By

A number of factors combine to determine a property’s true value. Location, aspect, quality of finishes, number of bedrooms: these are some of the more tangible aspects of real estate that influence a particular dwelling’s value.

Next, you start to factor in proximity to local amenities such as public transport, cafes, schools, local parks and beaches.

Lastly, there are the ‘external’ influences, which have nothing to do with the property whatsoever, yet everything to do with its potential value.

This is the category that the coronavirus pandemic falls squarely into. A health crisis that birthed an economic catastrophe, the pandemic has robbed Australia’s real estate market of demand and well and truly taken the wind out of its sails in terms of property price growth.

Now, as the country edges back towards the ‘new normal’ with a state-by-state easing of restrictions, how will the property market be impacted?

“Generally, the outlook for inner urban established housing values is to remain reasonably stable. Predicted value falls relate to lower-value, urban fringe established housing” Scott Keck, chairman, Charter Keck Cramer

If we take the banks’ word for it, then the immediate outlook for property owners is grim. In the middle of April, for instance, Commonwealth Bank – which holds the largest slice of the Australian mortgage pie, at a value of approximately $446bn – predicted that property prices would plunge 10% within six months as a result of COVID-19’s impact on the economy.

“Australian capital city dwelling prices, led by Sydney and Melbourne, have risen strongly over the past nine months, but we expect that stellar run to end abruptly,” Gareth Aird, CBA’s head of Australian economics, told the media at the time.

“The policy response to limit the spread of COVID-19 has created a plunge in economic activity, and unemployment will spike. This will have profound short-term consequences for the housing market.”

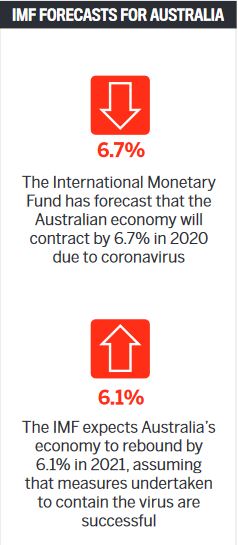

By mid-May, CBA had revised these figures quite dramatically. The bank flagged a number of scenarios, including a “prolonged downturn” forecast, which saw GDP growth fall by 7.1% this year and a further 0.8% in 2021.

In this scenario, unemployment would average 9% this year and 8.5% next year, before easing back to 6.5% by 2022. In this worst-case situation, the bank’s economists forecast that house prices would fall by around 32% over the next three years from their March 2020 peak.

Nicola Powell, senior research analyst, Domain

Nicola Powell, senior research analyst, Domain

“Homeowners are not being forced to sell, despite the economic turmoil and rising unemployment created by the current health crisis” Nicola Powell, senior research analyst, Domain

NAB group chief economist Alan Oster pointed to an outlook for the economy that “more broadly is unsurprisingly significantly weaker than three months ago”.

“We expect dwelling prices to fall by around 10% this year and decline further in the first half of 2021 before levelling off. The declines will be led by Sydney and Melbourne, but the other cities will not be immune to rising unemployment and slower wage growth,” he said.

“Alongside the decline in house prices, we expect dwelling construction to continue to fall. The pipeline of work yet to be done remains relatively elevated in NSW and Victoria, but this will be rapidly eroded with high rates of work done.”

“Alongside the decline in house prices, we expect dwelling construction to continue to fall. The pipeline of work yet to be done remains relatively elevated in NSW and Victoria, but this will be rapidly eroded with high rates of work done.”

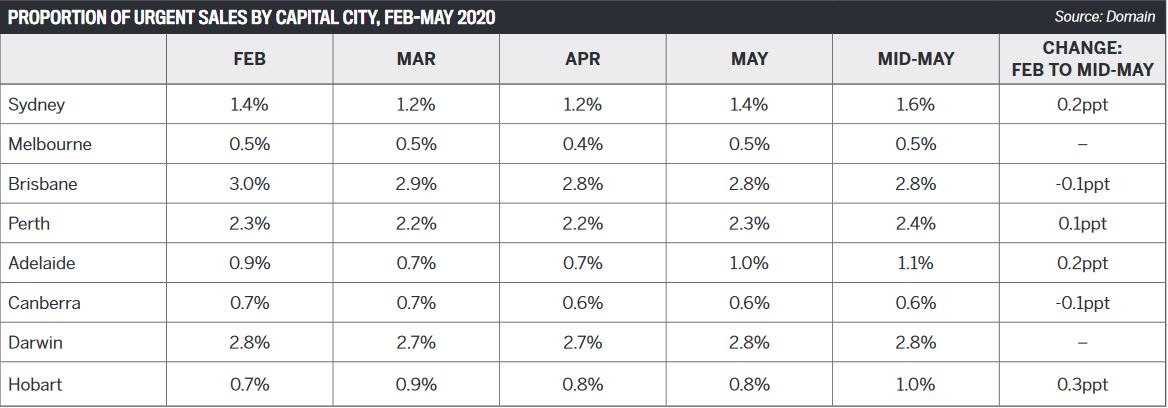

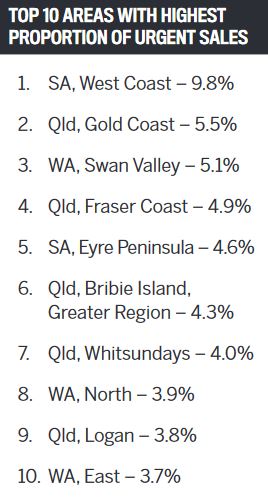

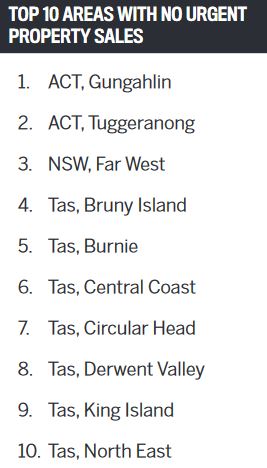

However, despite all of these predictions that property prices will tumble due to distressed sales, recent data from Domain reveals that most capital cities around the country have actually fared well so far.

Domain senior research analyst Nicola Powell said there was “little evidence to suggest an increase in urgent or distressed selling across Australia’s capital cities”.

In fact, our major capitals have seen only very marginal increases in distressed listings, with Canberra and Brisbane experiencing a decrease in the number of such listings.

“Sydney, Perth, Adelaide and Hobart had a marginal increase in the proportion of urgent sale listings from February to mid-May when the full economic shutdown and social distancing restrictions would have been felt,” she said.

Source: Domain

Source: Domain

“Melbourne and Darwin had no change, while Brisbane and Canberra saw a marginal decline in the portion of urgent listings. This suggests homeowners are not being forced to sell, despite the economic turmoil and rising unemployment created by the current health crisis.

”While the aftermath of the economic disruption caused by the coronavirus crisis could result in rising distressed sales, Powell suggests the action taken by banks and the government may serve to largely stave off any serious declines.

“Homeowners have been provided with a lifeline during this economically challenging time through the intervention of the banks and government: the JobKeeper subsidy and the ability to pause mortgages, as well as a more generous JobSeeker payment. These will minimise the number of urgent or distressed sales, which will in turn support prices. If the policies were not in place, the immediate risk to prices would be far greater,” she said.“

The longer-term impact could be different, and an uptick in distressed selling is possible once the policies cease. If the JobKeeper subsidy performs as intended and retains jobs, together with economic activity bouncing back, any dramatic increase in distressed selling is unlikely.”

This may put a floor under actual property values in real terms, but confidence in the property market – as well as the perception of it by key stakeholders – could cause some negative price movement.

Income2Wealth CEO Paul Wilson, a property investing expert with more than 20 years of industry experience, says that despite facts and figures showing a robust real estate market, the issue of falling house prices could become “a self-fulfilling prophecy”.

“The problem we have is that when banks and lenders start forecasting a 10% drop in property values, they then start factoring this into their property valuations. The data and activity in the market may not support a 10% drop, but they are being conservative and buffering that into their valuations, when in reality there is no evidence to support that yet,” he said.

“Another part of the problem is that we’re dealing with so many lagging indicators when it comes to data. We’re seeing the numbers coming out of CoreLogic and the ABS, and they’re two or three months old, so it’s hard to get a gauge on what is actually happening in the market.”

With a lack of evidence to support a sustained drop in property values, why are valuers being so conservative?

Those in the industry are wondering whether it’s a byproduct of the GFC, when many valuers were hauled over the coals for not being conservative enough when it came to property valuations. So they’re factoring in a drop in values in advance, despite the fact that the market hasn’t yet experienced a significant increase in distressed sales.

Paul Wilson, CEO, Income2Wealth

Paul Wilson, CEO, Income2Wealth

“When you can ride out the peaks and troughs [you’ll] experience a more profitable return on investment in the long term” Paul Wilson, CEO, Income2Wealth

Scott Keck, chairman of strategic property consulting firm Charter Keck Cramer, has almost five decades of property valuation experience in the Melbourne market. Keck said that although the impact of COVID-19 had been dramatic, it has “not yet manifested in indisputable evidence so far as the property market and values are concerned”.

“The simultaneous end of JobKeeper, JobSeeker and mortgage or lease deferments in September will represent a real challenge if the economy hasn’t revived sufficiently to give people the financial ability to resume their commitments. Quite significant structural changes will be occurring in the economy, which are yet to be reflected,” he explained.

A downturn in population growth as a consequence of reduced immigration through to mid-2022 is also expected to have an impact. While this may result in a short-term softening for houses and apartments, especially in Sydney and Melbourne, Keck is confident that a more likely outcome is a return to a balance between supply and demand by 2023.

A downturn in population growth as a consequence of reduced immigration through to mid-2022 is also expected to have an impact. While this may result in a short-term softening for houses and apartments, especially in Sydney and Melbourne, Keck is confident that a more likely outcome is a return to a balance between supply and demand by 2023.

“Generally, the outlook for inner-urban established housing values is to remain reasonably stable. Predicted value falls relate to lower-value, urban fringe established housing,” he said.

Banks, as Wilson suggested, are being much more conservative in their estimates.

ANZ has forecast weaker household income, sharply rising uncertainty for households, reduced population growth and a weaker investor sector as some of the factors that will depress Australia’s housing markets over the next 12 months. As a result, the major bank forecasts that the decline in demand will push prices down by around 10% on average across all capital cities.

The flip side to that coin is that ANZ expects prices will bottom out in mid-2021.

“I always advise property investors to view real estate assets as being a long-term play of at least 10 to 15 years,” Wilson says. “When you can ride out the peaks and troughs of the market along the way, you’ll be in a much better position to experience a more profitable return on investment in the long term.”