Eliza Owen (pictured above), head of residential research Australia at CoreLogic, analysing ABS housing finance data, underscored the escalating challenge faced by first-home buyers in Australia’s soaring real estate market.

Despite a significant increase in the CoreLogic Home Value Index by approximately 150% over the past two decades, wages have not kept pace, rising only 82% according to the ABS Wage Price Index.

The disparity has widened the gap in property affordability for first-time buyers, reflected by “a deterioration in affordability metrics and an increase in the average age of first home buyers over time.”

See LinkedIn post here.

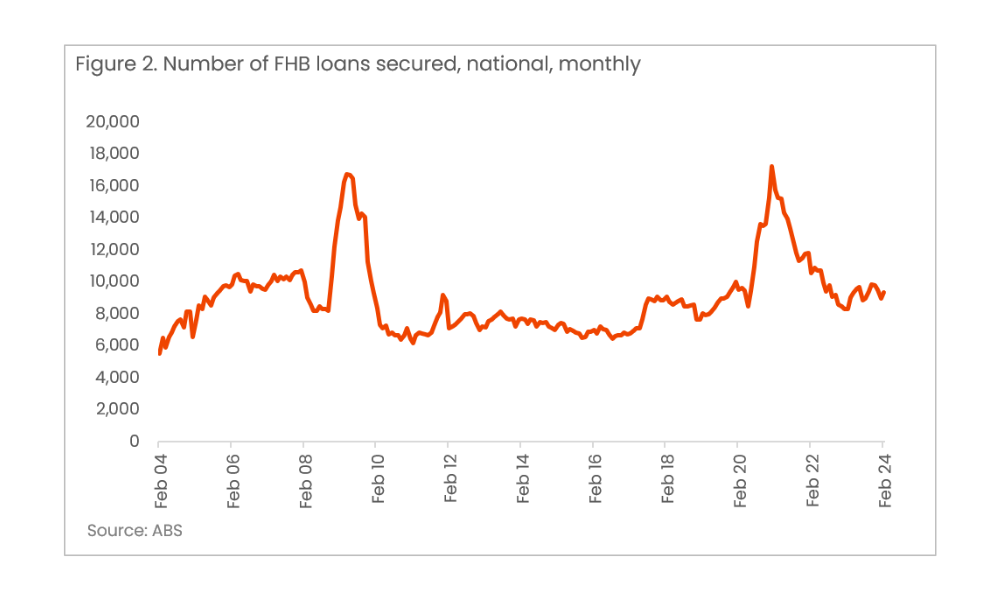

While the ABS’ lending indicators data from February showed a substantial $4.9 billion secured by first-home buyers, up 4.8% from the previous month, the figure doesn’t necessarily indicate improved accessibility.

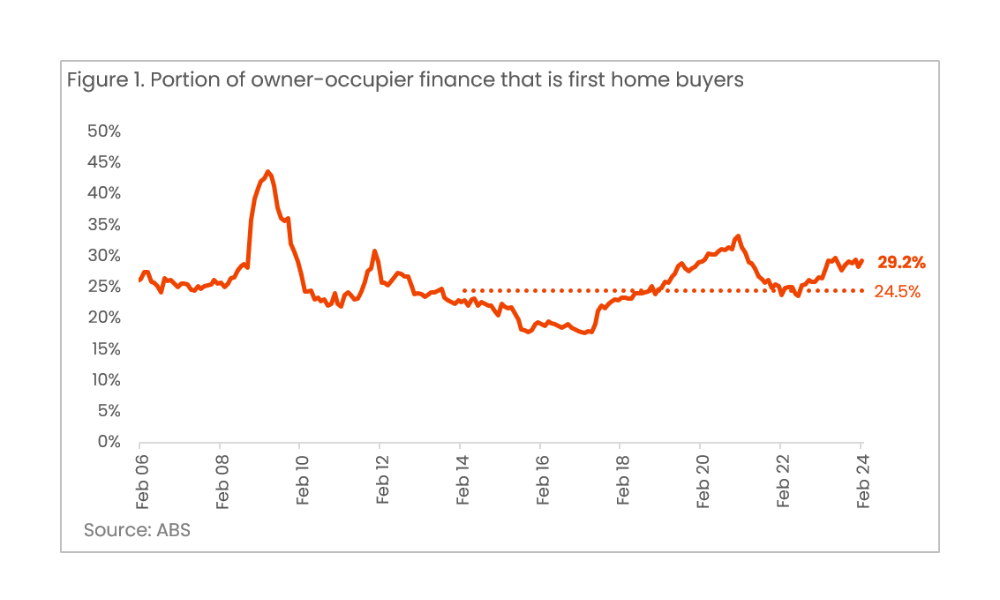

The data might suggest first-home buyers are becoming a larger portion of the market with 29.2% of all owner-occupied finance, but as Owen pointed out, “Does this mean first-home buyers are finding it easier to buy property? Not necessarily.”

The increase in first-home buyer finance is contrasted by the slower growth or decline in non-first-home buyer finance, skewing the overall picture. Over the past 12 months, the value of first-home buyer lending has surged by 20.7%, quadrupling the annual growth rate of non-first home buyer owner-occupier lending, which stands at 5%.

“The increase in the share of first-home buyer finance has been exacerbated by relatively mild growth in non-first-home buyer owner occupier finance,” Owen said.

The relative measurement indicated more about the market dynamics than a genuine increase in first-home buyer participation.

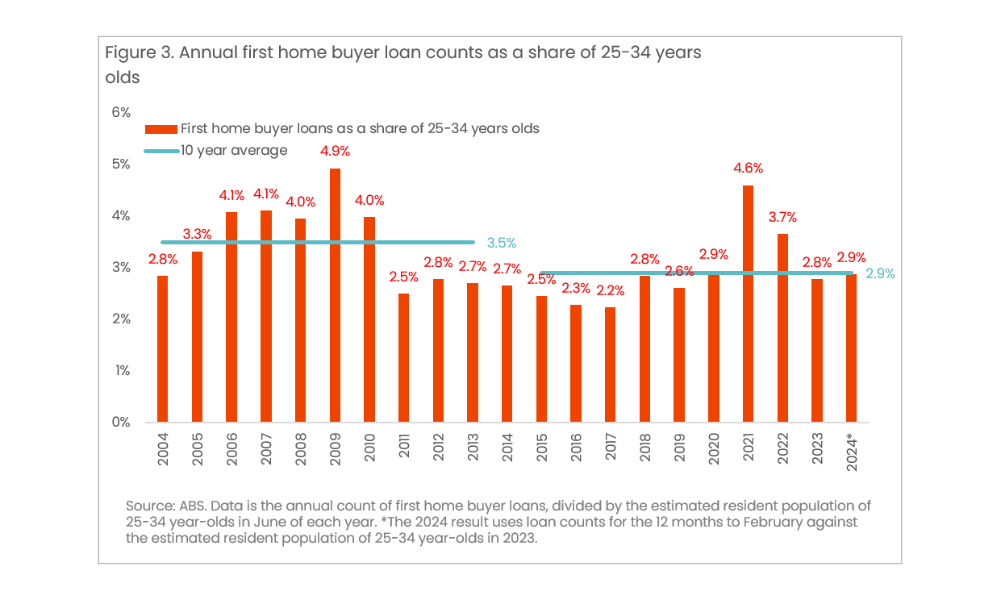

Despite appearances, the actual number of first-home buyer loans secured is currently below the record high of 2021, with significant fluctuations largely attributed to temporary government incentives.

This cyclical pattern fails to provide a stable foundation for sustained first-home buyer market entry, especially when considering the broader economic landscape affecting home values and market competitiveness.

Temporary government incentives such as the first home owner grant and the HomeBuilder grant have historically created spikes in first-home buyer activity. However, these are seen as artificial boosts that do not offer long-term support or affordability.

“These grants seem to have a temporary effect on first-home buyer numbers and may just bring forward demand for those that could have bought into the market at a later date,” Owen said.

Get the hottest and freshest mortgage news delivered right into your inbox. Subscribe now to our FREE daily newsletter.