By

Jenel McClelland, senior mortgage broker and founder of Green Apples Finance Australia, explains how working with her client to understand the worth of a deal was key to getting it over the line with the lender

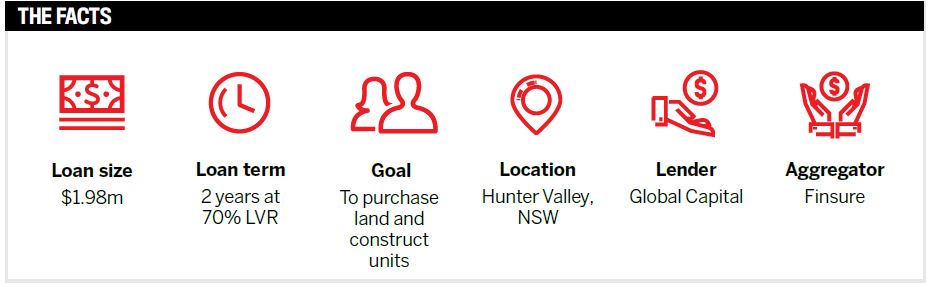

My client approached me to finance an investment development build of eight units, specifically tailored to the disabled community.

The client was purchasing the land and had a builder’s contract in place to construct specialty housing.

They were then approached by Compassion Australia to purchase these units after the building was completed, under a NSW Government housing scheme initiative put in place to build 300 specialty houses in the area in the next 12 months.

The problem was that the on-sale of the properties was to be exchanged with a $1 deposit only, as is common practice for government organisations.

I approached several lenders, but they said they couldn’t help fund the deal with a $1 exchange and needed the normal 10% deposit exchange; most even said they had not seen this before.

So I asked the lenders what they needed in order to accept the $1 exchange – what did they need to see?

This is where it became quite interesting: some lenders said it was not a deal they would be able to look at, while others had no idea what they needed and had to check with their head of credit and get back to me.

Many calls were made that week, between me and a lot of credit officers with the various lenders, and some even said the contract seemed “dodgy”.

However, upon investigating further, I realised that it was, in fact, an acceptable form of exchange, particularly when it came to non-profit organisations working with the government, as it protects the purchaser, particularly when construction is involved. This is because they can outlay very little cash, and if the process is not followed carefully – as disabled housing is very specific with respect to their needs and rules for housing – they have very little risk.

As the lender would have been relying heavily on the ongoing sale, I understood their hesitation over this deal. Therefore my clients and I had to work together to gather more information, because asking the local government for a letter explaining the incentive for this form of housing was never going to work; they would have needed to go through at least eight departments and then have the letter vetted by the prime minister himself.

So we had to prove the government incentive by researching announcements and government policies, then confirm that Compassion Australia was qualified under this incentive.

We also had to prove that the Hunter Valley region qualified for this incentive, as the government wanted to establish 300 homes in the overall area, so it even came down to postcode acceptance.

Additionally, we had to explain every detail of the conditions of the contract of sale, page by page, at each stage of the build, and how it would be monitored and passed by all parties, not just my clients.

We had to guarantee that the contract was watertight and that these conditions were acceptable to the lender and the time frames were realistic, as everything had to happen in sequence.

My client had previously built other small projects for Compassion Australia and had to obtain letters confirming the organisation had dealt with my client in the past and so were basing their guarantee to purchase on the quality of work previously completed.

We also had to confirm that this project would be using the same builder as before and obtain guarantees in writing that work would be carried out to the same standards.

After several days of explaining Compassion Australia’s commitment under the contract, with many calls and emails between all parties, I was able to fund the deal at the eleventh hour.

It just shows that knowing your client and understanding the worth of a deal is very important to your communications with potential lenders. It’s great when you have the same enthusiasm as your client to make it work.

I think my days of working with the Spastic Centre of NSW when I was an entrant in the Miss Australia Quest many, many years ago made me even more determined with this client. These people are screaming out for housing, the incentive is there, so why not help them?

Lenders should step up and look at how they can help get such initiatives across the line and not shy away from them because “it’s not the traditional way”.

My client was very happy and appreciative. I explained that we were a good team, “working together and not giving up”.

Every deal is ‘a big deal’ to me, and I hate not being able to help. We at Green Apples Finance Australia have become known as the ‘bulldogs’ because we get our teeth into the deal and won’t let go until we have exhausted everything.

Mind you, we celebrate our wins too… sometimes too much!

Jenel McClelland

Jenel McClelland

Mortgage broker and founder

Green Apples Finance Australia