Nearly half (47%) of Australian mortgage holders have made changes to their home loan, including stopping their extra repayments, extending their loan term, or even selling their home, in order to deal with higher interest rates, new research from Canstar showed.

The Canstar survey of 699 respondents found that reducing their extra repayments was the top move made by 35% of mortgage holders, closely followed by stopping their extra repayments (29%), tapping into redraw or offset funds to help with repayments (26%), refinancing to a lower rate loan (22%), and extending their loan term (12%).

There were also mortgage holders who switched to interest-only repayments (10%) and even made drastic moves such as selling their home (7%) or investment property (4%).

“It's good to see that almost half of Aussie borrowers have planned for increased repayments by making changes to their loan,” said Steve Mickenbecker (pictured below), Canstar’s finance expert. “Many borrowers have used the low-interest era in recent years to prepare for higher rates by making extra repayments and now have money in their offset accounts or available for redraw.”

Mickenbecker said refinancing into a lower-rate loan has got to be the “least painful way” to cope with higher interest rates.

“Borrowers can potentially save around half of the repayment increases that have come through in the last 12 months, halving the degree of difficulty,” he said.

The finance expert said many of the borrowers who secured a loan prior to the Reserve Bank’s first cash rate hike in May last year “will already be in mortgage stress” and “may have to be tougher with themselves” to save or supplement their income in order to meet higher repayments.

“Lenders have hardship provisions for borrowers who have exhausted their own resources and may offer an extension to the loan term or to briefly switch the loan to interest only to provide lower repayments,” Mickenbecker said. “Borrowers have to act before the loan becomes too big a problem to bear and they are forced to sell.”

One in two borrowers (50%) said they are coping okay and 18% said they are thriving – and this may be because they acted fast on their finances. This could all change though once the full effect of the 11 cash rate hikes are felt by households and if RBA slugs borrowers with another rate increase.

If the cash rate is increased a further 0.25% in June and is passed on by lenders, this could add $84 to repayments for a $500,000 loan over 30 years. This, in turn, would see monthly repayments rise from $2,103 in April 2022 to $3,320 – that’s a total increase of $1,217 since the rate rise cycle began last year.

How different changes/strategies impact repayments

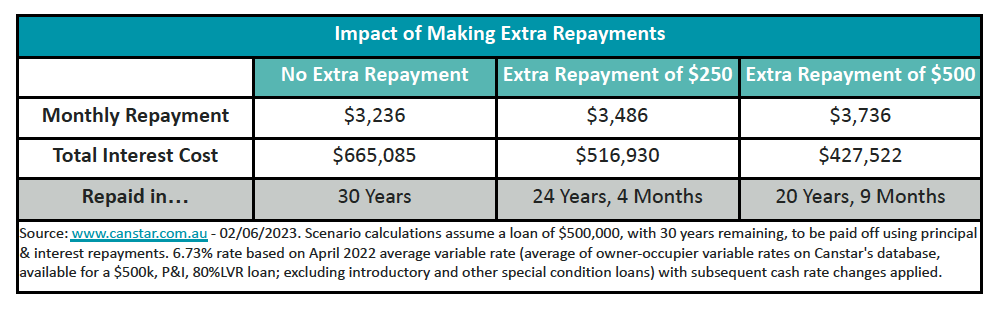

By culling extra repayments of $250 on a $500,000 loan over 30 years, borrowers can reduce monthly repayments to $3,236. Stopping or cutting extra repayments on top of the minimum requirement, however, wouldn’t enable borrowers to get ahead on their loan.

“With higher repayments now absorbing what were extra repayments, borrowers are no longer building their buffer for the future, but the present pain is being relieved,” Mickenbecker said. “However, borrowers who want to save on interest and pay off their loan months or even years earlier should look to top up their repayments again once they’re financially fit to do so.”

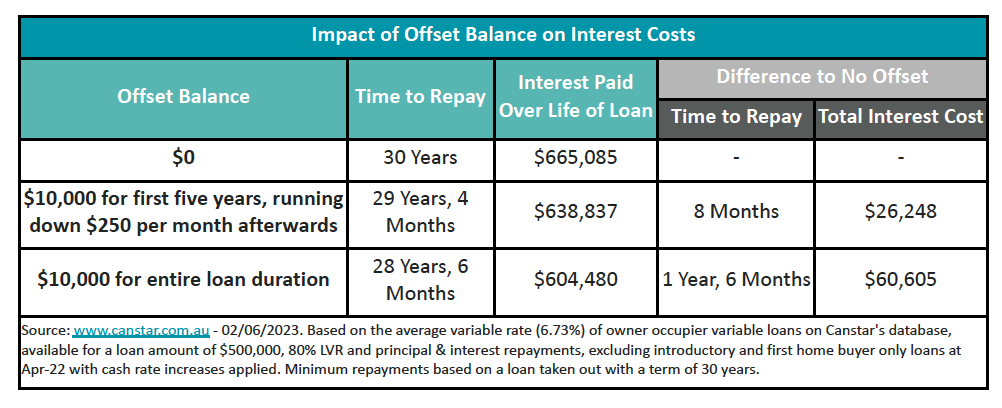

“Offset balances reduce the monthly interest being charged to the loan and shorten the life of the loan,” Mickenbecker said. “Progressively reducing the amount in offset will return the loan term closer to the original 30 years.”

In the case of a borrower with a $500,000 loan over 30 years with $10,000 in their offset account for the life of the loan, they would likely repay one year and six months earlier and pocket $60,605 in total interest when compared to those with no offset balance.

But, if five years into the loan, the borrower progressively dips into the $10,000 offset balance to meet rising repayments, their loan will be paid only eight months earlier and their savings would only amount to $26,248 in interest compared to if they didn’t have any money in their offset account during this time.

By refinancing from the average existing borrower variable rate of 6.73% to the lowest variable rate on Canstar’s database of 4.94%, borrowers can slash $570 off their monthly repayments on a $500,000 loan over 30 years.

“Switching from the average variable rate into one of the lowest rate loans available is the biggest saving borrowers can make,” Mickebecker said. “A low-rate loan can dramatically reduce the monthly repayment, helping mortgage holders to cope with rate increases without drastic changes to their lifestyle.”

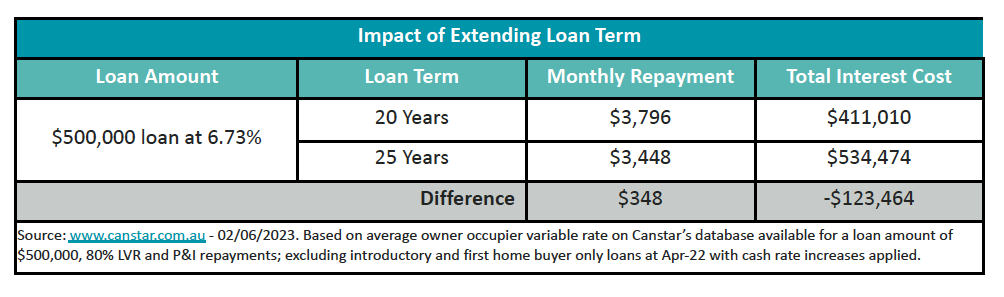

Extending the loan term by five years up to 25 years on a $500,000 loan could slash $348 off monthly repayments, but this will raise the interest paid at the end of the loan term by a whopping $123,464.

“Extending the term of the loan cuts the monthly repayment, but the trade-off is higher interest paid long-term and borrowers repaying loans later in life,” Mickenbecker said. “Critically, when people find affordability more under control, they should increase their payments to the loan to get back to the original trajectory.”

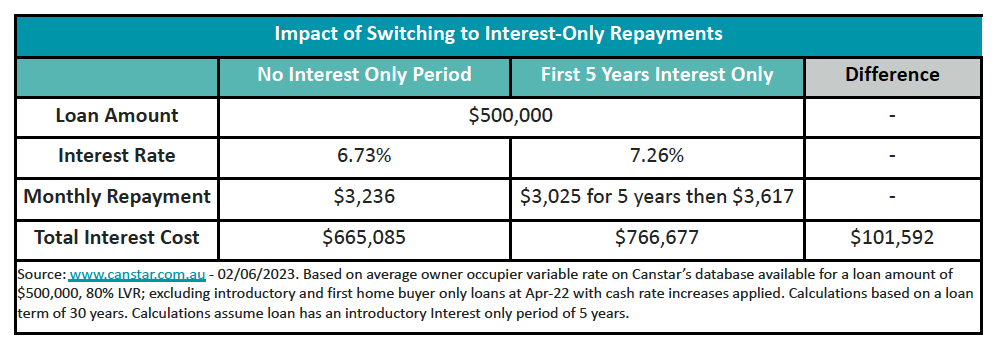

“Interest-only repayments reduce today’s burden but the risk is that the problem will be kicked down the road to the time when the interest only period ends and the repayment is not just restored to the former level but goes up to compensate for the period of no loan reduction,” Mickebecker said.

Borrowers switching to interest-only for a five-year period on a $500,000 loan over 30 years, can see their monthly repayments reduced by $211. However, the combination of a higher interest rate and making up principal loan repayments for the remaining 25 years will raise the total interest costs by more than $100,000.

Use the comment section below to tell us how you felt about this.