By

Jennings Mortgages broker Mitch Boulden won a Pepper Money Broker of the Year – Specialist Lending excellence award at the 2020 Australian Mortgage Awards. His knowledge of non-conforming loans helped an older couple with a credit file default buy their dream home .

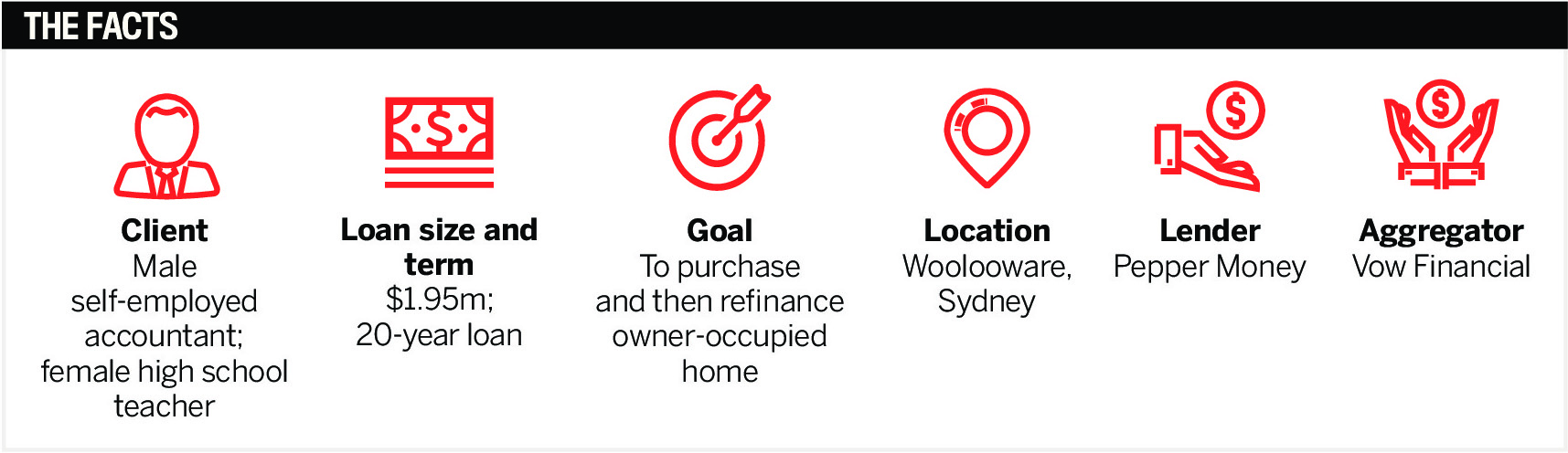

I have known and helped these clients over many years. They wanted to purchase their dream home, and I knew there would be a number of difficulties, considering their age and the man’s previous business credit history. He is 61, a self-employed accountant in a partnership, and his wife is a 60-year-old high school teacher. The couple knew this would be their last chance to obtain a property due to their age and the market not getting any easier. We knew this was going to be a tricky one.

Three years ago, my team and I at Jennings Mortgages looked high and low to get the purchase done for them. Even with 40 lenders on our panel, it fell short due to their credit file default. We knew what we had to do – get the credit file sorted and within a year they would be ready to refinance.

From our initial assessment of their credit file and current financial position, it was clear that we were not going to be able to obtain finance with any bank at that time. However, I have since partnered and built trust with private lender Agility Finance and can now be more flexible and offer greater choices for clients with non-conforming loans, including solutions over one, two or three years.

Before Agility Finance could send over the formal offer, it required exit strategies and the confidence of our team that we could refinance this deal as soon as possible, to pay back the private lender. We did our research and soon found out that we were going to have to go with a non-conforming lender if the couple took the private loan for the purchase – with this being only a short-term fix. There was also the challenge of the self-employed client’s financial position not being up to date.

We reached out and contacted all our BDMs in this space, but Pepper Money was the only non-conforming lender that would assist with this deal. The couple’s owner-occupied property was valued at $2.6m and would have a payout figure of $1.95m if they proceeded with Agility. This deal was sitting at a 75% LVR. No non-conforming lender would lend that dollar value – the maximum loan would be only $1.75m. Due to the time limit for repayment under the Agility deal, we needed to provide BAS and six months’ worth of business bank statements.

We have been valued brokers working with Pepper for the last 18 months. I was able to write up a great proposal to ask for an exception on the loan limit. Our positive selling point to Pepper was that “the client is an accountant and plans to work to age 80, and there’s been consistent strong growth in BAS over the years”. We requested the BAS statements and organised a business valuation of what his book would be worth to provide the lender with further assurances. Pepper Money agreed and made an exception to lend $1.95m at an interest rate of 5.29% over 20 years.

This meant we were able to secure the property purchase through Agility. We then started the application for a formal refinance approval with Pepper. Our clients had a long-term goal, and they believed in our team. They never imagined that they would have their dream home, as well as the positive outcome of further savings. Our clients are so happy – we are continuing to work with them to reduce their rates with our final refinance to a major bank and save a further 2% to 2.5%.

I have learnt from my early days that 99% of the time there is a solution and a step-by-step process to help your clients.I hate losing a deal, especially when it’s in your hands and the clients are relying on you. You can’t be narrow-minded, focusing on the lenders and the options available to you on your own panel. You might have to look outside the box for a solution. You need to know how to sell the deal to a bank/private lender, explain the timeline of how much it will cost, the timing of each stage and then the final savings.

Be open and honest and build rapport with your client. Explain how the lender works – it’s not the client’s job to know. The main takeaway is that I really didn’t think we were going to be able to help, but if you don’t go the extra mile and ask questions of your BDMs and explore other resources, you will never know. If you aren’t playing in the non-conforming space, you need to be. The world is changing, and brokers need to have more and more options up their sleeves. Non-conforming loans are becoming more common, and brokers need to have the knowledge to offer the right solutions for their clients.