The Labor government has unveiled a major extension of its homeownership policy, pledging to allow all first-home buyers to purchase a property with just a 5% deposit—without needing to pay lenders’ mortgage insurance (LMI).

Unlike the previous version of the scheme, there will be no income caps or restrictions on the number of places available. The government will instead guarantee part of the home loan, helping buyers avoid costly LMI fees, which can often amount to tens of thousands of dollars.

Announced just weeks before the federal election, the expanded eligibility aims to help more Australians—especially younger voters—enter the housing market and forms a key pillar of Labor’s housing platform, Mortgage Choice reported.

Under the scheme, a Sydney buyer could purchase a $1 million home with a $50,000 deposit—significantly easing the financial barrier for many would-be homeowners.

“The median home now costs $820,000,” Labor said. “5% is $41,000. The last time that was enough for a 20% deposit was in 2002.”

The Housing Industry Association (HIA) welcomed the changes.

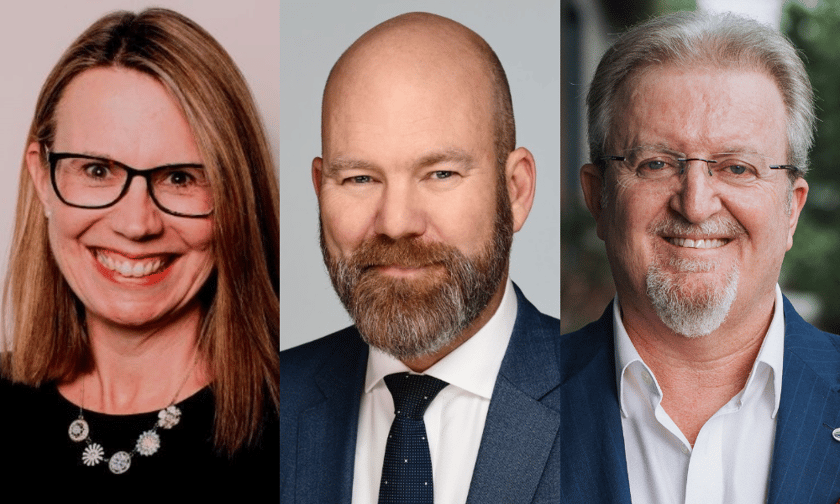

“The announcement to boost placements and recalibrating the median national purchase prices under the Home Guarantee Scheme will get more first-home buyers into a home sooner,” said Jocelyn Martin (pictured left), HIA’s managing director.

Martin added that LMI, which is traditionally required when a borrower has less than a 20% deposit, offers little value to buyers and primarily protects lenders.

“LMI doesn’t provide a benefit to first-home buyers, it is to protect banks,” she said. “There is an opportunity to lower the cost of borrowing for a first-home buyer without systemic risk to the financial system.”

However, not all industry voices are in favour.

The Insurance Council of Australia (ICA) voiced strong concerns, arguing the proposal could destabilise the private LMI market.

“By subsidising all first-home buyers, including those with a good income and savings in the bank, the purpose of the First Home Guarantee scheme is lost,” ICA CEO Andrew Hall (pictured centre) said.

ICA also cautioned that nationalising the LMI function could reduce competition and ultimately restrict access to finance for buyers not covered by the scheme.

“Effective nationalisation of the LMI market for first-home buyers as proposed will have the effect of reducing the pool of LMI customers so significantly that the market may become unviable,” ICA said.

The Finance Brokers Association of Australia also expressed caution.

Managing director Peter White (pictured right) acknowledged the benefits of the policy but highlighted possible roadblocks for lenders.

“While it is a positive move, there are complexities that may impact the ability of lenders to provide these loans to all applicants,” White said.

He noted that lenders must still uphold responsible lending standards and assess borrowers’ capacity to repay.

White also pointed out that limitations in securitisation—the process banks use to bundle and sell mortgages—could see lenders restrict how many low-deposit loans they offer under the scheme.

ICA concluded that Labor should narrow its focus to vulnerable groups such as single parents, frontline workers, and regional key workers—those who are most in need of housing assistance.

Without such targeting, critics argued, the scheme may dilute its original intent and disrupt the market’s balance, Mortgage Choice reported.