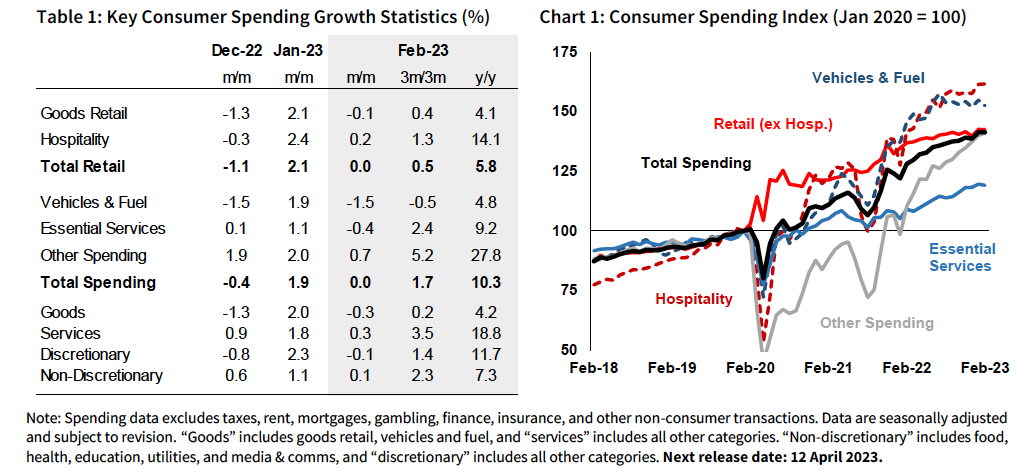

Total spending was flat in February after rebounding in January, with total spending lifting 1.7% over the past three months and 10.3% year-on-year, according to NAB’s latest Monthly Data Insights.

Retail spending was flat, with goods retail slipping 0.1% and hospitality rising marginally by 0.2%. Total retail spending increased 0.5% over the past three months and 5.8% year over year.

When it comes to non-retail spending, essential services spending dipped 0.4% month over month, and vehicle and fuel spending fell 1.5%, but the “other spending” category rose by 0.7%.

“Our monthly transaction data indicates that spending was broadly flat in February, consistent with our assessment that consumption has held up but is unlikely to be able to sustain its strong recent growth rates,” said Alan Oster (pictured above), NAB chief economist.

Goods and services spending continued to rebalance, with the 0.3% decline in goods spending month over month, offset by a 0.3% rise in spending across services. Spending across discretionary categories dipped 0.1%, while spending across non-discretionary categories lifted 0.1%.

“So far, there are few signs of significant shifts between discretionary and non-discretionary spending categories, albeit these distinctions are difficult to analyse in industry-level data,” Oster said.

Business credits were also broadly flat, up just 0.1% in February. Credits increased 7.6% from the prior year but have been broadly steady over the past few months, the NAB report said.

“While we expect inflation likely peaked in Q4, price rises are likely still contributing to nominal spending growth and, as such, the flat outcome for February implies a soft outcome for real consumption,” Oster said. “However, these data remain subject to significant seasonal effects so it will take time to get a clear read of consumption trends.”

Have a thought about this story? Include it in the comments below.