Australian property markets have had a busier-than-usual end to winter, with more properties flowing into the market compared to the same period last year, according to the latest report from REA Group.

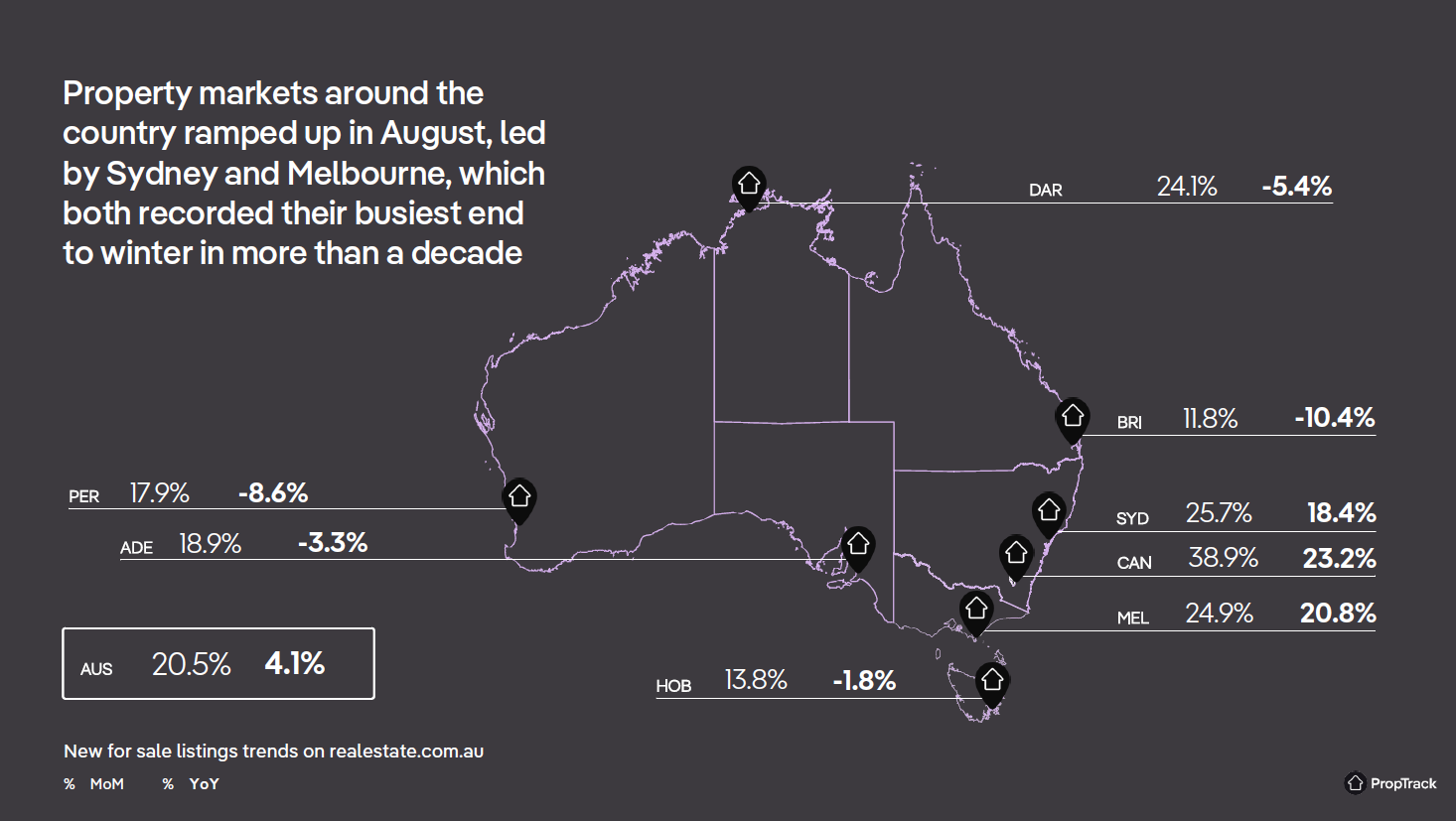

The PropTrack Listings Report August 2023, a monthly report analysing new and total listings on realestate.com.au, showed new listings on the property website were up 20.5% nationally in August compared to the previous month, and up 4.4% compared to the same period last year – the first positive year-on-year change since August 2022.

“After a quieter first half of 2023, property market activity appears to be picking up in Sydney and Melbourne, with both markets busier-than-typical in August,” said Angus Moore (pictured above), PropTrack senior economist and report author. “Activity in many other capitals has also increased but remains subdued compared to a year ago.”

Recording the biggest gains were Sydney and Melbourne, with new listings in both cities increasing 18.4% and 20.8%, respectively, compared to the same period last year.

With Sydney and Melbourne leading the increases, new listings in the combined capital cities lifted 8% in August year-on-year. By comparison, activity in regional areas ramped up ahead of spring, but with a slower pace this year than last year, at -2.2%.

According to the PropTrack report, the busier month of new listings meant an increase in the total number of properties listed for sale across Australia, which was up 5.7% in August compared to the prior month. Total listings were also up 0.5% year-on-year, providing buyers with a bit more choice compared to last year.

Moore expects activity to continue rise over the spring selling season, reaching the typical peak in October and November.

“Selling conditions and home prices have also improved compared to late 2022,” he said. “Home prices nationally have continued to recover, posting their eighth consecutive month of growth in August. Home prices nationally are now just 0.8% below the March 2022 peak. Auction clearance rates remained solid through winter and have improved from the levels recorded in late 2022.”

“The cash rate has remained steady at 4.1% for three consecutive months. While there may still be further interest rate increases, markets are pricing in only a small probability of that occurring. Inflation appears to be heading back towards target at a pace consistent with the Reserve Bank’s expectations.”

Moore added that the fundamentals of housing demand remained strong.

“Unemployment remains very low by historic standards, though it has edged higher recently,” he said. “Rental markets remain extremely tight across much of the country, and rents are growing quickly amid strong demand and limited rental availability. International migration and population growth are forecast to remain strong, which will further add to housing demand.”

Here’s where to access the full PropTrack report and more.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.