By

Aaron Milburn, Pepper Money GM of mortgages and commercial lending, explains how the group is ideally positioned to help brokers thrive in the incoming era of heightened compliance

A mortgage broker’s knowledge and ability to source the right loans for their customers makes them an integral part of the lending landscape. The 60% of Australians who turn to a broker for help finding the right home loan can’t be wrong.

That said, 2020 looks to be a watershed year for the mortgage broking industry. A key recommendation from the royal commission was to implement a best interest duty for mortgage brokers, with a civil penalty provision. Commissioner Hayne wrote in his report that:

“… mortgage brokers should still be bound by the same duty due to the ‘advisory role’ they play, taking into account the borrower’s ‘objectives, financial situation and needs’.

“Borrowers look to mortgage brokers for advice about how to finance what is, for many borrowers, the most valuable asset they will buy in a single transaction. And brokers not only give advice about what they think is best for the borrower, they submit the loan application on the borrower’s behalf and, to the extent the terms are negotiable, negotiate the terms of the loan for the borrower”.

What is a best interests duty?

The government is working towards introducing a best interests duty for mortgage brokers when providing credit assistance – currently scheduled to come into effect on 1 July 2020.

Under the duty, brokers would be expected to understand and articulate their customers’ objectives, consider a range of lending solutions, and recommend the products that match the need.

It boils down to offering a loan that is not only affordable but meets the client’s specific needs, and ensuring it’s done in a compliant manner. It’s not always about the cheapest price; it’s about what will work best for the customer’s circumstances. Sometimes this may be as simple as a speedy turnaround time or size of the loan. If a conflict arises, the needs of the customer should always be prioritised over those of the broker. We know most brokers are already looking for the best solutions for their customers, which means the issue becomes recording and demonstrating that is the case.

The question we pose is: can technology play a key role in preparing your business to operate under a best interests duty regime?

Leading the race in 2020

Over the years, Pepper Money has encouraged brokers to ensure they have the appropriate systems and processes in place to better serve their customers and protect their businesses.

Moving forward, understanding what it means to act in the best interests of the consumer and demonstrating that you are doing so will become even more crucial.

For some brokers, this might mean adopting an entirely new end-to-end approach, spanning from training staff on the changes to adopting new tools and templates to improving record-keeping.

As far back as 2012, Pepper Money was giving away recording devices at industry events to help brokers protect their businesses with more accurate record-keeping. If a broker properly documents their customers’ circumstances, objectives, and reasons for the recommendations they are making, they should feel confident about the regulation changes.

However, introducing new technologies to assist in servicing customers can solve pain points beyond those related to compliance.

Pepper has consistently invested in technology to easily connect customers’ life situations to its loan solutions. Our technology focuses on delivering better service to both customers and brokers.

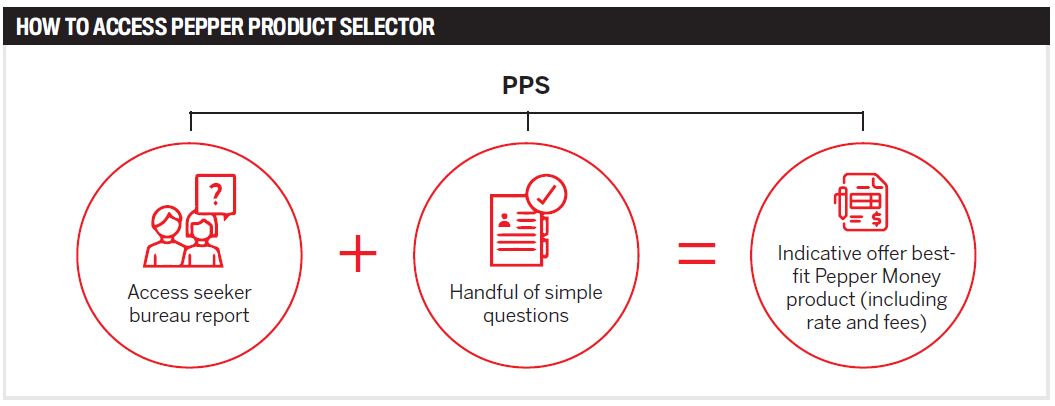

The Pepper Product Selector (PPS) tool is an example of this. It arms brokers with the insights and expertise to give their businesses a winning edge.

Pepper strives to remove friction from its processes with tools like PPS, helping brokers offer customers home loan solutions even when other lenders have said ‘no’.

When PPS was first introduced, it was designed to challenge the notion that non-conforming lending was ‘too hard’, when in fact the broker’s loan assessment remains the same. Brokers no longer need to consult a product guide or become an expert on Pepper’s cascading product model.

PPS identifies a specific home loan product, interest rate and fees, and provides an indicative offer (where applicable) for any client in less than two minutes – across Pepper’s prime, near prime or specialist product offerings.

The broker simply answers a limited set of questions about their customer. PPS runs a soft credit check (known as an ‘access seeker’) at no cost to the broker and matches the customer’s credit history with the information provided, to immediately return a Pepper loan solution, including an indicative interest rate and associated fees.

In a world in which a customer’s best interests come first, PPS will be an invaluable tool that will help make brokers more efficient and knowledgeable in sourcing best-fit solutions for their clients, the first time.

Often a customer working with a mortgage broker expects to obtain a loan at the low rate they’ve seen advertised, when in reality their circumstances or needs mean it isn’t available to them. That’s where Pepper’s 5 Step Process helps the broker successfully position an alternative home loan with a customer who may not have been expecting this type of solution.

Pepper Money has invested heavily in demystifying and simplifying alternative lending for brokers through a local BDM presence, a dedicated scenarios team, and a range of broker tools like PPS, which withallow brokers to manage their customers’ expectations.

Knowledge is power

Brokers who stay on top of the changes in the industry will surely benefit from making sure to adapt early. Those who ignore the debate may find themselves behind the eight ball once the incoming regulatory changes materialise in a way they weren’t expecting. The good news is there are steps that can be taken now to prepare for the future.

1. Educate yourself

We encourage brokers to stay abreast of the discussions across the industry to predetermine the direct effects of pending regulation on your specific businesses. If you’re concerned about the changes, reach out to your industry association.

2. Create relationships with the right mix of lenders

Best interests duty means you may have to be familiar with a broader mix of lenders who can assist your customers in getting the loan they needs. Broadening that group now will ensure you’re not caught unaware later.

3. Review your existing processes and make necessary changes

Will your current processes and systems allow you to accurately collect, prioritise and store a customer’s situation, needs and objectives? Do they allow you to effectively and efficiently match and communicate the recommended loan product? Considering how you will demonstrate compliance with future best interests requirements should start now.

At Pepper Money, we believe a good broker has nothing to fear from the implementation of a best interests duty, and a smart broker will already be aware of the role technology plays in ensuring customers’ needs are prioritised and delivered differently in the future.