ThinkTank’s latest market focus underscored a largely stable landscape across Australian residential markets, albeit with noted exceptions in Melbourne and Sydney.

Despite recent downgrades in these key capitals, the overall market sentiment remains cautiously optimistic.

Anticipated interest rate cuts early in the year are expected to positively influence real estate values, suggesting potential recovery in these cities.

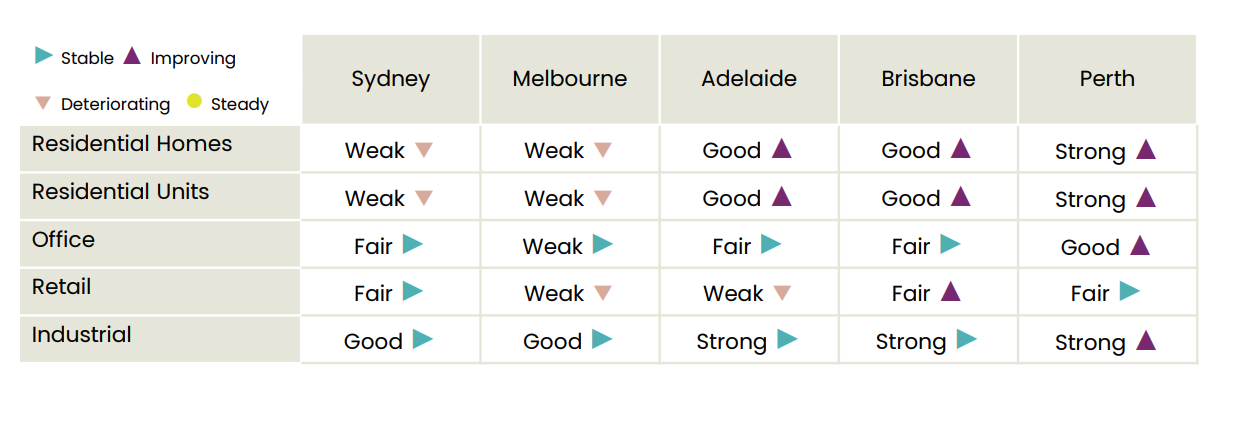

The current market ratings hold steady, with a distribution showing 7 ratings as Good, 6 as Fair, 5 as Strong, and 7 as Weak, reflecting varied performances across sectors.

CoreLogic data for January indicated a mixed performance across the national housing market, with a slight national decline of -0.3% for the quarter but remaining flat for the month.

Both Sydney and Melbourne continued to experience declines, with Melbourne seeing a -2% drop for the quarter and -0.6% for the month, while Sydney, which is poised to become the focal point of Australia’s BTR sector in 2025, reported a -1.4% quarterly and -0.4% monthly decrease. Melbourne’s annual performance also weakened, showing a -3.3% decline, placing it fifth in median home values among major capital cities.

The ThinkTank report highlighted a split in market dynamics, with improving trends in nine areas – primarily smaller capital cities’ residential sectors – and deteriorations noted in six areas, including both Melbourne and Sydney’s residential markets. This dichotomy illustrates the uneven impact of current economic factors on local real estate environments.

In contrast, Adelaide, Perth, and Brisbane have shown robust growth in both houses and units, leading the capitals with strong monthly, quarterly, and annual gains, significantly outperforming the national average growth of 8.3% over the past year.

The Reserve Bank (RBA) is poised to potentially reduce interest rates at its upcoming meeting on Feb. 17 and 18, following a period of stable rates throughout 2024.

Recent economic indicators such as a 2.8% favourable CPI for the last quarter and a gradual increase in retail sales support the optimism for a rate cut.

This potential shift comes as global central banks show a trend towards lowering rates, setting a backdrop for possible economic stimulus through eased monetary policies in Australia.

As the market navigates through these complex dynamics, the potential for lowered interest rates could catalyse significant shifts, particularly in underperforming areas like Sydney and Melbourne. With the economic landscape at a pivotal point, the upcoming decisions by the RBA will be crucial in shaping the trajectory of Australia's housing finance sector into 2025.