By

It's often said in property circles that the market is operatingat two speeds: one subsection is powering ahead and recording solid growth, while another is experiencing sluggish growth or perhaps none at all.

When Sydney and Melbourne experienced booming market conditions in recent years, it was the perfect demonstration of this. While the capital city property markets surged, and APRA stepped in with heavy-handed policies and regulations to prevent a massive bubble, other markets such as Perth, Adelaide and Darwin struggled to gain any price momentum.

Narelle Kerstan, Gloss Finance

Narelle Kerstan, Gloss Finance

“I’m the typical mortgage broker that is too busy working in the business to work on the business, so I thought, this is an opportunity” Narelle Kerstan, Gloss Finance

When this ‘two-speed’ trajectory is at play, it’s often capital city markets reaping the rewards, while regional areas are on the back foot. But in 2020, as the COVID-19 crisis continues to evolve, it seems that regional Australia is in a position to ride out this pandemic on a more solid footing.

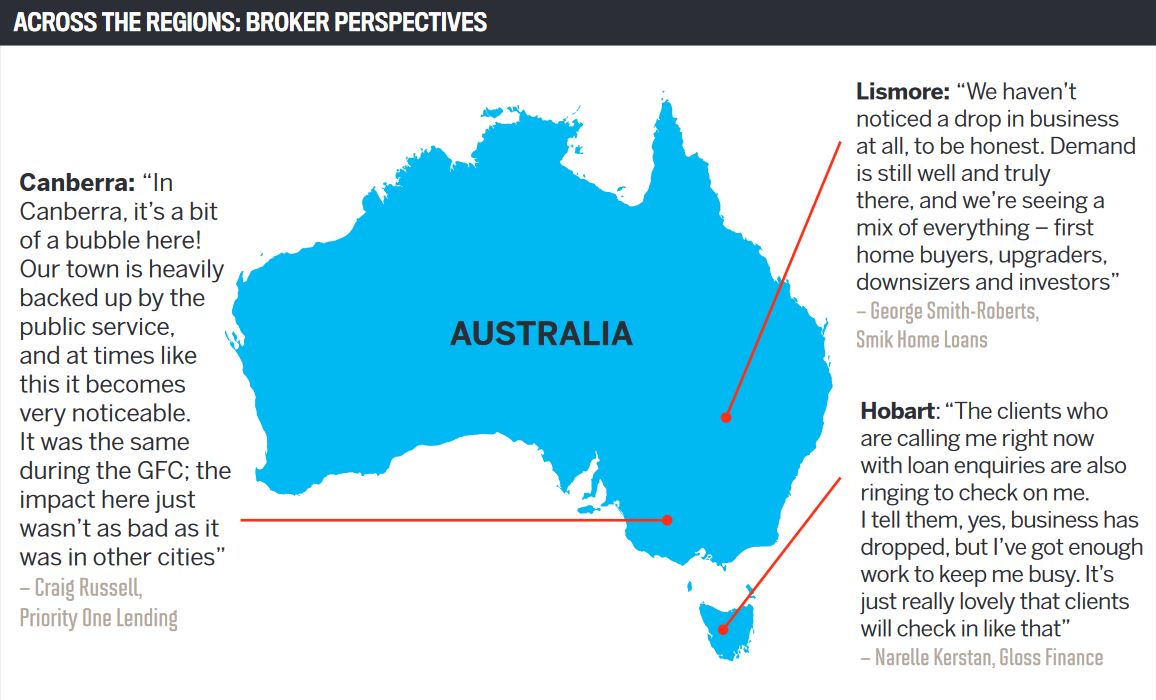

George Smith-Roberts, the Broker of the Year – Regional award winner at the 2019 Australian Mortgage Awards, runs his brokerage, Smik Home Loans, out of Lismore, NSW, where he says business has been booming in the last couple of months.

“We’ve been extremely busy. We’ve got plenty of sales coming through, so it’s not just refinancing, but we’re in a different position being regional. People here are signing up for a lower-value loan, and when loans are smaller, people are a bit more confident about their capacity to repay,” Smith-Roberts explains.

“Our average loan size is around $280,000 to $350,000, and the loan repayments on a loan like this are around $300–$350 per week. This is a lot easier to manage on one income, and people who are picking up the government benefits like JobKeeper and Jobseeker are able to get by a little easier than others [in capital cities].”

That’s not to say there aren’t people struggling in the country towns; every corner of the country has been impacted from an economic perspective, and where Smith-Roberts is based in Lismore, inland from Ballina and Byron Bay on the northern NSW coast, it’s no exception.

“We’ve had a small percentage of people requesting information on loan deferrals and hardship options, but given that our loan sizes are much lower, they’ve been a lot easier to manage,” he says.

A similar situation is emerging in Canberra, says broker Craig Russell from Priority One Lending.

In the first few weeks when uncertainty was high and there was speculation that the economic shutdown might linger for months, confidence was low, and Russell’s team spent plenty of time helping panicked clients assess their financial situation.

But there was another group of borrowers making contact: those who could see some opportunities brewing and were keen to get into a position where they could take action.

“I would say for the first two to three weeks, around half the calls I was getting were from people who were in trouble. They had lost their jobs completely or had a significant drop in income – one of my clients is a pro golfer and he was meant to play the Japanese tour, but that’s obviously not going to happen, so it was about helping these clients get clarity,” Russell says.

“The other 50% of enquiries were from people who could see opportunity. They wanted to take advantage of the share market, for instance, so they were looking to refinance and restructure to borrow extra money. People are always positioned differently, and while the cafes and the shops are closed, our client base is not retail or cafe-based. It’s professional-based, so we’re busier than we’ve ever been.”

Russell says enquiries are coming in for a range of funding requests, from residential and investment loans to commercial, cars and asset finance.

George Smith-Roberts, Smik Home Loans

George Smith-Roberts, Smik Home Loans

“People here are signing up for a lower-value loan, and when loans are smaller, they are a bit more confident about their capacity to repay” George Smith-Roberts, Smik Home Loans

“There’s been quite an uptake in people wanting more money overall, as our employment market is quite strong – it’s the medicos, the professional space, the public service, so they’re earning money and they’re sitting around at home, thinking, ‘I must get that done’, or ‘should we look at renovating?’” Russell says. “By the same token, I have spoken to a couple of brokers who are single operators without staff in Canberra, and they say their business has fallen off a cliff. Speaking to our aggregator, he said that in some parts of regional Australia all activity has stopped, and there is nothing going on. But in other parts of Australia some people are busier than they’ve ever been. The pandemic is hitting differently in different areas.”

Russell adds that his main focus is to demonstrate to clients that he is “more than just a transactional broker”.

“It’s hard to put a finger on why [some Canberra brokers are more successful than others], but perhaps for me, it’s because we have such a strong referral network. Almost 80% of our business comes from referrals, so that’s helping to keep things moving forward and keep the momentum going.”

Bradley Quilty, Tungsten Home Loans

Bradley Quilty, Tungsten Home Loans

Another broker with a large number of clients in Canberra, Bradley Quilty, director and finance manager at Tungsten Home Loans, also reports that business is coming in. Though he works out of an office on the Gold Coast, he built his brokerage in the nation’s capital and continues to service a client base that is largely settled in the ACT.

“Activity hasn’t dropped for us – in fact, in March we were busier than we were in February. It doesn’t make much sense really!” Quilty says.

“I’m sure at some point there’s going to have to be a decline; there are going to be businesses that are not able to reopen, and there has to be a recession coming. But most of our clients are in Canberra; they’re largely public servants and they all have secure jobs – most of them are OK and nothing much has changed.”

Over the last couple of months, Quilty has seen sentiment turn from a position of fear and uncertainty to many clients readying themselves to take advantage of the opportunities that may arise in the next six to 12 months.

“There was so much panic and fear at the beginning. We had a couple of clients pull out because of the uncertainty; we had one commercial SMSF client who pulled out, and then a few weeks later they decided they wanted to go ahead. By that stage, we couldn’t find a lender who wanted to proceed,” he says.

“We have other borrowers who are getting their finances ready because they think the market is going to crash, and they want to get ready to buy when it does.”

Meanwhile, down south – all the way across the Bass Straight, in Tasmania – the market is different again. Gloss Finance broker Narelle Kerstan, who won the Highly Commended, Broker of the Year award at the 2019 AMAs, says in Hobart her business has “slowed a little”, which she qualifies as going from working 60-plus hours a week down to around 40 hours a week.

“I’m usually frantic, and when COVID-19 first hit and everything died down a little, I thought, ‘Wow, this is an opportunity!’ I’m the typical mortgage broker that is too busy working in the business to work on the business, so I thought, this is an opportunity to get stuck into those things I’ve been putting off,” Kerstan says.

Craig Russell, Priority One Lending

Craig Russell, Priority One Lending

“While the cafes and shops are closed, our client base is not retail or cafe-based. It’s professional-based, so we’re busier than we’ve ever been” Craig Russell, Priority One Lending

“But it was probably only quiet for about two weeks. I’ve now started getting refinancing enquiries, and while activity has definitely slowed, I’ve still got more than enough work to keep me busy.”

Hardship loans and applications for deferrals have been few and far between, with just three clients approaching Kerstan for assistance in this area since the pandemic began.

“Two of them had it pretty much sorted, and I was happy to sit with them and discuss other ideas, but they’d already spoken to their banks direct. The other client sent me an email, and as they were still working and not in dire straits financially, I explained to them the potential ramifications of deferring their payments, and they were happy to continue as they were,” she explains.

“I found it really interesting that I’m reading all of this data, all of these stories saying that millions of loans have been frozen, but I’m not seeing any evidence of that in Hobart.”

Kerstan points to the lower average loan size of her clients as being a potential driver for this, with the average loan in her brokerage sitting at around the $340,000 mark.

“Perhaps because people can survive off one income more easily here, compared to bigger loans in Sydney and Melbourne?” she says.

“Or I wonder if perhaps the clients are just dealing with their lender direct, but my service model is quite personal, and I would think that because I base my service on being quite personal, they wouldn’t deal with it all on their own without reaching out. I’m not sure, but I’m just not getting the enquiries.”

In recent weeks, Kerstan has processed a number of loans for residential home purchases and blocks of land, but she admits that activity has fallen off by about two thirds.

True to her decision to work on the business rather than in it, she’s been using her time wisely to clean up her database and reach out personally to clients who may need some financial assistance in the weeks and months ahead.

“I’ve been in this industry nearly 15 years, so I have a reasonable database and trail book. I spent a weekend putting together an email, explaining what fixed rates were on offer and how I could potentially help people into a new, better product, and I got about 10–15 responses. It was definitely worth my weekend, spending that time on my database, as it well and truly paid off!” Kerstan says.

“I’m still getting a fair few brand-new clients, and every day my phone still rings. Anyone who has been in the industry for at least 10 years may not be stressing, as their trail book should be able to sustain them. It’s the newer brokers I worry about; it’s very hard to drum up any new business right now, so you really need to be able to work your database.”