More than half a million Australian mortgage holders have switched to interest-only payments to avoid delinquency, according to new research by Finder.

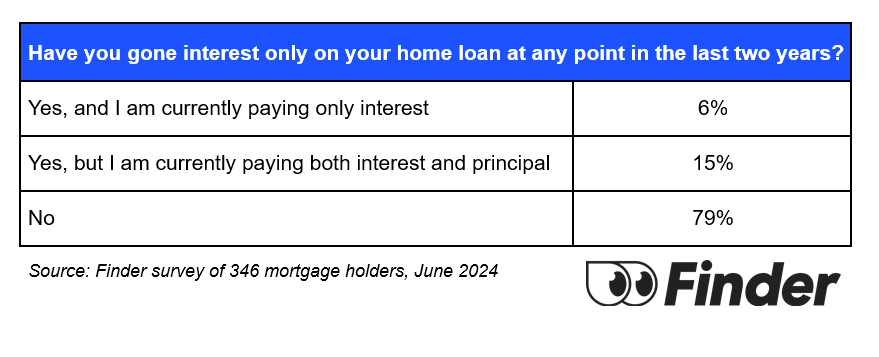

A survey of 1,062 respondents, including 346 mortgage holders, found that 21% have gone interest-only over the past two years. This change equates to 693,000 people paying the bare minimum on their loans.

The research indicated that 6% of borrowers, or 198,000 people, are currently on interest-only loans to avoid falling behind on repayments.

“Millions of Aussie households are in survival mode. Such a large portion of people’s earnings are allocated to their mortgage and spare cash has been extinguished,” said Richard Whitten (pictured above), Finder’s home loans expert.

Mortgage defaults have been increasing.

Finder’s analysis of APRA data showed $14.6 billion worth of home loans were 30-89 days past due in March, up 65% from $8.8bn in December 2022.

Overdue mortgages now account for 0.9% of all outstanding home loan debt, up from 0.62% in December 2022.

Whitten urged those struggling with mortgage payments to seek financial hardship assistance from their lenders.

“Banks have a responsibility to support customers experiencing financial stress, so put shame aside and speak up if you are in that position,” he said.

Whitten recommends borrowers ensure they have a competitive interest rate.

“You should be looking for an interest rate starting with a ‘5’ or a low ‘6’ – otherwise you’re paying too much,” he said.

Whitten also suggested conducting a mortgage audit at the start of the financial year to find better deals

To manage interest-only loans, Whitten advised:

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.