In a week marked by both hikes and cuts in home loan rates, borrowers are facing a complex landscape, with a Canstar expert providing insights into these movements and offering strategic advice for borrowers navigating the current market.

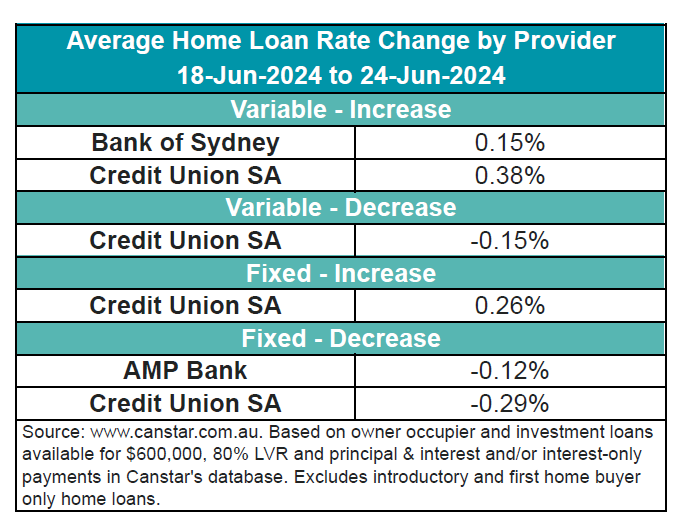

Two lenders have increased 10 owner-occupier and investor variable rates by an average of 0.29%. Conversely, two lenders have cut 19 owner occupier and investor fixed rates by an average of 0.19%.

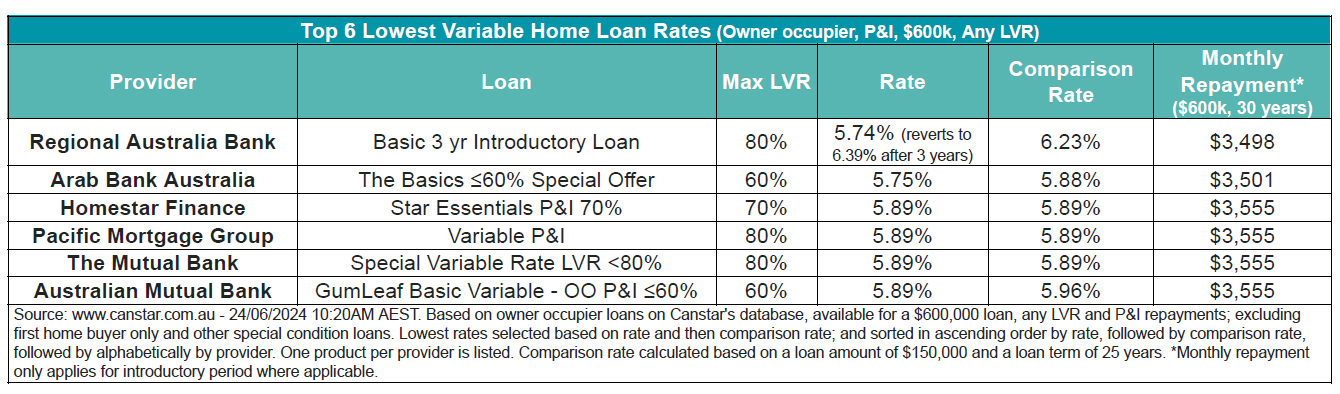

The lowest variable rate for any LVR continues to be 5.74%, offered by Regional Australia Bank. There are currently 26 rates below 5.75% on Canstar’s database, remaining steady from previous weeks.

“This week, the Reserve Bank spared borrowers from the pain of a further interest rate hike but has put us all on notice that a June quarter CPI number like the March result will put a rate increase well and truly on the radar,” said Steve Mickenbecker (pictured above), Canstar’s group executive of financial services and chief commentator.

Mickenbecker highlighted the forward-looking concerns.

“One of the big banks has already pushed its prediction for a rate cut out to February 2025, adding a further three months to the time before any rate relief, and borrowers are rightly nervous about a further increase before we see the first cut,” he said.

The Canstar expert also noted that the forward interest rate picture and risks will become clearer at the end of July when the ABS releases the June quarter consumer price index data, followed closely by the next Reserve Bank board decision in August.

Regarding strategic borrowing decisions, Mickenbecker advised considering a shift to a fixed rate, particularly highlighting the benefits of a one-year term to provide 12 months of certainty with minimal risk.

“With the best one-year fixed interest rates sitting just below the lowest variable rates, borrowers could do well to transfer into a fixed rate,” he said.

“It would be a brave move to lock into a five-year fixed rate term or even three years, but a one-year term will give 12 months of certainty with relatively modest downside that borrowers could be digging a hole for themselves.

“Even if rates fall as expected by three of the big banks, borrowers will only be paying over the odds for six months or so, making the trade-off for 12 months of certainty reasonable for the risk averse borrower.”

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.