CoreLogic’s Eliza Owen (pictured above), head of residential research for Australia, has conducted an in-depth analysis into the evolving dynamics of the housing market, revealing how traditional economic indicators have become less predictive of housing trends, especially amid the challenges of the pandemic and into 2023.

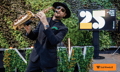

Typically, a direct relationship exists between interest rates and home values: as the former rise, the latter tend to fall, and vice versa. Yet, this well-established economic courtship faced turmoil from late 2022 into mid-2023, despite a record rise in the cash rate, as depicted in Figure 1.

“Initially, home values had a strong reaction to rate rises, falling -7.5% between April 2022 and January 2023,” Owen said. “However, by November last year, home values rebounded to new record highs. This coincided with five further cash rate increases in 2023.”

How, then, did home values manage to climb despite the rising cost of borrowing?

Other elements have stoked the market’s resilience.

“These include a strong-bounce back in population growth from mid-2022, when international border restrictions eased and net overseas migration soared to 518,000 in the 2022-23 financial year,” Owen said. “Tight rental markets may have also been at play, with unusually high rent growth and low vacancy rates prompting more people to purchase housing.”

This isn’t the first time the bond between interest rates and property values has been tested. A similar trend was observed between 2004 and 2008, during a strong economic cycle enhanced by a mining boom and rising net overseas migration, leading to a decrease in national unemployment rates. Recent data also suggested a shift towards buyers less dependent on housing loans, further diversifying market dynamics, the CoreLogic analysis showed.

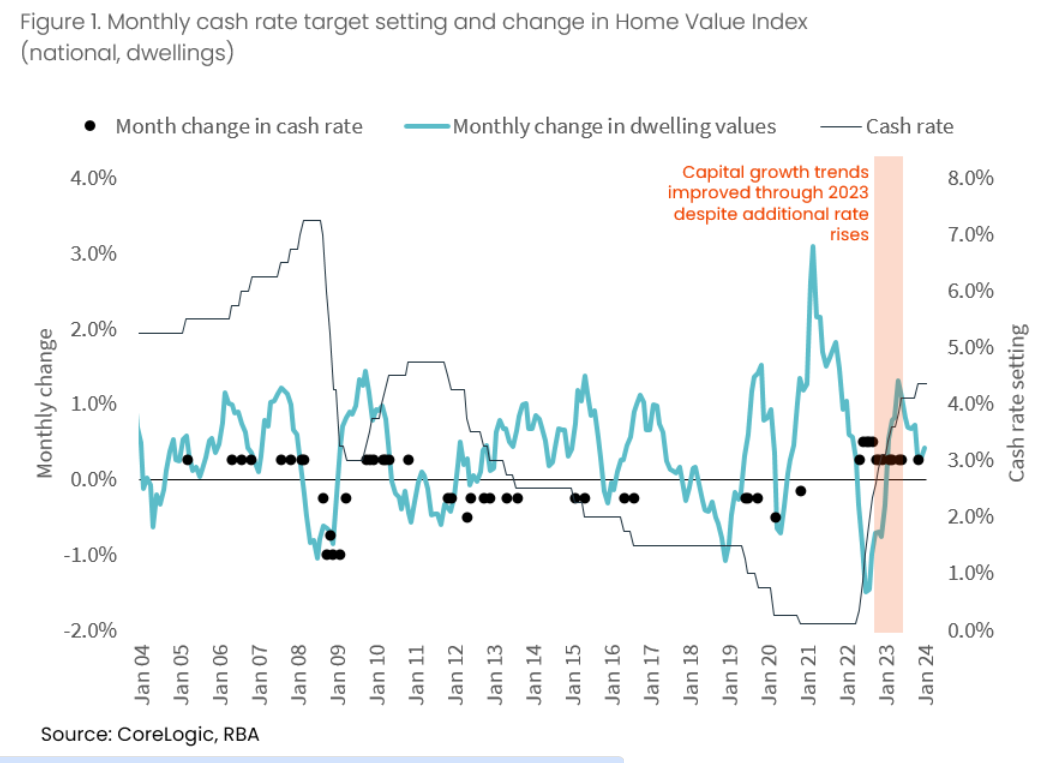

Despite 2023 hosting some of the lowest consumer sentiment indices since the early ‘90s recession, dwelling sales defied expectations. With sales volumes peaking in October 2023, the market demonstrated an uncanny resilience, diverging from the gloomy consumer outlook.

In October, 51,302 sales were recorded, a 27.6% surge compared to the previous year, even as consumer sentiment dipped by 2.0% during the same timeframe.

“The departure of sales volumes from gloomy consumer sentiment reads echoes the recovery in housing values amid high interest rates,” Owen said. “Tight rental markets, strong population growth and active buyers who are less reliant on housing credit may have played a part in pushing sales volumes higher in the spring of 2023.

“However, as with the monthly growth in home values slowing nationally, the end of 2023 did show a slight easing in the six-month trend of sales volumes.”

While the latter part of 2023 indicated a potential cooling period for housing values and sales, early 2024 shows signs of reinvigoration in some capital markets, highlighted by Sydney’s robust auction clearance rates and marginal home value increases.

This suggests that even the perception of stabilising interest rates could breathe new life into the market as we advance through 2024, Owen said.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.