By

Despite a favourable interest rate environment and APRA’s removal of interest-only caps, arrears data highlights a new trend across Queensland and WA. Australian Broker examines the prospects for mortgage-stressed borrowers in the country’s most challenged markets

Tougher refinancing conditions, lower property values and slow wage growth have created the perfect storm for mortgage arrears in Australia. But, for a country that generally boasts a healthy and diversified economy, emerging trends don’t quite add up: full-doc and low-doc borrowers are experiencing more mortgage stress than those with non-conforming loans.

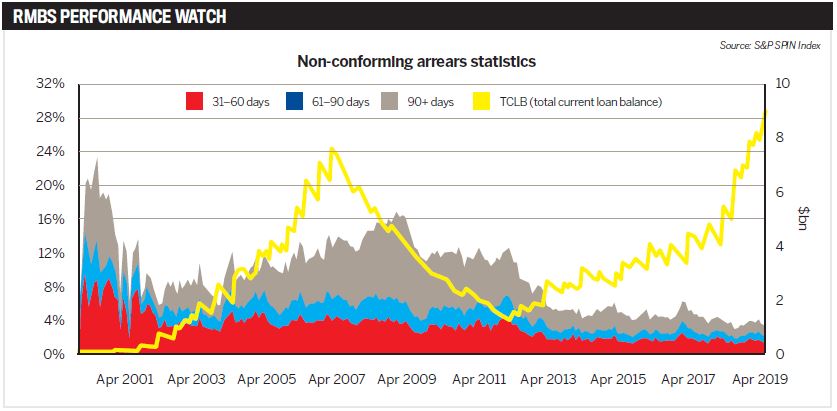

The latest statistics from S&P Global Ratings show that arrears of 90-plus days for full-doc prime loans increased from 0.7% in July 2018 to 0.8% in June 2019, while the same figure jumped from 3.1% to 3.7% for low-doc prime loans. On the contrary, arrears of 90-plus days for non-conforming loans improved over the year, albeit by an equally small margin, inching down from 1.57% in July 2018 to 1.52% in June 2019, while outstanding loan values for this sector of the market soared.

Bianca Patterson, director of Calculated Lending, attributes the trend to multiple historic factors; however, she also notes that Australia is currently facing its worst economic growth since the GFC, and that is clearly affecting those who, on paper at least, should be best placed to pay their mortgages.

“Borrowers are facing uncertain employment conditions and minimal salary increases while the cost of living continues to increase,” says Patterson. Backed by what the S&P report suggests, she says this income pressure leaves the “highly indebted household sector vulnerable to a sudden shift in economic conditions”.

The situation only seems to have worsened following APRA’s aggressive caps to limit interest-only lending, and Patterson points out that ripple effects are still being felt five years on – with property investors being hit the hardest – despite the caps now being lifted.

“Many borrowers are stuck in loans with higher interest rates or less attractive terms as a result of APRA’s intervention with the interest-only cap, the resulting capital holding requirements and high serviceability assessment rates,” she says.

“In some states there is the added issue of declining rents and property values. While renegotiating the terms of their loans could save them thousands and alleviate some of their financial stress, borrowers are trapped in old contracts due to overzealous lending terms.”

With economic performance muted, Patterson doesn’t expect to see a break on the horizon for these borrowers for “at least two or three years”. The current lower interest rate environment and reduction in assessment rates will ease the mortgage repayment stress for new customers, but the borrowers who are already in trouble require urgent help from their brokers.

The hardest hit

Of the top 20 areas with the highest arrears, 16 are in Queensland or WA, while the top six suburbs with the lowest arrears are in Sydney.

The S&P report suggests that “borrowers in areas with protracted property market declines have found it more difficult to ‘self-manage’ their way out”.

Tracy Kearey, managing director at Home Loan Connexion, believes that perhaps Australia has a two-speed economy, with the WA and Queensland markets still struggling post-mining boom. The decline in the required workforce in the last five years has drastically affected both states’ economies.

“Due to industries being affected in non-metropolitan areas, employment opportunities aren’t as easily available compared to major cities such as Sydney and Melbourne,” says Kearey.

“Lower employment naturally affects property prices following the rules of supply and demand, making it, as the report states, ‘more difficult to manage their way out of arrears’ by refinancing and selling.”

Patterson reiterates the challenges faced by the two states. The borrowers’ negative equity positions prevent them from selling, as there will be residual debt and no security for them to hold.

“Not being able to sell or convert their loans back to interest-only, or to lower rates, leaves some borrowers with no other option than to allow them to fall into arrears,” she says.

Early intervention

In the last 18 months, Patterson has been referred to more clients experiencing mortgage stress than at any other time in her eight-year career.

“Many are taking responsibility and genuinely trying to get ahead but are forced to face default interest rates, dishonour fees and unclear hardship processes as some of the roadblocks to getting on track again,” she says.

A lender’s hardship team will often be unwilling to speak to the broker, despite the latter being best placed to know the borrower’s financial situation.

“When I have been allowed to sit with a customer on a call to the lender’s hardship line, it’s easier to see how much work needs to be done to assist the client, what solutions are offered and how these conversations should be handled in general,” she says.

Patterson hopes the new Banking Code of Practice will assist lenders in addressing this issue in the near future. In the chapter ‘What to do when things go wrong’, it advises consumers to be “open and realistic” about their financial position, adding, “In turn, we will be compassionate in trying to understand your situation and when discussing any way we can help.”

Kearey believes it’s crucial for brokers to continue maintaining contact with their clients so that when the first loan repayment is missed brokers can quickly jump on the situation and speak to the hardship team to put a plan in place to get them into a better financial position.

“Now more than ever, brokers need to have systems in place to be regularly contacting the client at key events such as the anniversary or the fixed and interest-only expiry,” she says. “We have found that regular contact with the client gives them the opportunity and comfort to discuss any financial issues which could alleviate future arrears.”

However, a step back from the coalface confirms that bigger forces are at play in the lending environment. The total current loan balance among full- and low-doc prime loans has slipped from $122.6bn to $116bn in the year to date, reflecting muted economic conditions as well as the tighter lending and serviceability criteria around these loans.

The pendulum swing is an uptick in non-conforming loans, which posted a combined total current loan balance of $9bn this June, up from $4.6bn in July 2018, and their loan books continue to grow while their arrears, so far, remain low. How the trend will develop from here remains unclear, but what can be deduced from recent events is that, when it comes to serviceability, regulation does not always reflect reality.