According to Canstar, this past week marked significant changes in the home loan sector.

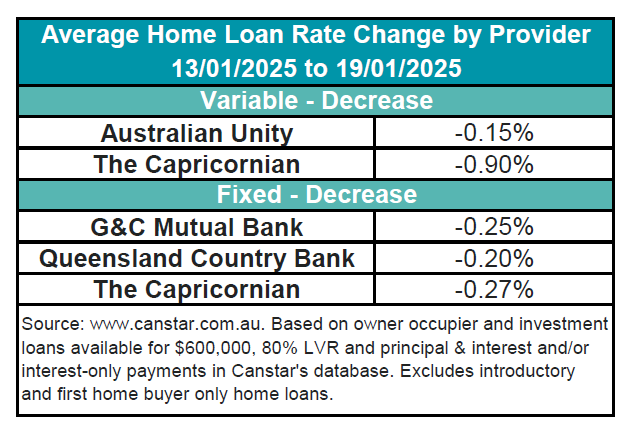

Two lenders made cuts to eight owner-occupier and investor variable rates, reducing them by an average of 0.34%. Additionally, three lenders lowered 21 fixed rates for both owner-occupiers and investors by an average of 0.21%.

Source: www.canstar.com.au. Based on owner occupier and investment loans available for $600,000, 80% LVR and principal & interest and/or interest-only payments in Canstar's database. Excludes introductory and first home buyer only home loans.

The average variable interest rate now sits at 6.83% for owner-occupiers paying principal and interest.

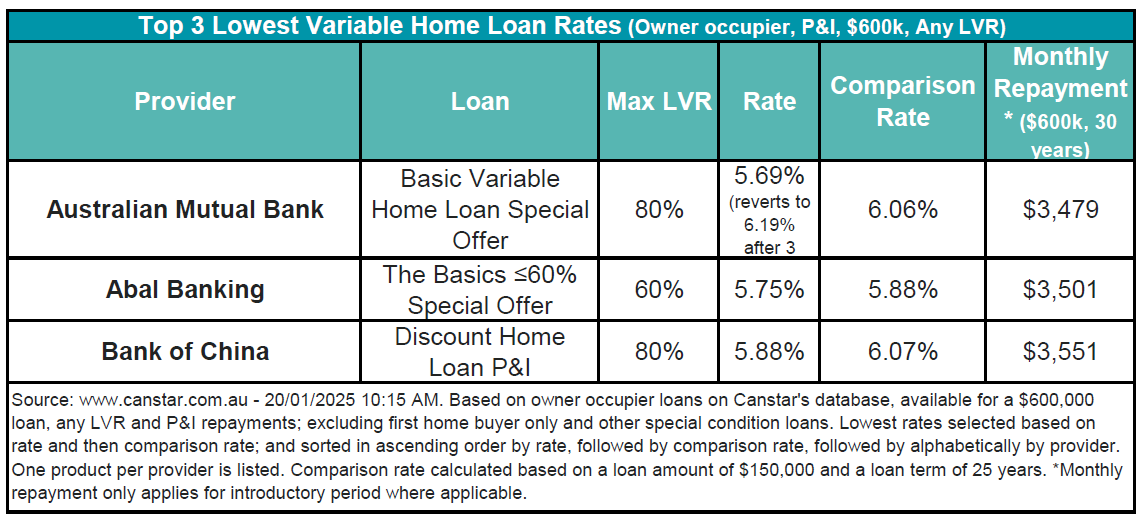

Meanwhile, the lowest variable rate available, excluding introductory rates, remains at 5.75% through Abal Banking.

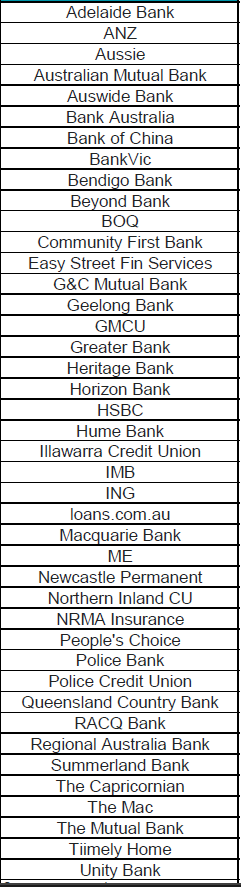

Canstar’s database currently lists 168 rates below the 5.75% mark, a figure that has held steady since the previous week. This stability reflects a cautious approach by the market amid broader economic indicators.

See table below for the list of lenders offering home loan rates below 5.75%.

Source: www.canstar.com.au - 19/01/2025. Based on owner occupier and investment loans on Canstar's database, available for any loan amount, LVR and repayment type. Based on lenders that have at least one fixed/variable rate below 5.75%.

For the lowest variable rates available on the market, see table below.

Compare the latest changes with last week’s figures.

According to Sally Tindall (pictured above), Canstar’s director of data insights, a small group of lenders initiated these rate cuts, possibly in anticipation of future cash rate reductions.

“Five lenders cut a smattering of fixed and variable rates in the last week as banks start to look forward to the prospect of cash rate cuts,” Tindall said.

“If it cuts too soon and inflation jumps back up again, then the board could have to revert back to hikes,” Tindall said.

Forecasts from financial institutions vary, with NAB predicting up to five rate cuts by mid-2026, potentially reducing minimum repayments for some borrowers by $367 over this period.

In contrast, ANZ predicts only two cuts, which would result in a smaller reduction of $151 monthly.

While rate cuts could boost the borrowing capacity of prospective homeowners almost immediately, their effect on property prices is uncertain.

The potential increase in buyer activity, fuelled by lower rates, could elevate property prices, especially if supply constraints persist.

However, economic and consumer sentiment will play a crucial role in determining whether potential buyers engage actively in the market or remain cautious, Canstar reported.

Canstar’s Consumer Pulse report highlighted that 44% of current property owners are considering purchasing an investment property within the next two years, influenced by falling interest rates.

This sentiment could drive property prices up if it translates into actual buying activity.