As the RBA's latest rate hike takes effect and the construction industry spirals downward, one part of the home loan supply chain is booming: deposit bonds.

A deposit bond is a certificate from an insurance company that can be used instead of a cash deposit for home purchases.

Enquiries for this often-overlooked product segment has spiked by 300%, according to one of Australia’s oldest deposit bond providers, Deposit Power, with first homebuyers and families hoping to safeguard and grow their money.

As interest rates rise, deposit bonds become “more and more attractive”, according to Brent Davidson (pictured above left), general manager at Deposit Power – especially now that borrowers typically have a three-month lag before they feel the full impact of a rate rise.

“Back when interest rates were around 2% to 3% it was line ball if you were better off using your cash or a deposit bond,” Davidson said.

“Now interest rates are more like 6%, customer can save thousands when purchasing off the plan, use a deposit bond keep their cash working harder either in home loan offset or high interest earning savings.”

While the “bank of mum and dad” is there for some, finding the cash deposit can be tricky so deposit bonds are often becoming popular among first home buyers.

Deposit bonds work by replacing the 5% or 10% cash deposit when contracts are exchanged. This enables the buyer to pay the full purchase price at settlement instead of paying the upfront cash payment.

The buyer pays a one-off fee to issue the bond, on average around 1.3% of the deposit amount.

Davidson said Deposit Power typically saw two types of first home buyers – those who needed a short-term bond for a standard six-week settlement, and those who had a longer settlement period because they were buying off the plan.

“Those using short-term bonds tend to use them so they can move quickly and secure the property – they’re after speed and convenience,” Davidson said. “Those purchasing off the plan are the ones using deposit bonds to save money.”

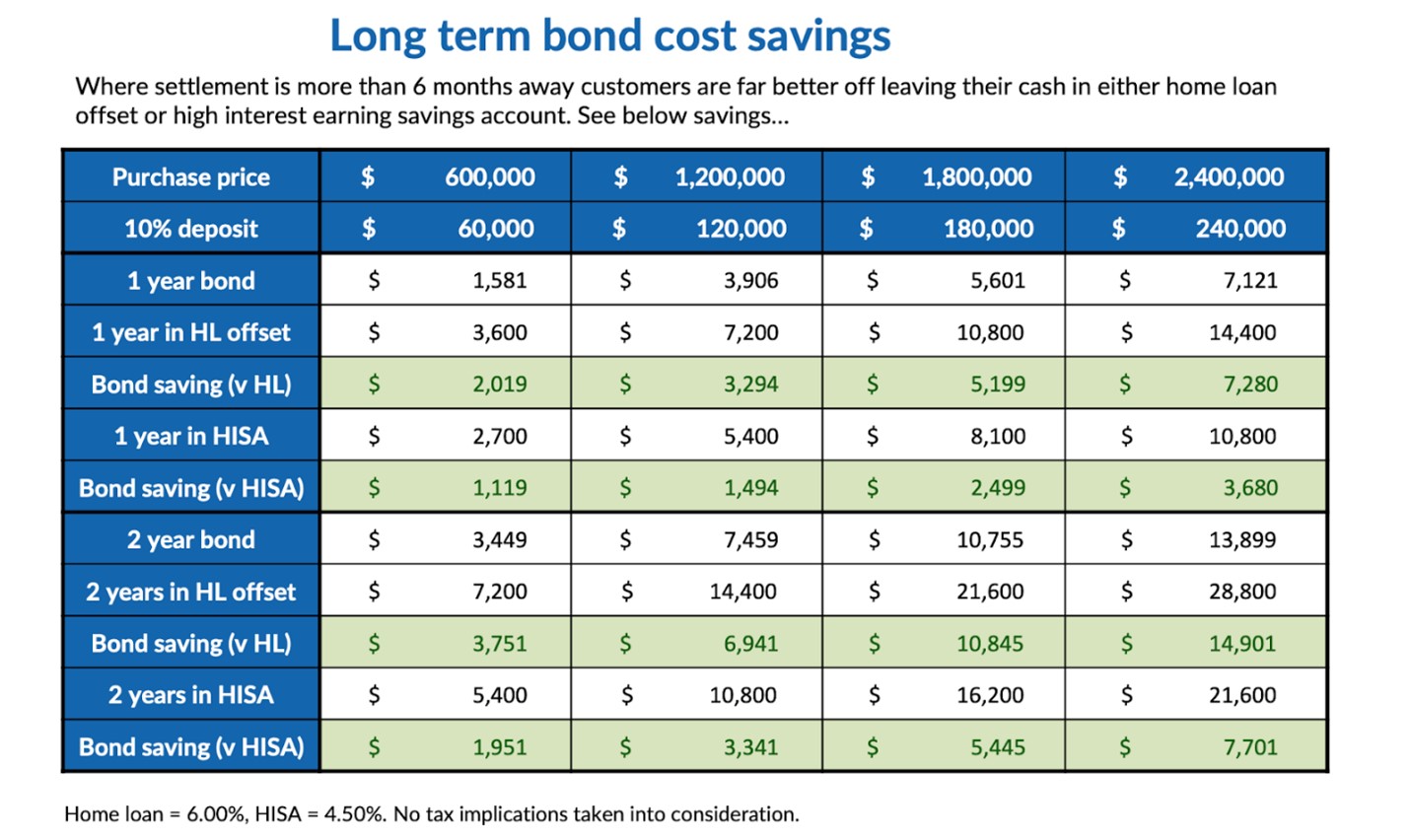

“Buyers with a settlement more than six months away will save by leaving their money in a high interest earning savings account and using a bond instead.”

For example, if a first home buyer bought a place off the plan for $1.8 million, requiring a 10% deposit ($180,000). However, the construction company goes under and there’s a two-year wait.

Without a deposit bond, they must use their cash for a deposit. With a deposit bond, they pay a one-off fee for the deposit bond certificate, in this case $10,865, and secure the title to the property.

From there, they could either put that cash towards an offset account or in a high-interest rate savings account for two years, potentially saving them $10,845 or $5,445 respectively.

“Financially it makes more sense to leave their cash in the bank while they wait for the property to be built,” said Davidson.

“People are saving thousands of dollars by using bonds rather than their own cash deposit for a property purchase, which for many can be difficult to get their hands quickly – either through lengthy loan approvals or having to break term deposits.”

Australia’s construction industry is reeling from tough conditions, with 2,023 companies going bust since mid-2021, according to ASIC data.

Many of these operations are not small either, with companies such as Clough Group, Probuild, Dyldam Developments, Snowden Developments, and ABG Group being among the larger companies to fold.

Porter Davis Homes Group – rated the 13th largest builder in Australia – alone put 1,700 projects in jeopardy across multiple states, according to UNSW.

While this is bad news in the midst of a housing supply crisis, it has increased demand for deposit bonds.

Deposit Power revealed internal data showing a 40% increase in retirees using their bonds to downsize and a 10% increase in people downsizing for lifestyle reasons including reducing their mortgage.

Davidson said in tough economic times, the company often experienced a surge in deposit bonds.

“We are seeing a repeat of what happened during the global financial crisis with younger people downsizing, often to a suburb a little further out, to reduce their mortgage,” said Davidson. “With the huge number of collapses in the construction industry, homebuyers are turning to deposit bonds for their new build.

Davidson said many saw the “no cash down solution” as the safer option because if the developer went under, they wouldn’t lose their deposit.

“It feels like Australia’s best kept secret. Lots of customers would benefit from using it, and if you are buying off the plan you would be crazy to use your cash.”

Amid the growth, Deposit Power has secured an agency agreement with HDI Global Specialty SE, an international insurer with an A+ credit rating.

“This rating underscores HDI’s exceptional financial strength and stability and gives assurance to our customers at Deposit Power that we’re in a strong position to meet our financial commitments,” said Davidson.

HDI is part of the Talanx Group, which has a premium income amounting to EU53.4bn ($88.6bn)

Davidson said the new rating would also help other businesses underwritten by Deposit Power such as Australian proptech platform Downsizer.com.

“We’re so excited about the rating upgrade with our partners Deposit Power,” said Mark MacDuffie (pictured above right), co-founder of Downsizer.com. “This will greatly increase the available stock for our qualified downsizer buyers whilst giving more security to our property developer clients.”

“Providing a cheaper alternative than bridging finance removes a significant barrier for downsizers who are often asset rich but cash poor. Older Australians can also be nervous about downsizing and the new A+ rating will help give them peace of mind when making the leap.”

While many brokers were well-versed in issuing deposit bonds for first home buyers and those buying off the plan, Davidson said he would “love to see” brokers use them for other scenarios.

“Education is a huge focus for us at the moment, helping brokers understand our top six scenarios or customer types we see. Most brokers only think of two or three,” Davidson said.

Other scenarios include buying vacant land, investing in commercial property, and buying with SMSFs.