New owner-occupier home values surged 4.9% in October – defying expectations of a slowdown fuelled by declining refinancing activity.

This, coupled with a 2.8% increase in owner-occupier commitment numbers, paints a picture of resilient demand despite a cooling refinancing market.

“The growth in number and value of new owner-occupier loan commitments ... has been relatively strong since February 2023,” said Mish Tan (pictured above left), ABS head of finance statistics.

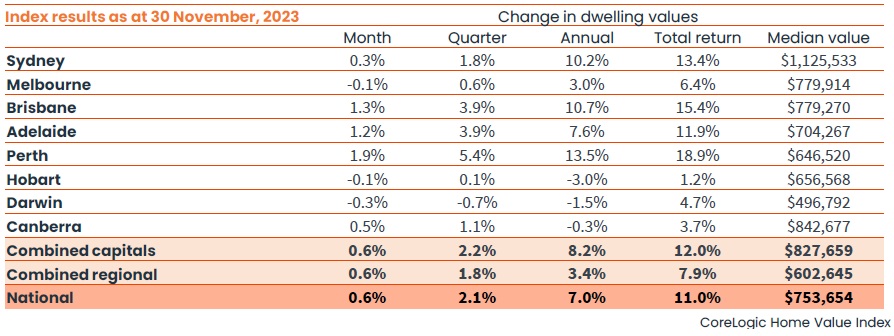

This aligned with CoreLogic's record high November Home Value Index (HVI) rise of 0.6%, marking a remarkable 8.3% V-shaped recovery from its January 2023 trough.

First home buyers are leading the charge, with the amount of loan commitments soaring 5.1% in October compared to the month before. They're also taking on bigger loans, with the average size now at $507,000.

This trend is mirrored across all owner-occupier loans, averaging a hefty $564,000 – up from $553,000 in September.

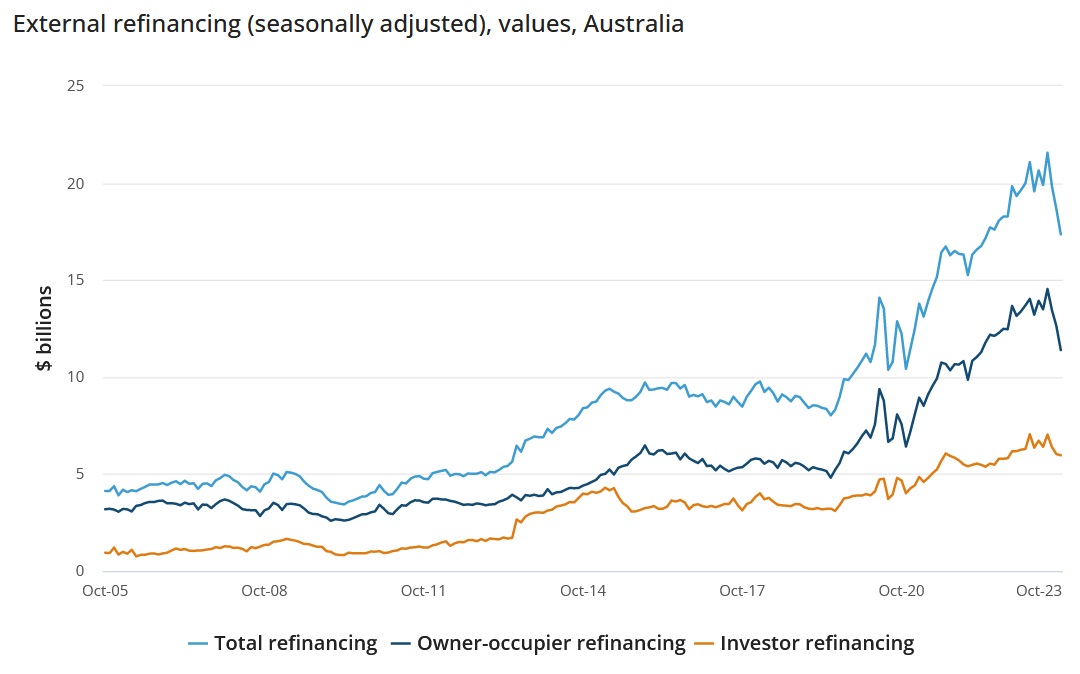

However, refinancing activity plummeted 12.4% to a mere $6 billion, suggesting many borrowers have either rolled off their low fixed rates already or the worst is yet to come.

This could spell trouble for the broader economy as refinancing activity is often a key driver of household spending.

The market's multi-speed nature is becoming increasingly evident.

While Perth sizzled with a 1.9% gain, the largest since March 2021, and Brisbane and Adelaide followed suit with 1.3% and 1.2% growth respectively, others faltered, according to Corelogic.

CoreLogic research director Tim Lawless (pictured above right) said these three cities continued to show “remarkably low levels” of advertised supply while purchasing activity was holding above average levels.

Melbourne, Hobart, and Darwin saw values dip, and Sydney’s once-robust growth slowed to a meagre 0.3% – its weakest since the rebound began.

Experts are cautiously optimistic. While headline trends have slowed, particularly in refinancing, Tan emphasised the "continued rise in pricing and demand for housing."

However, they warn of potential cooling in Sydney, which could follow Melbourne's lead.

This is especially the case after the Melbourne Cup Day rate rise that Lawless said had “clearly taken some of the heat out of the market.

“The more expensive end of the market tends to lead the cycles in these cities,” Lawless said.

“As borrowing capacity reduces, we may be seeing more demand deflected towards lower housing price points, with the broad middle of the market now recording the strongest rate of growth in Sydney and Melbourne.”

The gap between regional and capital city growth rates has converged, with both the combined capitals and combined regionals index recording a 0.6% rise in values in November. The convergence comes after regional markets have lagged their capital city counterparts through the recovery phase to-date.

“While housing values across both of these broad regions found a floor in January, the combined capitals index has since increased by more than double the combined regionals index, up 9.6% and 4.3% respectively to the end of November,” Lawless said.

Regional Australia’s housing values remain -1.8% below the historic high recorded in May 2022, with Regional Victoria (-6.7%) and Regional NSW (-5.5%) recording the largest shortfall from record levels.