By

Due to the changing lending landscape, there is a strong demand for private funding in Australia. Kevin Wheatley explains to Australian Broker how this could impact brokers

Founder of Sydney-based Bayside Residential and Commercial Mortgages Kevin Wheatley works predominantly with clients from across the globe to deliver and maximise investments in property development.

He established the company back in 2009, bringing to it years of experience as a logistician by trade, having worked on projects such as shipping ports and waste-to-energy facilities.

During his time as a logistician, Wheatley – one of MPA’s Top 10 commercial brokers for 2019 – says he developed a passion for the financial industry and the way it could make a difference to people’s lives.

He says: “In logistics, there’s a very high level of procurement, and procurement requires funding."

This led him to take a natural step towards offering financial services.

“I’ve taken Bayside Residential and Commercial Mortgages from a one-man operation to what it is today, and this is just the beginning,” Wheatley says.

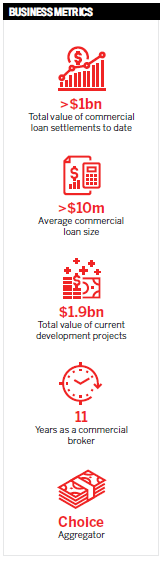

In 2018, the volume of residential and commercial funds that came through Bayside totalled $249m. The volume for 2019 is also estimated at around $200m.

Wheatley is also currently looking to provide about $1.9bn in development funding for three projects in Australia, including one in Port Melbourne and another major development in Cronulla.

“Our core focus this year will be on raising the capital required for AusCity Capital, to take it to the next level,” he adds.

AusCity Capital is the private business arm of Bayside Residential and Commercial Mortgages. It aims to provide debt funding for construction development, stable income-producing properties, unlisted and listed property securities, cash and fixed-income securities. It gives investors access to premium construction and development projects that are not available on the public market.

Access to private debt

Wheatley explains that because banks are applying unyielding disqualifying criteria, such funding opportunities are usually fulfilled by non-conforming lenders who offer premium rates and fees to their clients, knowing that institutional lenders are rigid in their financing requirements.

Wheatley explains that because banks are applying unyielding disqualifying criteria, such funding opportunities are usually fulfilled by non-conforming lenders who offer premium rates and fees to their clients, knowing that institutional lenders are rigid in their financing requirements.

But through the establishment of a debenture issuing company, he says the AusCity Capital fund is able to raise private funding for strong projects with time-sensitive needs, as well as those projects that have been unable to raise funds from banks due to overly prudent regulation stemming from the royal commission.

“Our investment vehicles allow us to compete with non-conforming lenders by offering commercial mortgages to institutional clients at more competitive rates,” he says.

Another key focus for Wheatley is on AusCity Capital eventually becoming a non-bank.

“Non-banks are here to stay. There’s demand now more than ever because of the lack of competition that’s been in Australia, allowing the big four to monopolise the industry,” he explains.

“What has been found by the royal commission now is only the tip of the iceberg … you’ll see a lot more class action cases in the courtrooms this year because of banks’ misleading and deceptive conduct.

“If anything, this has given a lot more credibility to our business, because we’re the ones now that are constantly finding an alternative funding solution for disgruntled borrowers.”

He adds, “The private funding opportunities are going to be there for a long time.”

However, Wheatley points out that his business could be negatively impacted if the government was to go ahead with plans to scrap trail commissions.

The future of trail commissions

The biggest threat to Australian brokers is going to be the disruption that will come as a result of the 76 recommendations made by the Hayne royal commission, suggesting a crackdown on mortgage brokers.

Wheatley says, “Josh Frydenberg, the treasurer, is proposing that by July 2020 he is going to cut trail payments. Do you think that’s not going to be detrimental to the industry?”

Trail payments are designed to cover the time that brokers spend keeping an eye on their borrowers. “Because we want to make sure the borrower stays with the bank,” explains Wheatley.

“Commission payments are not worth nickels and dimes; my residential division actually loses money because of the time it takes to process home loans, and you get very little remuneration for it.

“So if we have to rely on upfront commissions, which they’re talking about cutting back as well, to a fee for service, no one’s gonna pay that.”

This is a complete backflip to what Frydenberg said in the lead-up to the elections, Wheatley says.

“That’s going to be the biggest disrupter in the industry over the next six months, and we are preparing for that now.”

But for borrowers, he argues, it is cheaper to keep making trail payments than to carry the fixed costs of banks, which will have to find alternative resources to the third party channel.

“If they cut trail payments, there will be three people here [in this company] that won’t have a job. We can’t survive on commissions alone,” he says.

“The government has not spent enough time talking to the industry leaders.”

Instead, Wheatley says what is needed is a two-year moratorium period for the government to consult the industry across the board.

“These people need to come back to the table and talk to us,” he says. “This will impact the whole broking industry, because they won’t be able to afford to operate. Where will their cash flow come from?

“It takes some two to three months to do a home loan, so how do we pay our staff and provide the services that the Australian community now expects?”

The only way to find a pragmatic outcome will be on the back of sensible discussions and, hopefully, by negotiating a result that’s going to work for the entire financial industry.

Looking ahead

Aside from new regulations and proposals to scrap trail commissions, the year ahead is “looking really exciting”, Wheatley says.

“Not only with the development that we’ve got here in Australia but the projects I’ve got offshore; I pick the eyes out of what I want to do offshore. Because you could end up wasting a lot of time.”

So, in between raising capital for major construction projects in Australia, the company will also be providing logistics support for a new waste-to energy plant in Phnom Penh, Cambodia.

“We’ve already started, and it will take about two years to complete,” Wheatley says.

Another reason 2020 could be an exciting year for Wheatley is that a number of venture capitalists in the US have expressed a strong interest in AusCity Capital’s fund.

“We’re really excited about where AusCity Capital is going and the interest it has attracted,” he says.

“It will be a very niche managed investment trust where we are going to handle the projects we fund directly with the capital we raise, primarily from our high-end borrowers – those that we have been working with for years.”

“These financiers really have the capability and capacity to start a project and finish it, whether that is property development or infrastructure – projects like the waste-to-energy and port facilities.”

In the Australian market, Wheatley expects to see steady economic growth and opportunities as the nation heals from the devastating impact of the summer’s bush fires.