Prudential regulator APRA confirmed it will maintain the 3% serviceability buffer for new home loans, requiring borrowers to demonstrate they can handle mortgage repayments at 3% above their loan rate.

This decision adds to the challenges faced by borrowers in an already tight financial environment.

According to Rachel Wastell (pictured above left), Mozo finance expert, the buffer means borrowers must find significant extra funds each month.

“It’s like being told to set aside enough money for a big house renovation, even though your place only needs a fresh coat of paint,” Wastell said.

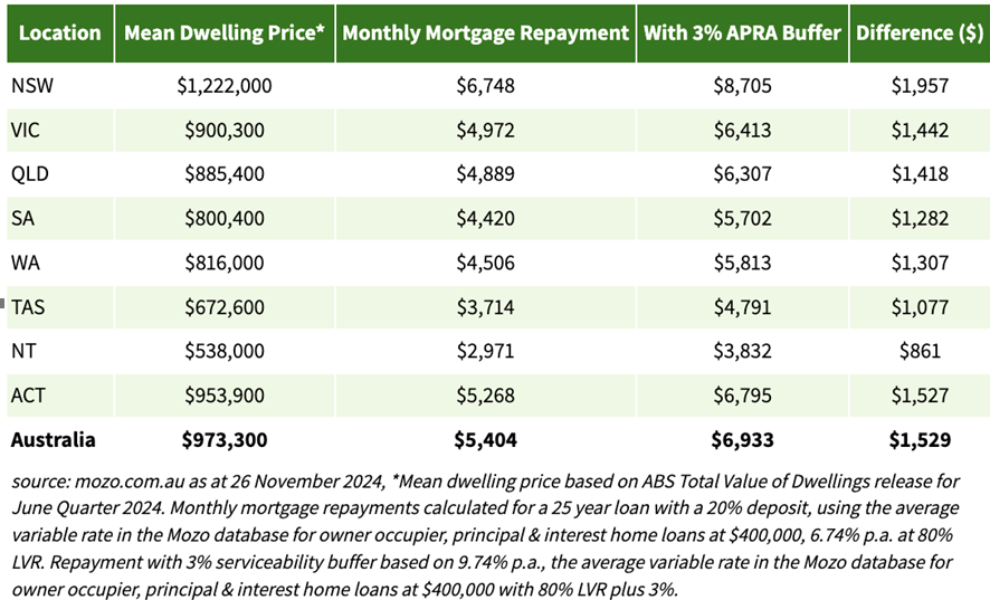

For NSW residents, based on median dwelling prices, the buffer translates to nearly $2,000 more per month in hypothetical repayments.

Despite recent rate hikes that have lifted the cash rate from a historic low of 0.1% to 4.35%, the 3% serviceability buffer prepares borrowers for a 7.35% rate – a level last seen in 1996.

Wastell noted the unlikelihood of a further 3% rate increase in the short term.

“By the time such rates materialise, borrowers would have significantly reduced their loan balances,” she said.

APRA chair John Lonsdale (pictured above right) emphasised the serviceability buffer’s role in protecting financial stability.

“It’s a contingency against economy-wide risks, whether from a rise in unemployment or an international trade war,” Lonsdale said. “This safeguard ensures our banks and borrowers remain resilient in uncertain times.”

Borrowers looking to refinance or secure new loans are advised to focus on securing lower rates.

“The difference between a low and high rate can determine whether you comfortably meet your obligations or struggle under the buffer’s demands,” Wastell said.

As the housing market grapples with high household debt and rising rates, APRA’s firm stance underscores its focus on long-term financial stability over short-term borrower relief.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.