Confidence is returning to the economy and with it the need for small businesses to access finance. NAB boasts one of the largest business bank networks and wants to help commercial brokers service the SME market.

NAB executive for commercial broker Chris Thomas is excited by what he’s seeing across Australia.

“The resilience of the Australian business community is remarkable,” he says. “Once again it’s risen to the challenge and found new ways of overcoming obstacles.”

Thomas says businesses are gaining pace with gusto in their recovery from COVID.

“We’re seeing good levels of growth in most industries. It’s wonderful to see. Many Australian businesses are now roaring back to life, and the level of business confidence is now above average at plus 15 based on our March NAB business survey. Business conditions also rose eight points to a record high of plus 25 index points in the March survey.”

Thomas says COVID-19 was an opportunity for Australia’s 2.1 million business owners to rethink their models, and many have adjusted.

Retailers switched to a digital and online sales model and performed better than if they had stuck to their previous modes of operation.

“You look at the agricultural sector, they’re going very well, with record crop yields, and there’s a bit of resurgence of the popularity of our provincial towns.”

Thomas says this is generating interest among people who want to relocate, which is having a knock-on effect of land sales, housing development and new retail businesses.

“You can start to see businesses actively employing more Australians – you’ve got the unemployment rate falling to 5.6% in March, and there’s confidence we can get to the other side of the pandemic in good shape.”

Thomas says with growth across most industries and “so many ideas floating in the heads of SME owners”, it is the right time for commercial brokers to turn their clients’ ideas into reality.

“We’re seeing significant demand for agri-equipment at our regional locations; the current instant asset write-off concessions in light of really strong profits coming from strong crop yields gives rise to buying new equipment and making those investment choices.”

In the cities, NAB is seeing significant demand from supply chain customers buying industrial land, new warehouses and warehouse equipment.

“It’s all coming back off the realisation that we can’t be purely reliant on global supply chains in light of the just-in-time concerns we’ve had with international supply,” says Thomas.

Australian manufacturing is also making a comeback, with demand for trade financing and equipment from Europe for food manufacturing.

Australian manufacturing is also making a comeback, with demand for trade financing and equipment from Europe for food manufacturing.

“There’s a shirt manufacturer that predominantly manufactures in Fiji, and they’ve just announced a line of shirts here in Australia – I don’t think we would have ever thought we would see that again.”

Thomas says the construction industry is extremely busy, with record levels of infrastructure projects and building of properties for new home buyers who are being supported by the government.

tThomas says the hallmark of NAB is its relationship-led approach to business banking.

“Relationships with our valued brokers are of paramount importance to us. It’s a great credit to our brokers that they’ve earnt the title of trusted adviser with their clients ... so we see the most powerful thing we can do as a business bank is to be the best partner for those brokers when it comes to forming the right solutions that meet their customers’ needs.

“We have to understand the broker, so we take a lot of time in really trying to get underneath what their business strategy is and what is important to them.”

The bank provides value through its BDMs, bankers and specialists who support brokers’ advice to their clients in what Thomas describes as a “powerful partnership”.

“We call it providing the ‘best of NAB’ to our brokers so they can feel comfortable that they’ve got a big business bank standing behind them.”

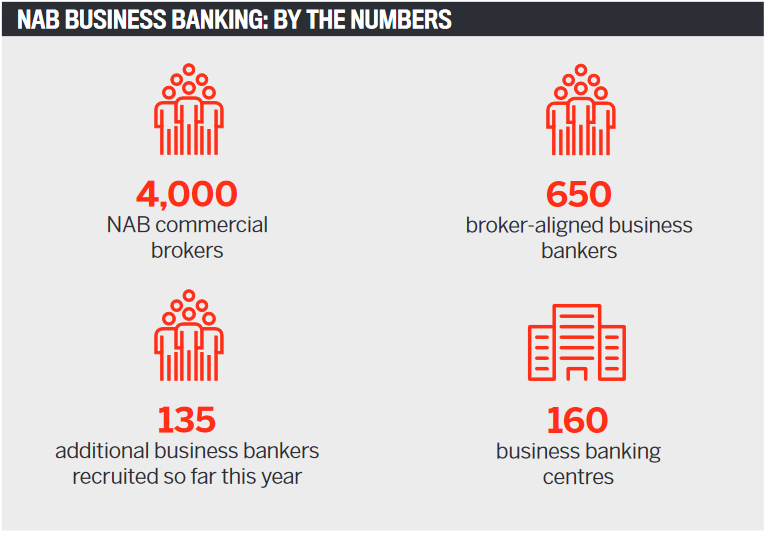

NAB has 4,000 accredited commercial brokers supported by 650 broker-aligned bankers.

“The strongest part of our value proposition remains that we have more bankers in more places across Australia,” says Thomas.

“The broking community is a national one, spread everywhere from regional locations into the capital cities. We have 160 business banking centres across the country.

“We like to believe that we can provide brokers with access to the whole of NAB better than any other lender in the market, and with that they’re tapping into that experience, that understanding of the local markets, and really working those partnerships to the maximum value.”

NAB commercial brokers are business owners themselves, and the bank is eager to help them grow their businesses.

Thomas says the partnership, when working well, serves both the broker and the bank by fostering mutual understanding of what all parties are trying to achieve.

The bank also supports brokers who are looking to diversify their businesses into commercial lending.“

Brokers that are curious about diversifying need to invest though. They need to invest in themselves and their businesses, either through upskilling or acquiring the talent that they need to run the commercial sides of the business.

“We recommend that they reach out to their aggregator and discuss the potential for NAB commercial accreditation.”

Thomas says that as the finance community strives towards a higher level of professionalism and education, he expects accreditation standards for commercial brokers to rise.

“We see the industry bodies, in particular CAFBA, playing a really big part in this evolution. The aggregators are playing a significant part as well.”

NAB works alongside aggregators with their PD programs but also conducts its own regular seminars at its business banking centres to “help brokers increase their understanding of complex fi nance solutions”.

Thomas says NAB’s lending proposition is one of the widest in the market.

“We have products to fund commercial property, agricultural producers, service-based and capital-intensive industries. We’ve taken a lot of pride in the fact that we can off er that wide-ranging level of lending solutions, enabling us to be innovative in the way we build our funding solutions.”

Employing bankers and credit managers with their own lending authority means that decisions can be made close to the transaction, avoiding extra layers of bureaucracy.

NAB can provide specialist advice to brokers and their clients, says Thomas. One example would be a business that wants to export goods and needs funds prior to shipping.

“We will bring in a trade specialist to support the business banker with the broker. Having that solution brought to the customer as a team approach is a real strength of what NAB can bring to our partnership with brokers.”

Turnaround times can be just as important in commercial finance as in residential, especially when businesses need quick funding for new contracts.

Turnaround times can be just as important in commercial finance as in residential, especially when businesses need quick funding for new contracts.

“Fortunately we have the muscle in our network – we’ve got over 650 broker-aligned bankers to support quick turnaround times, but we’re always striving to invest in ways to make our responses faster.”

NAB aspires to move customer documentation from paper to digital if legislative restrictions are removed in the future.

Digitising loan applications is also a goal, and the industry should move collectively towards that, says Thomas. Faster applications would allow brokers to spend more time with their clients than on paperwork.

“We have a QuickBiz product for funds up to $150,000 which can be applied for digitally, but anything beyond that it’s a more traditional way of applying for that finance.”

The bank has been part of the federal government’s loan schemes for SMEs since the beginning and has also signed up to the latest phase – the SME Recovery Loan Scheme.

This provides secured business loans of up to $5m or an unsecured business loan of up to $250,000 to those businesses that were receiving JobKeeper between 4 January and 28 March or were affected by the recent floods.

“NAB’s commitment to business customers extends 160 years, so we’ve been doing this a long time. We are there for the good times and the bad,” says Thomas.

He says NAB is proud and privileged to participate in the government support programs and provide the necessary support for businesses to recover. “We would encourage our brokers to make enquiries with us if they’ve got customers they feel qualify for that lending.

“We’re also seeing unprecedented demand for traditional lending, and that’s reflecting how quickly the economy is recovering, and that’s super exciting.”