By

Few people were expecting the Australian Bureau of Statistics’ most recent round of mortgage data to paint a rosy picture.

Indeed, the April 2020 Lending to Households and Business figures released by the ABS in mid-June revealed that the value of loans for housing fell by 5.0% in seasonally adjusted terms, with the decrease largely driven by a drop in owner-occupiers purchasing existing dwellings.

Adrian Kelly, president of the Real Estate Institute of Australia (REIA), says the figures represented the greatest decline the market has seen since the GFC.

“The value of new loan commitments for both owner-occupiers and investors displayed the largest fall in 12 months, and the purchase of existing dwellings experienced the largest fall in over a decade,” Kelly says.

“Not surprisingly, the ABS reports that lending institutions have indicated that COVID-19 impacts were evident through both reduced demand from borrowers and tighter lending criteria. What is more sobering is that the ABS says COVID-19 operational impacts experienced by some lending institutions resulted in a backlog of March housing loan applications being processed in April, which moderated the April fall in loan commitments.”

The number of owner-occupier first home buyer loan commitments fell by 3.8% in seasonally adjusted terms, but the proportion of first home buyers, as part of total owner-occupier housing finance commitments, was 36.7%, Kelly adds.

“Feedback from agents suggests that worse is yet to come on housing finance figures, as restrictions on movements throughout May and caution about the economy’s impact on activity in the housing market,” he says.

Economist Maree Kilroy from BIS Oxford Economics shares similar sentiments, after analysing the Lending Indicators data and finding that the monthly result was dragged down by “weaker demand for established dwelling loans (down 6%), as barriers to property transactions were imposed in response to the pandemic”.

Economist Maree Kilroy from BIS Oxford Economics shares similar sentiments, after analysing the Lending Indicators data and finding that the monthly result was dragged down by “weaker demand for established dwelling loans (down 6%), as barriers to property transactions were imposed in response to the pandemic”.

“Investor demand took another fall, down 4%. Similarly, first home buyers contracted by the same amount,” Kilroy says.

“The easing of restrictions on live auctions and open house inspections will see new housing loans gradually recover over the subsequent months” Maree Kilroy, economist, BIS Oxford Economics

These results are largely in line with what economists expected, Kilroy explains, with the month-on-month fall of 5% of total owner-occupier housing loans considered “relatively soft, all things considered”.

“Increased processing times meant that the April result included a backlog of loans from March, pre-pandemic,” she says.

“Following weak turnover with a modest lag, mortgage approvals are expected to contract further in May. The easing of restrictions on live auctions and open house inspections will see new housing loans gradually recover over the subsequent months. The recently announced HomeBuilder program will provide material support for new construction loans, but this will not be evident until the end of 2020.”

One group that hopes Kilroy is on the money with her prediction of a HomeBuilder-driven boost in activity is real estate agents, who are more than ready to see some activity return to the market.

National research by RateMyAgent has revealed that Australian sellers are increasingly unhappy with housing prices, with vendor price satisfaction decreasing by 5% in the first quarter of 2020.

Surveying more than 20,000 Australians, RateMyAgent’s newest Price Expectation Report (January–April 2020) asks successful vendors if the sale price they achieved was above, below or in line with their expectations.

The first quarter of 2020 showed a substantial increase in overall price satisfaction and a recovery trend, with net vendor happiness increasing 17%, from 25% in March 2019 to 42% in March 2020. However, as government-mandated regulations and physical distancing measures came into place in response to COVID-19, April vendor price satisfaction dipped nationally. Tasmania led the drop with a 16% decline in seller happiness, closely followed by Victoria and NSW.

“The Price Expectation Report shows us that the initial impact of COVID-19 on the market wasn’t as severe as expected, as the housing market has proven to remain resilient,” says Mark Armstrong, CEO of RateMyAgent.

“While we still need to analyse the long-term effect of the pandemic and keep a close eye on economic conditions, we are seeing the real estate industry begin to recover, particularly with the easing of restrictions and a slight drop in the national house price.”

In response to uncertainty, metro areas saw the largest drop in vendor happiness, with robust property markets in Melbourne and Sydney experiencing declines of 10–16% respectively. Meanwhile, regional areas in Victoria and Queensland saw a reduction in vendor happiness of between 4% and 1%.

Contrary to this, property markets in Queensland (4%), SA (1%) and WA (1%) initially saw a steady increase in price satisfaction in April. The remainder of Q2’s results will determine the full impact on the real estate market.

Contrary to this, property markets in Queensland (4%), SA (1%) and WA (1%) initially saw a steady increase in price satisfaction in April. The remainder of Q2’s results will determine the full impact on the real estate market.

“Not surprisingly, the ABS reports that lending institutions have indicated that COVID-19 impacts were evident through both reduced demand from borrowers and tighter lending criteria” Adrian Kelly, president, Real Estate Institute of Australia

“What’s great to witness is how high-performing agents have adapted and learnt new ways to remain ‘undisruptable’, while continuing to provide exceptional customer experiences in an ever-changing property market,” Armstrong says.

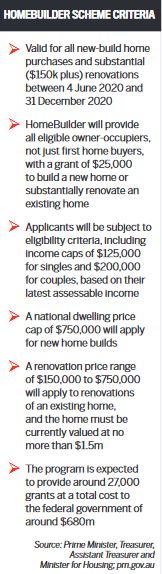

Looking ahead, will the newest stimulus package announced by the government, which will see grants of $25,000 awarded to homebuyers who build a new property or substantially renovate their existing home, have much impact on mortgage figures?

“While we still need to analyse the long-term effect of the pandemic and keep a close eye on economic conditions, we are seeing the real estate industry begin to recover” Mark Armstrong, CEO, RateMyAgent

“While we still need to analyse the long-term effect of the pandemic and keep a close eye on economic conditions, we are seeing the real estate industry begin to recover” Mark Armstrong, CEO, RateMyAgent

“In tandem with weak property turnover, we expect a further and larger decline in May of mortgage approvals given the lags involved,” Kilroy says.

“The HomeBuilder program favours the greenfield housing market over off-the-plan apartments, due to the short time frame for construction, as the intention is for construction to commence within three months of the contract date. Combined with existing grants, first home demand should respond solidly, especially in Western Australia.”

Eliza Owen, head of research Australia at CoreLogic, says the HomeBuilder scheme was announced in early June with the intention to boost activity in the construction sector, but the jury is still out as to whether it will have a substantial impact on the mortgage market.

“Dwelling construction is expected to see a lagged decline in activity off the back of COVID-19, as the recently recovering trend in dwelling approvals began to slip in April, led by a decline in unit approvals,” she says.

“However, the $25,000 incentive for building a new home, or renovating an established one, comes with a set of extensive eligibility criteria.”

Part of the eligibility criteria for renovations is that the property must be owner-occupied and not exceed more than $1.5m in value.

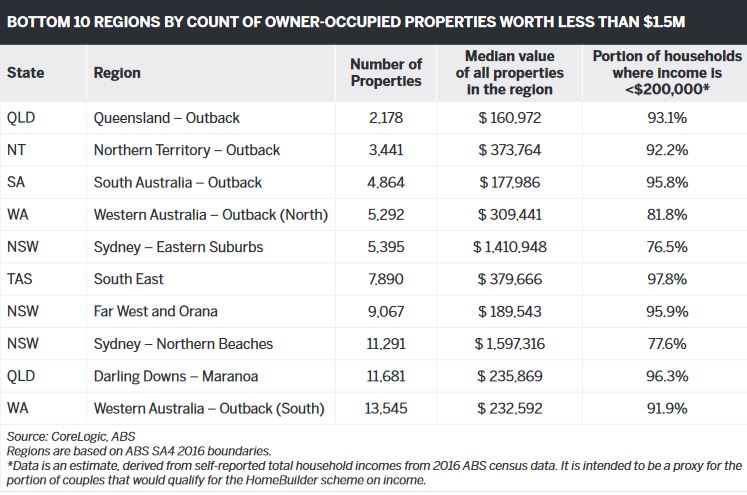

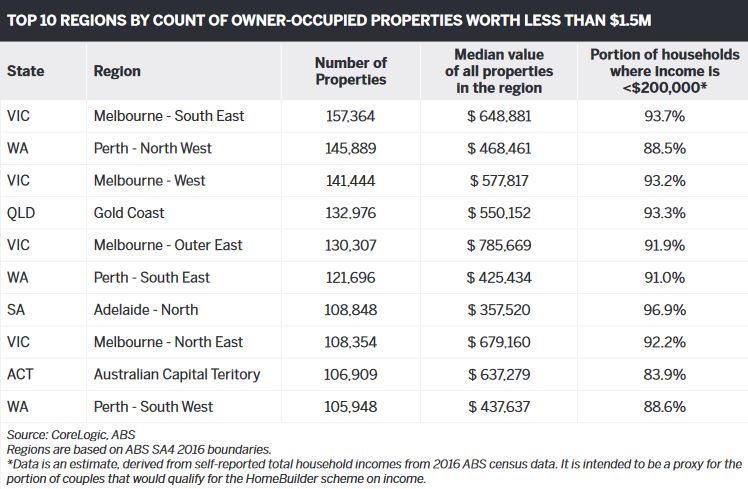

Using its extensive database, CoreLogic has put together a count of properties in the regions where the highest and lowest number of owner-occupied properties valued at under $1.5m are located (see boxouts). The count of properties includes those that it estimates are owner-occupied and have a high confidence valuation of less than $1.5m.

“Even where dwellings fall well below the $1.5m threshold for a renovation grant, many of these owner-occupiers will not take up the HomeBuilder incentive for renovations,” Owens says, warning that in areas where dwelling prices and incomes are relatively low, taking up the grant “may lead to owners overcapitalising on renovations, where they cannot recoup the cost of upgrades to the property”.

“CoreLogic estimates there are about 4.4 million owner-occupied properties across Australia with a high confidence valuation below $1.5m, but the federal government estimates the scheme may only support about 7,000 renovations,” Owens adds.

“While part of this is [due to] the income cap put on the scheme, it is also due to the high value of renovations that is set in the eligibility criteria.”