By

Emmanuel Marios is the director of Hobart-based mortgage brokerage Derwent Finance, which serves clients across Tasmania and Melbourne. He assisted a borrower who wanted to purchase his first investment property through his SMSF but was unhappy with his lender.

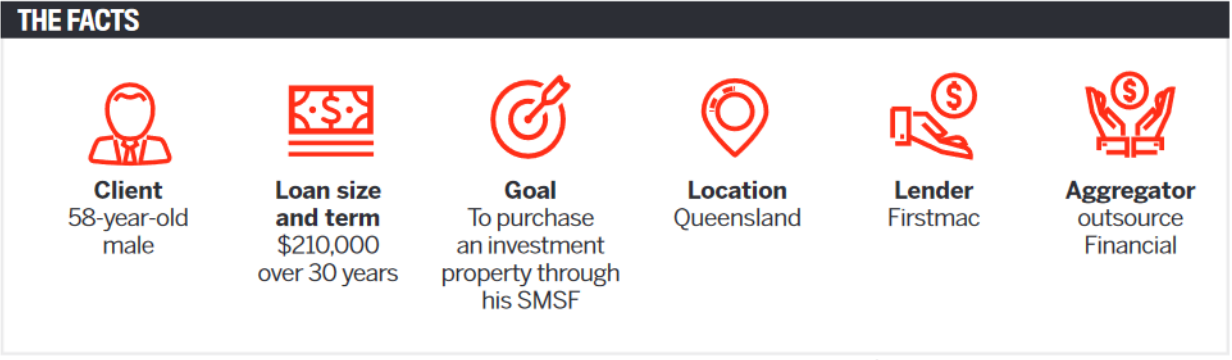

This client, who was referred to us by a referring partner, was looking to finance the purchase of his first investment property through his self-managed super fund. The client already had a contract of sale in place and had made contact with another lender; however, he was unhappy with their reliability and therefore lost trust in the lender and wanted to find another professional to handle the transaction.

At the beginning of the application it was very simple: a low purchase price on the contract of sale and high serviceability on the client’s end. Although it was an SMSF purchase, we had many lenders on our panel for the client to choose from.

The deal was submitted, and everything was moving along smoothly until the client’s original lender came back to him with a better offer. The client then asked us to withdraw the application we had submitted on his behalf. To be fair, the off er was indeed a fantastic offer, and one that would have been hard to say no to. However, this was a time-sensitive matter with a contract of sale in place.

Two weeks later and with five days until the finance clause was due, the client came back to us, stating that the original lender was too unreliable and slow, and asked us to resubmit his application to Firstmac. As we all know, with lenders’ current service level agreements, unconditional approval within five business days is often unheard of, especially with a more complex deal like an SMSF purchase. Personally, I really didn’t know if it was possible, but I took the risk.

I know that unfortunately this isn’t the case with all applications, and I have had my fair share of finance clauses not being met; however, I believe fantastic communication is the key to moving forward, and quickly.

This wasn’t a deal that needed solution-based thinking or conflict resolution; it was an application that was time-sensitive and needed approval within a very short period of time.

Having a clean application from the very start, taking the time to write detailed broker notes, and providing as many of the required documents as possible on submission minimises the back and forth between the lender, broker and client, which can take up a lot of time.

Although the goal is quite often to submit an application as quickly as possible, you also need to take it one step at a time and ensure everything is spot on before submitting.

It’s then important to maintain good communication with the lender, explaining the scenario to them and highlighting the due date; constantly contacting them for updates on how the fi le is travelling, and to find out if there is anything you can do at your end to get things moving, and so on. This good communication also applies to the client, so they need to be advised to be on the ball and proactive in responding to all requests that come to them, in order to avoid any delays.

By doing all the above, fortunately we received an approval letter from the lender and met the finance clause due date on the contract of sale. This was hugely to do with each party communicating and being active regarding the application – from the client to myself and my team and the lending support. Our BDM was passionate and on our side in his efforts to get the loan approved, which was fantastic and resulted in a successful transaction. This was a huge relief for all parties involved.

Additionally, we received the approved loan documents for the client the day following the approval (that day was a public holiday as well, so the lender’s team was thin on the ground), so there was no further delay in the next step of the transaction.

This outcome would not have been possible if it wasn’t for the team involved in this application.

The takeaways from this deal are primarily to keep your relationships strong with everyone involved in the application process, from the client right through to the BDM and lending support, and to keep everyone motivated and passionate about getting the deal done. At the end of the day, you need to be on the lender’s side and to maintain a good relationship with them, because they are the ones controlling when the application is picked up and approving the loan.