity to pay on a new loan where the 2020/21 financial year may have been adversely affected by COVID.”

Alternative forms of income verification are useful here, says Vala, such as Thinktank’s Mid Doc offering, which draws more on an SME’s current trading performance, with one form of supporting income verification to demonstrate serviceability.

Burnett says there has been strong demand for commercial lending and asset finance, and he expects this to continue.

“Asset finance agreements have increased by about 20% in the last six months, with funding amounts increasing by about a third.

“Growth has been driven by the car market, which is up 15% in deal numbers and over 30% in amount financed. Trucks and agricultural equipment are both up over 45% in the last six months,” says Burnett.

Sfeir says during the pandemic there was reduced lending risk appetite across the board, which made Moula’s offering even more critical in delivering finance to SMEs to enable them to seize opportunity and fund growth.

“We maintained our commitment to delivering same-day credit decisions throughout COVID-19, and now are able to offer even faster turnaround times.”

Mohnacheff says the small business sector has been challenged by the pandemic, but what the market is seeing is change.

“As we enter a post-COVID world, switched-on SMEs are adapting their business models to accommodate the changing needs of their customer base and are seeking funds to do so,” he says.

“As the situation continues to unfold and we settle into the new normal, we’ll likely see things start to balance out. Some will look to return to the old way of doing things, but by and large, most business owners have found the benefits of the new business models are worth holding on to.”

Poolman says there’s a marked return to positive market conditions, growing SME confidence and an increase in SME appetite for rapid finance.

“Our Open for Business marketing campaign, launched in Q4 of 2020, reassured SMEs that OnDeck is always open to new clients, and this was rewarded with sustained growth in new loan applications from August onwards.

“In the final quarter of 2020, we experienced an increase of almost 90% in loan applications over the previous quarter, and we continue to see an uptick in SME loan applications.”

“Liberty is known for fast turnaround times, and our business partners know they can count on us when customers are in a pinch,” says Mohnacheff.

“To maintain our speedy response times, we continually measure, track and adjust where we need to. We also give direct access to our underwriting team so that our business partners can get quick updates.

“It’s an ongoing process, and we rely on many teams to work together cohesively to ensure we deliver consistently strong results.”

Burnett says CBA provides a dedicated broker-only service proposition for brokers and its small business customers.

“We work closely with them to try and make sure application forms are completed correctly and fully the first time round,” he says. “This helps us ensure the broker and customer get a decision on credit applications and access to funds as quickly as possible, and that we’re well inside the service promise timeline.”

Burnett says the bank’s ABCD Commercial lending offering continues to deliver conditional approval within its 24-hour service promise for eligible sub-$1m commercial lending transactions.

Poolman says OnDeck has always harnessed the power of technology to ensure a simple application process and rapid approval times.

“Our latest innovation is Lightning Loans, delivering turbo-charged finance of up to $95,000 to Australian small businesses in as little as two hours,” he says.

Lightning Loans’ innovations include requiring zero asset security, with just a personal guarantee, and a streamlined, efficient application process involving six months of recent bank statements to be uploaded via a secure online portal.

Sfeir says Moula guarantees fast turnarounds through its “heads and hearts” approach.

“This is about balancing the data, automation and tech with the personal, human touch,” he says.

“We leverage machine learning and artificial intelligence to deliver faster outcomes to brokers and their clients. Instead of a lengthy application process and weeks-long waiting period, ours is a fast, streamlined application, with API access to business data helping determine eligibility.”

Sfeir says technology makes things fast and easy, “but at the same time, we take the time to listen when needed”.

At Thinktank, responsiveness has always been a priority, says Vala.

“We have invested heavily over the years in a range of technological improvements to improve SLAs.

“We have also invested substantially in our relationship management team, who are always ready to assist regardless of a broker’s experience in self-employed or commercial loans. Workshopping a loan with one of our RMs is the best way to ensure a transaction has the smoothest and quickest passage through to approval and settlement.”

Mohnacheff says diversifying into small business lending can be a great way for brokers to broaden their customer base, and SME borrowers need guidance more now than ever before.

“After a trying 12 months, many small businesses are still not out of the woods financially and could greatly benefit from broker support.”

To help brokers enter the SME lending landscape, Liberty provides tailored training and development sessions with one-on-one support as required.

“With highly skilled BDMs across Australia, our team is here to walk you through the entire process, and we’re always available to answer any questions you have along the way,” says Mohnacheff.

Vala believes it makes sense for businesses to diversify their trade and supply chains to ensure continuity of income in times of change.

“A broker should really be no different,” he says. “By diversifying their income into different streams such as residential, commercial property finance, asset finance and cash flow finance they can help spread their income risk and weather market changes.”

It’s all about looking after their customer’s entire needs, resulting in a stronger relationship, improved retention and new referral business from that customer.

Vala says Thinktank is committed to helping brokers diversify, participating regularly in industry events and providing one-on-one training and education workshops.

Poolman says it always makes sense for brokers to diversify their business beyond home loans, and many could be surprised to find a wealth of SMEs already in their database.

“OnDeck research confirms that one in four of a broker’s existing home loan clients are likely to be small business owners. It makes commercial lending a way for brokers to deepen relationships with their clients, becoming a ‘one-stop shop’ for all their clients’ lending needs.”

Poolman says OnDeck not only delivers a wealth of training but its “hi tech, hi touch” philosophy means intensive BDM support, a straightforward accreditation process, and keeping brokers regularly updated with industry news and product updates.

“Importantly, the feedback from brokers who expand into commercial lending with OnDeck typically runs along the lines of ‘it is much easier than I anticipated’.”

Burnett says small businesses are the backbone of our economy, but they are often time-poor so brokers provide an important service option.

“As a service-oriented organisation, it’s very important our accredited brokers are adequately informed and trained to represent our current policies, processes, capabilities and offering to prospective small business customers.”

CBA’s innovative Broker Education Skills & Training (BEST) program is designed to ensure this is the case, says Burnett.

“The BEST program also provides an opportunity to raise broker awareness of contemporary industry issues and ensure accredited brokers understand their – and our – compliance and regulatory obligations.”

Sfeir says that in the three-and-a-half years to September 2019 the value of commercial loans settled by mortgage brokers through aggregators in Australia almost doubled.

“Through COVID-19, the case for diversification into commercial lending only became more compelling as repayment holidays depressed the available housing stock on the market.”

But Sfeir admits business lending is nuanced and can sometimes be challenging for residential brokers who are new to the space.

He says Moula’s experienced BDM team offers support through training and scenarios, including ‘Good Business Deals’, which highlight key considerations behind recent funding decisions to help educate brokers in underwriting.

“We publish regular blog content on industry issues, including a recent piece comparing annual percentage rate to simple interest rate,” Sfeir says.

“All these things help brokers better understand how we can help tailor finance to their SME clients with a wide range of needs.”