Despite signs that Australia's inflation peak is behind us and interest rates may be near their peak, new findings from credit bureau illion suggest that credit stress has yet to hit its ceiling.

Given that the RBA’s decision to raise interest rates aims to tighten credit, which exacerbates credit stress, the new report offers a warning that the pain will only grow if interest rates remain high.

This would especially be the case if the RBA decides to raise the official cash rate on the first Tuesday of November.

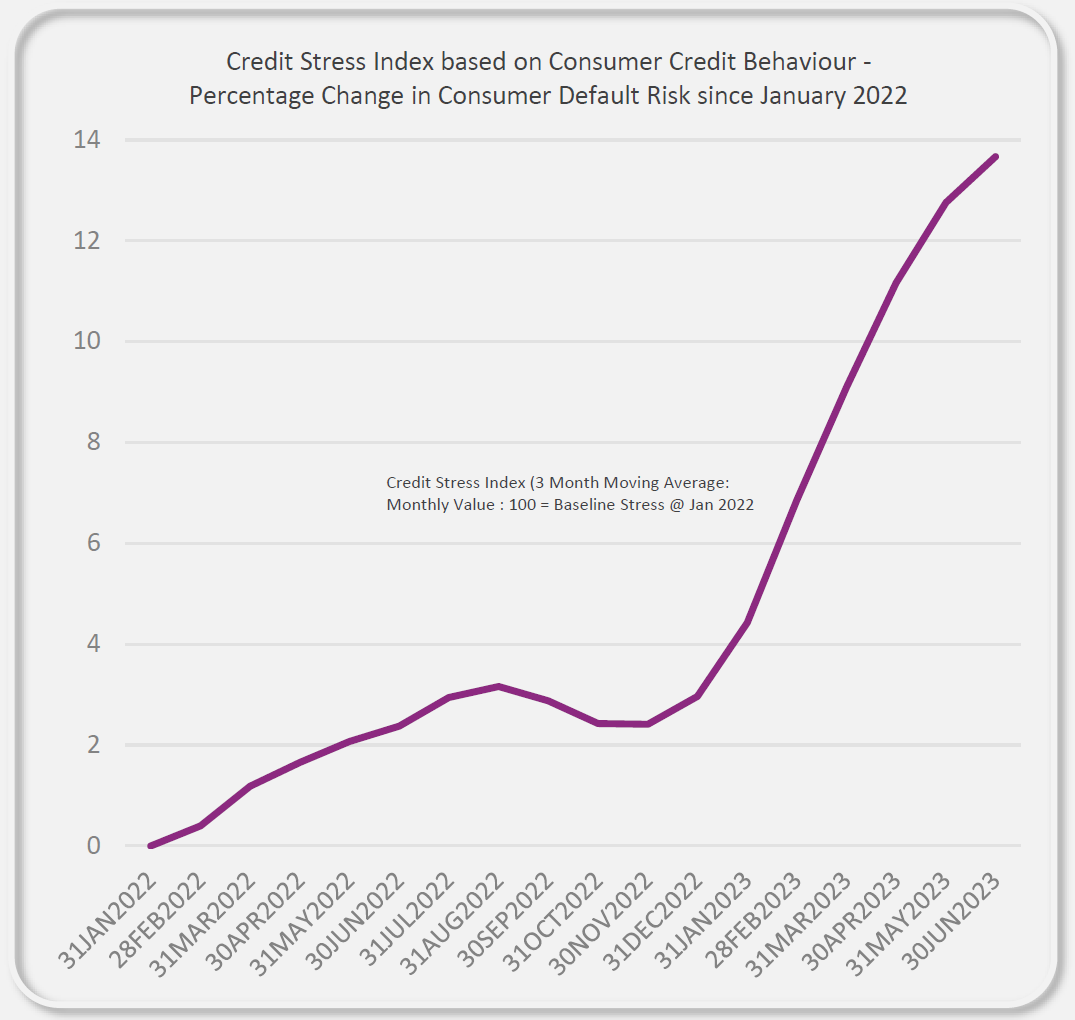

illion's Credit Stress Barometer shows that credit stress increased 11% year-on-year in the second quarter of 2023, similar to the increase in the first quarter.

“There is no real evidence yet that a turnaround in credit stress is in sight, said illion head of modelling, Barrett Hasseldine (pictured above). In fact, the current trend suggests that credit stress is continuing to climb, with no clear improvement observed as yet”.”

Overall, credit stress is accelerating due to a number of reasons, according to illion.

These include higher overdue repayments on revolving and consumptive credit (credit cards, consumer loans, and student loans), rising overdue home loan repayments, greater demand for consumptive credit, falling rates of home loans opened, higher rent obligations, and lower saving balances.

“illion’s Credit Stress Barometer suggests that there has been a large rise in credit card and home loan delinquencies, as well as rising credit card demand,” said Hasseldine.

Illion’s findings back up previous results by digital credit and collections platform Credit Clear, which saw debt files increase by 60% year-on-year and financial hardship cases rising by 25% over the latest quarter.

The latest illion barometer suggested that personal savings have also fallen significantly, but have possibly found a bottom now, with Australians unable to tap into their savings due to increased costs.

Savings balances have been depleted, falling in Q2 by an average 25% to 30% year on year, according to the credit bureau.

The last half of the year includes months such as November and December where savings are traditionally lower, according to illion, due to consumer days such as Black Friday and Cyber Monday, and then Christmas.

“Many households in Australia have limited scope for generating a surplus and we see the number of households like this increasing as credit stress continues to rise.”

Another finding from illion’s Credit Stress Barometer is that personal wellbeing is also beginning to suffer, with consumers taking on higher personal risk to help manage stretched budgets.

This has manifested in many ways such as the substantial fall in health insurance spend since October 2022, with this expense now 10% lower in June 2023 YOY.

This fall implies that Australians are choosing to drop cover, reduce cover, or increase their insurance claims excess to reduce costs.

With credit stress being felt already, all eyes are on the RBA to see whether it will raise the cash rate.

While only NAB is the only major bank to assert that there will be another rate hike before the end of the year, it has looked increasingly likely that its forecast is correct.

Two-thirds of experts who weighed in on a Finder survey on September 1 (66%, 23/35) had said the cash rate had peaked in the current rate rise cycle.

However, by the end of September, another Finder survey found the figure had decreased, with almost half of the experts expected another rate rise this year.

Perhaps most damning of all was what was revealed in the October 3 RBA board meeting minutes released mid-October, which cited concerns about the growing tension in the Middle East fuelling inflation.

“The board has a low tolerance for a slower return of inflation to target than currently expected,” the meeting minutes said.

Hasseldine said there were two main impacts that came to mind if the RBA decided to raise rates this November.

The first would be the impact on households that have interest-bearing debt, such as home loans and personal loans that are variable rate.

“The interest charges on these debts will go up, which will put further pressure on household budgets that are already stretched due to high petrol prices and other factors,” Hasseldine said. “This could lead to an increase in credit delinquencies.”

The second impact would be that a rate rise could lead to a tightening of credit from lenders.

“This would make it harder for people to get new credit or refinance existing credit. This could also lead to an increase in credit stress, as people may have difficulty accessing the credit they need to make ends meet,” Hasseldine said.

In addition to these two main impacts, Hasseldine said another rate rise could also have a knock-on effect on consumer spending.

“As households have less money to spend, they may cut back on non-essential purchases. This could have a negative impact on businesses and the economy as a whole.”

Despite inflation rates falling and rate hikes becoming less frequent, Australians should remember that, according to illion’s findings, the pain felt by the current economic conditions has damaged household budgets and may continue to do so until incomes begin to catch up.

Against this however, over the medium term, Australians will also need to guard against the ‘double edged sword’ to their finances from falling consumption if Australia falls into a recession that adversely affects their employment stability.

Irrespective, in the short term, the Australian economy may need to prepare for higher levels of credit stress, from higher credit delinquencies, if more people continue to come off fixed loans and endure higher rates of interest on their home loan.

“We are seeing the deterioration in home loans as quite striking,” said Hasseldine. “High rates could be with us for some time and credit stress may continue to build for as long as these rates are high.”

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.