By

The scenario

A lot of our business comes via referral, and that was the case with this particular client. I met them through our network when an existing client personally referred him to me.

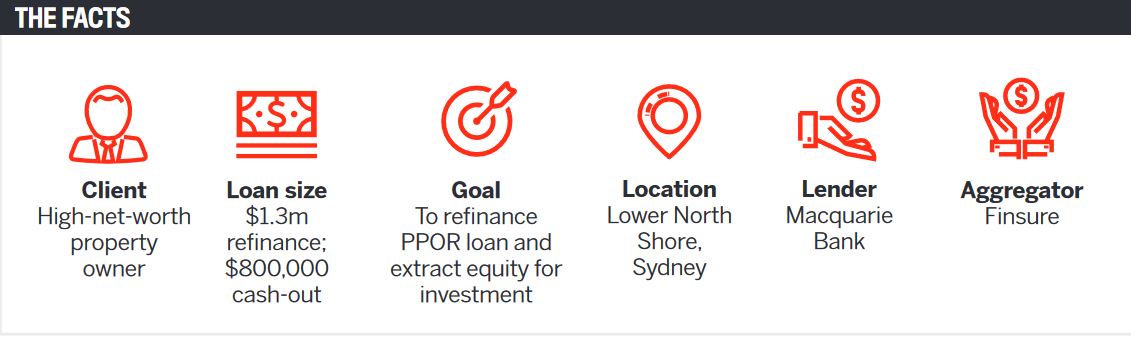

The client had substantial equity in his owner-occupied property – more than $1.5m. He was managing investments for an international fund and had a very strong profile and background; however, he was going through a job change. The client was weighing up whether to invest in shares or property, but his highest priority was flexibility so he could move fast and make swift decisions if required. He was running a share portfolio, which he wanted to retain, but he had noticed that the market had started to plateau, and he wanted quick access to funds to purchase land, a unit or shares.

He was trying to decide between property and shares for his next move, but he kept coming back to the fact that, if he decided to pursue a property investment, he wanted the flexibility and agility to be in a position to respond quickly and make a strong offer, once he found the property he wanted to purchase.

To facilitate this, the client required a large cash-out from his owner-occupier loan. We processed a refinance to extract equity from his PPOR loan to give him full flexibility in his use of the funds. He wanted access to $800,000 in total, which we arranged for him, and ultimately we went with Macquarie Bank for the finance.

The solution

The challenge with most lenders is that many of them create restrictions around the release of funds, as they prefer the bank to hold full control, and this can create potential delays. Finding a lender that understood our client’s position and requirements, and where we could demonstrate they could make the transaction as easy and seamless as possible, was essential to get the deal across the line.

Finding a lender that understood our client’s position and requirements, and where we could demonstrate they could make the transaction as easy and seamless as possible, was essential to get the deal across the line

The client was also worried that his recent job change could have the potential to impact the scenario. This is a common concern among borrowers, and it’s a valid one, as banks and lenders are looking for job security and continuity of employment when they assess a loan application.

I assured him that his recent job change wouldn’t impact his application, given it was a transfer within the same industry and his income level hadn’t changed. I also advised that the bank would consider all previous income being factored into the transaction.

The client requested the funds be flexible and ready to draw at request. Some banks apply covenants and require details of the investment, which can restrict the timing and potentially the opportunity. Given the range of events and the request from the client, many banks would not have been able to facilitate the transaction without having control over the funds or lending.

My understanding of all the banks’ policies helped overcome the client’s funding issue, as I was able to match him with a lender (Macquarie Bank) that recognised his position and understood the reasons why flexibility of the funds was required.

Also, the bank recognised that the client’s financial position was more than adequate, which meant it was comfortable about processing the transaction with a quick turnaround. Macquarie understood the industry and the client profile, which made this bank the ideal funding partner for the loan.

At the time, the interest rate the client was moving to under the refinance was also a significant decrease from what he was paying previously, so the deal put him in a better financial position overall.

The takeaways

Assessing the client’s individual needs is the first step of the process, but matching them to a lender that will work with them and help them reach their outcome is key.

Most banks have policy niches and professional niches. It’s always important to educate the client on each bank’s strengths and weaknesses when it comes to policy and professional specialists.

It’s about understanding each bank’s strengths and weaknesses, as this enabled me to facilitate a seamless transaction and provide my high-net-worth client with a great outcome.

Luke Heavey

Luke Heavey

Senior finance consultant,

Orium Finance