PwC has advised its major clients that diversity legislation could be on the horizon in Australia. However, as women in the finance industry observe, ticking boxes is only half the story

In March, PwC Australia revealed it was advising high-level clients, including major banks and C-suite leadership teams, to prepare for the introduction of diversity legislation specifically focusing on gender balance in the workforce.

While the Workplace Gender Equality Agency (WGEA) collects data across six key areas from all non-public-sector employers with 100 or more employees, there are no mandatory reporting laws for gender pay gaps. However, PwC’s chief diversity and inclusion officer, Julie McKay, predicts that will change within three to five years.

Self-regulated diversity and inclusion policies exist across Australia’s largest banks. Westpac was the first to publicly commit to appointing women to 50% of its leadership roles and achieved its target in 2017, the same year it achieved its target of 40% of all the bank’s GM roles being held by females.

At Commonwealth Bank, new targets were set in 2015, following the fulfilment of previous targets set five years earlier. Currently, more than 50% of CBA’s graduate employees, 44% of all managers and higher, and 37% of all executive managers and above are women.

ANZ ensures a female candidate is interviewed for every role, and that all its interview panels contain at least one woman. Looking ahead, NAB has set itself a 2020 deadline to achieve its gender parity targets. Currently, 39% of the bank’s executive management roles are held by women; 39% of directors on group subsidiary boards are women; and 54% of its total workforce are female.

However, elsewhere things aren’t so positive.

Globally, it is calculated that the average income of women would increase 76% if gaps in participation and pay were closed. According to the UN, these disparities cost the global economy US$17trn annually – almost equal to the national debt of the US in 2014.

The bottom line is, when women work economies grow, and it isn’t just women – age, ability, background and race have all been explored in UN studies over recent years, unanimously concluding that a diverse workforce underpins a robust economy.

Social science aside, the business case is equally strong. A 2015 report by McKinsey & Company concluded that US firms in which women made up more than 22% of the executive team were 15–35% more likely to report greater financial returns.

Creating culture

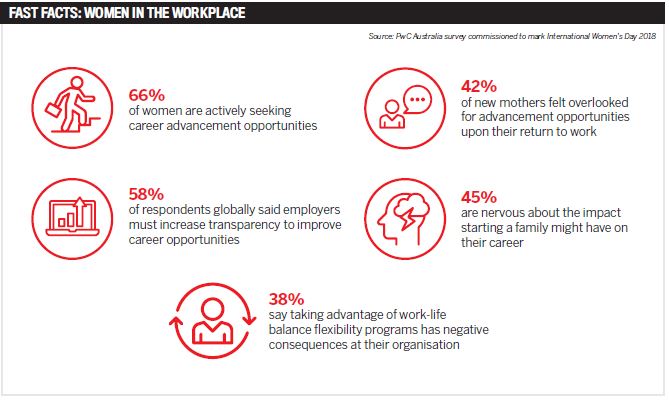

To mark International Women’s Day, PwC Global surveyed more than 3,600 professional women aged 28 to 40, including 247 Australian women at manager level or above. The results highlighted a need for trust and transparency, strategic support and advocacy, and support to achieve a work-life balance (see infographic).

PwC isn’t the only company crunching the numbers. Last year Astute Ability Finance Group principal Mhairi MacLeod commissioned her own survey on why workplace equality isn’t just about women. Questioning male and female respondents from the three “traditionally testosterone-dominated industries” of mortgage broking, professional sports and the motor trade, the survey confirmed that positive changes have been made but the work is far from over.

“I believe there is a need to create more positive information, messaging and communication about careers for women,” MacLeod says. “Then it’s crucial to ensure the right culture, policy and procedures are in place to promote this messaging.”

In creating that culture, men also have a significant role to play. Observing a shift in thinking among male colleagues and peers, MacLeod’s survey confirmed a greater respect for and acceptance of women in senior roles, and that, she says, has been a team effort.

“Men are deserving of credit here as they’ve played a huge role in mentoring, supporting and guiding women as they’ve found their way in these male-dominated industries,” she says.

Committed to change

There are pros and cons to legislating D&I, and the jury is still out on the effectiveness of imposed targets.

“I do not believe that gender diversity in finance could soon be regulated, and I am not an advocate for regulating an outcome. I would, however, be supportive of regulating a process,” says Siobhan Hayden, adviser and COO of HashChing.

“A great example is the Rooney Rule in American NFL, which is a policy that requires league teams to interview minority candidates for head coaching and senior football operation jobs. In the same vein, regulating that 50% of interviewee candidates are female would assist in driving better outcomes.”

In the first three years of the rule’s implementation, the percentage of African-American coaches in the league increased from 6% to 22%.

At the current rate of change, the World Economic Forum (WEF) estimates it will take 217 years to address the complexities of the global gender gap regarding pay and appointments. Despite this, there are some stand-out pockets of progress.

Australian finance is advancing ahead of the global rate of change, and that’s a testament to a strong national culture of inclusion and opportunity. Meanwhile, in Japan, which boasts a notoriously male-dominated business world, 60% of women leave work after having a child due to a cultural lack of work-life balance. WEF figures from 2017 rank the country 114th out of 140 global economies for gender equality.

MacLeod says, “For me it is critical that leaders are committed to, and involved in, the change. Businesses must also have programs in place that enable change. Some great examples of how this can be achieved are leadership development or mentoring and coaching programs that are designed specifically to support the necessary workplace shifts at the employee level."