NAB CEO Ross McEwan has thrown his bank’s weight behind vaccine passports as the way out of the Covid lockdowns in Australia.

Speaking in a submission to the Senate Standing Committee on Economics, the Big Four bank chief said that Australia needed to have a vaccine pass system ready to go when national double vaccination rates hit 80%.

“Current forecasts show 80 per cent of eligible Australians will have had their first jab within three weeks, and their second jab by mid-November,” said McEwan.

“This is our light at the end of the tunnel. Our communities need hope. Our businesses need clarity, to plan for the future.”

“The National Cabinet plan states that, when we hit the 80 per cent vaccination target, vaccinated residents will be exempt from all domestic restrictions.”

“Australians need more detail on what this means and how it would work.”

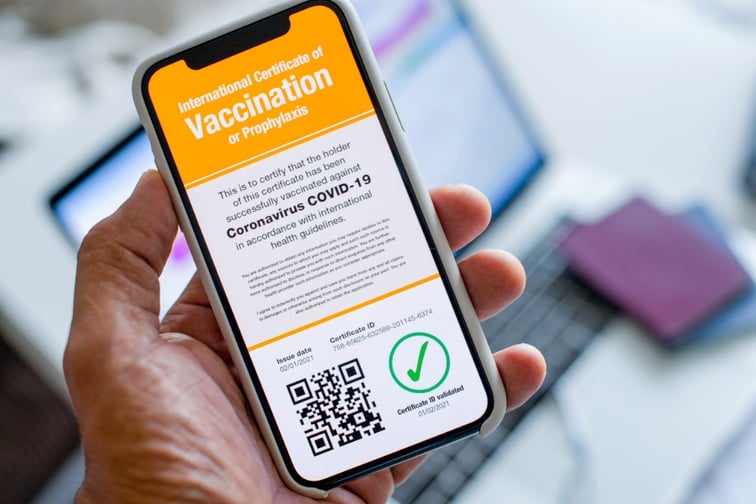

“European countries have provided this by implementing a vaccine pass, which gives people freedom to attend restaurants, sporting events, major concerts and domestic travel.”

“Australia needs its own national vaccine pass, providing similar freedoms, ready to launch when we reach 80 per cent.”

“This should be developed alongside existing plans for an international vaccine passport for Australians to prove their immunisation status overseas and on their return to Australia.”

McEwan added that, while the current lockdowns had not caused the same deep issues as last year, it was still vital for small businesses to be offered a route out as soon as possible.

“When we can safely move from restrictions to freedoms, I am very confident the Australian economy will recover swiftly,” he said.

“This series of lockdowns have not been as financially damaging for many of our customers as last year’s lockdowns.”

“Many businesses are in a state of hibernation, waiting for restrictions to open up and ready to get going again.”

“For others, in particular, small business customers in Sydney and Melbourne CBDs, the situation is more fragile.”

“The number of customers in financial hardship is rising since the Delta outbreak but most continue to be able to make some form of payment.”

“As at 31 August, just over a $1.8 billion in lending was on deferral. This compares to $58 billion at the height of the pandemic last year.”

“Our position remains that a good business before COVID will most likely be a good business going forward.”

READ MORE: Banks throw weight behind SMEG extension