By

Chris Howitt is an experienced mortgage broker at Port Melbourne who has worked at Mortgage Choice for more than 16 years. He assisted a single mum who was struggling to secure a construction loan so she could build her first home.

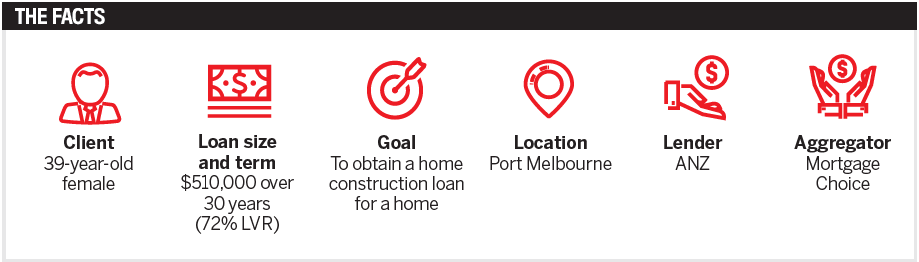

A 39-year-old single mother was trying to buy her first home through an owner-occupier land and construction deal but couldn’t get lenders to approve it due to serviceability issues.

Having been declined twice for a construction loan through another broker, this client felt like she would never be able to build her dream home, let alone buy a home at all.

She was a PAYG employee, received maintenance income for four children, as well as the Family Tax Benefit (FTB) A and B. Her parents were gifting her funds to pay part of the deposit, and she qualified for the $20,000 First Home Owner Grant. She was asking for a $510,000 loan over a 30-year term at a 72% LVR.

When I heard about the client’s predicament from the first broker, the reasons for her being declined all seemed circumstantial to me – and specific lender policies appeared to be the only hurdle. I was keen to be referred and to speak to the client because I knew immediately of a lender (ANZ) that would most likely understand her situation.

After meeting the client and obtaining more supporting information relating to her income payments, we soon identified the potential hurdles.

One issue was the age of her four children. They were all aged over 13 years, and many lenders simply won’t recognise income payments once children become teenagers; however, they continue to classify them as an ongoing expense.

It turned out that one of the client’s children was over 18, working, and no longer a dependant, but the mother was in the process of removing the child from Centrelink in relation to the FTB. It was enough to create potential issues, as lenders still saw this child as a dependant and an expense.

Separate to this case study, I’ve seen a scenario in which a father only saw his teenage child on a Saturday night once a fortnight. The bank wanted to expense the child as well as the father’s maintenance payments (a double up), and this led to his loan application being declined.

Thankfully, when talking to the right lender, they put the maintenance payment down as an expense and didn’t expense the child. Teenagers are not likely be an ongoing expense over the life of a 30-year loan, but not all lenders recognise this in their policies.

Back to the single mum. Another issue was that she was salary sacrifi cing in her current employment. So, when it came to her income assessments, lenders were taxing her full pay, and this became less income to use, as opposed to taking into account her overall net income.

This is where it’s important to have access to a database of lender policies. I knew that ANZ considers the issue above more sensibly. It does not consider a child’s age when assessing maintenance and FTB payments. I was also aware that the bank assesses net income, allowing for things such as salary sacrificing. I always knew that lender policy was going to be critical to my recommendation.

Once the deal was approved, the client was in tears. She will be moving into the home this month. I’ve just submitted an application to increase her mortgage by another $40,000 to vary some of the construction and give the client some extra money for landscaping.

The most important takeaway is really having good knowledge of all the policies of lenders on your panel. Mortgage Choice has a Lending Centre Toolkit that displays all lender policies in one place and is searchable by keyword, meaning you can easily get to know how lenders treat certain circumstances.

You should also be prepared to do your research for your clients prior to making your recommendation. I often tell clients with more complex deals that researching the specific details of their loan application may take a week. It’s also good to communicate with the client about what documentation and details will be needed so they understand what you’re doing and why.

It is critical when in doubt to run the scenario past your lender BDM, other brokers in your o ce or your network, or your aggregator’s credit team. Furthermore, it’s essential to have clear notes to present to the lender and BDM. In this case, you wouldn’t want to miss that the client receives income for a child but the child is over 13 years of age. Every little detail matters.